2015 2nd Quarter Market Commentary

2015 2nd Quarter Market Commentary

July 22, 2015 | Documents and Literature,Insight,News & Press | Editor | 0 Comment

Overview

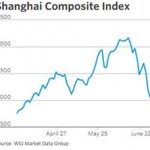

The fireworks came out just in time for the Fourth of July. The second quarter was relatively sleepy until the end of June when the Greek debt crisis made headlines again. Greece rejected a cash-for-reform proposal by the EU and missed an IMF debt payment causing a banking system closure. The Greek people voted on the matter July 5th and rejected the plan as well. As of this writing, no final agreement has been made. Additionally, there has been a massive correction in the Chinese stock market where the Shanghai Composite Index dropped 22% in a matter of weeks. To cap it off we had an announcement from Puerto Rico’s Governor that said the Commonwealth cannot pay its debts. These are not exactly the type of fireworks we enjoy but we were thankful for our distant viewpoint.

Economy

In our last commentary we discussed the fear of weak first quarter economic growth; this was substantiated as GDP contracted 0.2% during the first three months of the year. Our main concern was determining if there were systemic growth issues or if “one-off” explanations were to blame. At this point we feel confident saying that fundamental economic drivers are strong. That said, isolated issues will continue to trigger volatility and irregular economic readings. The second quarter GDP number is expected to be positive as estimates range from 1% to 4% with a weighted average of 2.3%. Durable goods orders (ex-transportation) in May were finally up after seven months of consecutive declines. This coupled with a strong consumption report in May persuades our team to expect second quarter GDP growth in the 2% range.

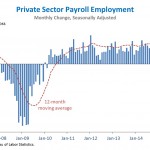

When we reference “fundamental economic drivers,” two such examples are the employment picture and the housing sector. The June jobs number came in at 223k which is not spectacular but enough to pull us out of the current slow growth trajectory. It is also worth noting that we have now had 64 months in a row of growth in private payrolls, the longest streak since at least the late 1930s. Another piece of positive news was that the median duration of unemployment fell to 11.3 weeks (the lowest since 2008).

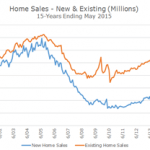

On the housing front, the most recent data in regards to existing and new home sales were both better than expected. Sales of existing homes in May were up 9% from a year earlier, according to the National Association of Realtors. Also, new home sales were up 20% from a year ago, hitting their highest level in seven years. Encouragingly, higher mortgage rates did not negatively impact sales. The anxiety over rising rates has dampened economists’ enthusiasm regarding the housing sector. However, this data reinforces our belief that housing is a sustainable positive force and a slowly rising mortgage rate scenario will not derail the story.

Below is our list of concerns that we continue to monitor in 2015:

Instability in Russia and the threat of more aggressive military action from Putin

An ugly Greek Exit from the Euro and the impact on Europe

Slowing growth in China and ongoing fears of Chinese banks with questionable loans (more below)

Growth of terrorist groups in the Middle East

Stocks

The second quarter of 2015 posted muted returns for equity investors, similar to the first quarter. The S&P 500 returned 0.3% for the quarter and is now up 1.2% year-to-date. More recently, equity markets were impacted by several growing concerns, mainly outside of the United States. Debt issues in Greece & Puerto Rico coincided with extreme volatility in Chinese equities (graph below) to change investor sentiment for the worse. In addition, investors continue to grapple with the timing of a Federal Reserve rate hike and how that will affect the U.S. economy.

During the quarter, five of the ten economic sectors in the S&P 500 posted positive returns, with the other five posting negative results. Healthcare was again the best performing sector up 2.8% for the quarter, now up 9.6% year-to-date. Healthcare companies continue to benefit from new drug development, ongoing M&A activity, as well as increased venture capital investment. Venture capital funds are on pace to invest almost $7 billion into biotech companies in 2015, which would surpass last year’s record of over $6 billion. The Consumer Discretionary & Financial sectors were the next best performers during the quarter, up 1.9% & 1.7% respectively. Both sectors are benefitting from the housing data mentioned previously.

Coming off a strong 2014, the Utilities sector was the worst performer during the first quarter and again in the second quarter, down 5.8%. Utilities are now down 10.7% year-to-date. Utilities and other “bond proxies” continue to be impacted by the Federal Reserve’s rate hike talk. The concern is twofold: 1) investors may shift money to bonds (away from Utilities) as bond yields become more attractive and 2) higher rates could impact debt financing costs for this capital-intensive sector. In our Q4 2014 commentary we highlighted how Utilities were trading at lofty valuations. Given the correction over the last few months, we are now beginning to find value in specific, well-capitalized, high dividend paying stocks in the sector. The second worst performing sector during the quarter was Industrials, down 2.2%. Industrials, along with the Materials & Energy sectors, were impacted by global economic growth concerns.

As we consider current equity valuations in this economic and interest rate environment, we still believe high quality companies, trading at a discount to intrinsic value, are an attractive alternative given the global investment landscape. In short, we continue to find value in stocks despite our list of concerns.

Bonds

In a reversal from the first quarter, bonds retreated into negative territory for the year. The Barclay’s Aggregate index (as represented by the ETF “AGG”) was down 1.8% for the quarter and is now down 0.3% for the year. The Federal Reserve did not raise the funds rate in June but did leave the window open for a move later this year. Domestically speaking the economy continues its uneven advance, providing the Fed Governors ample reason to begin the process of “normalizing” rates. On the other hand, destabilizing events in the global markets (mentioned above) are persuasive arguments for the Fed to go slow. In fact, the IMF (International Monetary Fund) has publically encouraged the Fed rate hikes to be delayed until 2016, giving time for the international turmoil to subside. It is anyone’s best guess as to the exact month that the “lift off” will begin but we do believe that it will occur later than many expect, and take longer to get back to “normal.”

Greece and Puerto Rico are suffering with the reality that debt is not free. Very simply, these two countries have borrowed more money than is sustainable given the poor shape of their economies. Regarding Greece, creditor nations do not want their citizens paying for excessive pensions. Many Greeks enjoy retirement beginning in their 50s while the creditor nations, notably Germany, have set a retirement age of 67. From an investing standpoint the markets appear to have discounted this situation, as long as the Euro stays intact and orderly. If the situation devolves into a contagion where other distressed members (i.e. Portugal and Spain) begin to favor a default themselves, more downside volatility is expected. Already, prices of high quality debt have rallied in a textbook “flight to quality.” Our approach, which favors high quality bonds, has benefitted from this recent rally.

The Puerto Rico crisis is unique due to the fact that it is not legal to file Chapter 9 Bankruptcy which was the path Detroit chose. Court rulings have sided with creditors and a negotiation must take place to work out the financing options. We expect this to be tied up in court and/or Congress for some time. A silver lining is that the high quality municipal market has not been affected by this development and the S&P Municipal Bond Index is virtually unchanged for the year. We have avoided Puerto Rico bonds for some time as this situation has been a slow motion train wreck for quite a few years.

We believe, as a result of all of these economic variables we have discussed, that inflation will remain muted in the U.S. We are largely avoiding the most Fed Funds sensitive part of the yield curve, which historically has been the 0-2 year sector. We continue to find value in the 5-7 year sector, with above market coupons and step-up agency structures. As reiterated earlier, we continue to focus only on the highest tiers of credit quality at this time.

Conclusion

The U.S. economy continues to prove it is on a “slow and steady” path of growth out of the Great Recession. Employment gains have been meaningful, the housing market continues to strengthen, and both inflation and interest rates remain low. From a macro-economic perspective, America is a bright spot in the world. Domestic stocks are fairly priced (not “cheap” and also not “bubble” territory). Bond yields are low, and will most likely be low for some time, but offer a reasonable rate of “safe” return. Globally, there are a few issues that give us cause for concern. There are also a few issues that make for great headlines but in all reality have very little impact on our clients’ portfolios. This quarter, a few of those issues (both real and media-driven) reached an inflection point. Given the unspectacular American economy, focus on these events led to increased volatility. It is very logical that this volatility will continue which is why we believe so strongly in, and to continue our focus on, the long term.

Continue reading –

2015 2nd Quarter Market Commentary

See which stocks are being affected by Social Media