Adobe Systems Incorporated (NASDAQ:ADBE), FedEx Corporation …

The S&P 500 (SPX) has seen its fair share of ups and downs in the first half of June, but the overall direction lacks conviction. Or is that changing? Like, real soon. This week kicks off with some noise due to failed weekend talks to rescue Greece. Just a little volatility primer before attention turns to the midweek Federal Reserve meeting.

Talks broke down Sunday night for Greece, which is lobbying hard for a new finance deal before a big payment deadline in coming days. The situation remains a wild card for global stock markets. Greece’s main composite index is off over 5% Monday, trading at its lowest since April. Europe’s broad stock averages are logging losses of at least 1%, with banking shares leading the day’s declines.

The week also features one of four quarterly “quadruple witching” dates, which bring the expiration of futures and futures options on top of stock and index options. That means the big firms with market muscle may have to unwind many of their stock-versus-futures-versus-options positions, and the net result might be a bit more trading activity, which could heat up volatility.

Volatility Still Low for the Low

Last week, the swings culminated in a narrowly mixed finish across the major stock averages last week. And this state of limbo sets the scene for a midweek Federal Reserve meeting—a session that’s not expected to end with an increase to interest rate policy, although it’s not a foregone conclusion. However, the meeting is expected to offer more clues on just when the Fed pulls the trigger on the first rate hike since 2006.

In fact, the SPX slipped Friday as concerns about uncertain Greek debt negotiations weighed on European equities markets; the weakness on the other side of the Atlantic set the table for a dip on Wall Street. Energy stocks led a retreat across all 10 SPX sectors, as crude slipped below $60 a barrel. For the week, however, the SPX was decidedly flat. The index also sits at nearly the same levels as in mid-May. The average daily point move in the SPX over the past month has been 8 points. That compares to average 11-point daily moves in the three months prior.

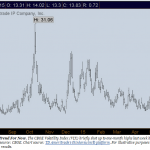

Yes, despite the media focus on the ongoing Greek debt debacle, the CBOE Volatility Index (VIX) dipped from one-month highs of 15.74 hit intraday last Tuesday to finish the week at 13.83 (figure 1). It’s down 29% year to date. Since the index tracks implied volatility in SPX options, the decline in VIX is a potential sign that participants in the options market aren’t yet bracing for any real Greek tragedy in the days and weeks ahead.

In Yellen’s Own Words

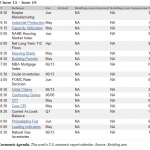

On the economic front, data on housing is due for release early in the week. Jobless claims and consumer inflation figures help set the tone for morning trading Thursday (see the full calendar in figure 2). Those reports may not matter a whole lot, considering that the Fed meeting and Chair Janet Yellen’s subsequent press conference on Wednesday afternoon are likely to be this week’s headliners.

The U.S. central bank is looking to raise interest rates later this year, it’s said, in order to normalize what has been excessively easy monetary policy. Still, with spotty data to start the year as well as international distractions, Yellen and crew want to be sure that actual price inflation, which remains low, will rebound to near the Fed’s 2% target. The May jobs report showed a jump in wages, which rekindled inflation talk.

As of Friday’s close, Fed funds futures markets had priced in a 48% probability of a 0.25 rate increase for the middle of September. And while no change in rates is expected this week (or at least, it’s given very thin odds), bond yields could react higher to any changes in verbiage within the post-meeting statement. Forward-looking comments from the Fed head could have market impact as well. The yield on the 10-year Treasury note, a benchmark for several borrowing markets, hit 2015 highs of more than 2.4% last week. Higher rates tend to be positive for banking stocks, but can be a drag on other sectors amid fears that prohibitive borrowing costs could slow business expansion.

A limited earnings menu could distract only briefly from the Fed meeting. Among the few notable reports, software-maker Adobe Systems (NASDAQ: ADBE) reports Tuesday. FedEx (NYSE: FDX) and Oracle (NYSE: ORCL) are slated for Wednesday releases. Grocery chain Kroger (NYSE: KR) reports Thursday, and home builder KB Homes (NYSE: KBH) releases its results on Friday.

Good trading,

JJ

@TDAJJKinahan

This piece was originally posted here by JJ Kinahan on June 15, 2015.

TD Ameritrade, Inc., member FINRA/SIPC. Commentary provided for educational purposes only. Past performance of a security, strategy, or index is no guarantee of future results or investment success. Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before investing. Supporting documentation for any claims, comparison, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading.

Posted-In: JJ Kinahan The Ticker TapeEducation Economics General Best of Benzinga

© 2015 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Link to article:

Adobe Systems Incorporated (NASDAQ:ADBE), FedEx Corporation …

{kind=link}