Baxano Surgical: A $3 Dollar Stock Trading At $1. – Seeking Alpha

Baxano Surgical (BAXS) is a medical device company focused on minimum invasive surgery (MIS) equipments, which have shown superior clinical results comparing to traditional open surgeries. I rate BAXS as a strong buy for the following reasons:

- BAXS’s revenue and earnings have bottomed in 2013 and will grow explosively in 2014

- Insider buys and positive technical signals support the stock price

- Legal overhangs are gone and BAXS has no POD exposures

- BAXS has a healthy balance sheet with enough cash to operate for the remaining of 2014

Company Description and Investment Reasons

BAXS was formed in 2013 when TranS1 acquired privately held Baxano Inc. and adopted the Baxano Surgical Inc. name. The deal establishes BAXS as a unique, highly differentiated MIS spine platform. It almost doubles BAXS’s revenue base (from $3.2m in Q3 2012 to $5.7m in Q3 2013), and it provides much wider access to surgeons, especially those with an interest in the MIS market. The merged company is currently headquartered in Raleigh, North Carolina, and it has a large training center in San Francisco, California.

I have a price target of $3.2 for BAXS comparing with 2/19/14 closing price of $1.29 (250% upside). 2013 turns out to be a successful transition year for BAXS and I believe 2014 is the harvesting year. BAXS has a great potential to become the market leader in fusion of the lower lumbar spine. This is an area that the larger companies do not actively pursue, so it provides many opportunities for small players like BAXS with innovative technologies. Now is the best time to invest in BAXS before the stock price taking off. Below is a detailed explanation of my investment reasons:

1. BAXS’s revenue and earnings have bottomed in 2013 and will see explosive growth in 2014

Minimum invasive surgery (MIS) is a fast growing sector in spinal market. It is currently less than 20% of the spinal market but is estimated to exceed 50% of the market share in the next few years (source: Barrington Research report (12/31/2012), Nuvasive Presentation). Comparing with traditional open surgery, MIS offers patients a much better experience (e.g., less pain, less blood loss, less complication rate and quicker to recover). And there are plenty of clinical evidences to support the superior of MIS over traditional open surgery. BAXS is the only publicly traded pure MIS player. Therefore it will be one of the primary beneficiaries of the rising MIS market.

One of BAXS’s main products, AxiaLIF, is a proven procedure that had gained surgeons’ acceptance since it was launched in 2005. Its utilization is peaked in Q4 2008 but since then started to decline because of the elimination of the CPT category I code in early 2009. The elimination of the category I code caused problems for surgeons to get reimbursements from insurance companies, and it caused the AxiaLIF sales to tumble. The company successfully announced a new CPT category I code in January 2013, and also expanded its sales and distribution network to drive the revenue growth. There are many surgeons who have used the product in the past showed strong interests to return because they have been trained and are familiar with the procedure. The market for AxiaLIF has increased since 2009 and it is estimated that the global market opportunity for AxiaLIF is over $1B, with $700M in the US (source: Barrington Research report). Therefore I expect the sales of AxiaLIF should grow significantly in 2014.

Another product, iO-Flex, started to show growth momentum since TranS1 merged with Baxano. The merger provided BAXS with the necessary scale to efficiently operate in the competitive spinal market. The products from TranS1 (AxiaLIF, VEO) and Baxano (iO-Flex and iO-Tome) are good complementary to each other. Now BAXS can provide a portfolio of MIS equipments for the entire lumbar region. As the CEO mentioned in the latest earnings call, they saw many surgeons using one of their products also show very high interests on their other products. This creates the cross-marketing opportunity and significantly expands BAXS’s client base. In addition, I expect the gross margin to increase because of the cost saving from merger synergy and increased sales.

2. Insider buys and technical analysis

For small cap companies I pay special attention to insider buys because it aligns the management’s interest with shareholders. As Bloomberg data shows, the current CEO bought 10,500 shares of stock in the open market at the price of $1.03 in 12/5/2013. In addition, the CEO’s compensation is highly linked to the company’s growth. For example, a large chunk of his stock option would only vest if the company’s revenue can increase by over 30% for two consecutive quarters.

Figure 1 shows the two years weekly chart of BAXS. The stock has built a beautiful U-shaped bottom and is currently in its early uptrend (higher lows and higher highs). The stock breakout in early 2014 and is currently sits above its 20days moving average, which is above its 50days moving average (a bullish technical signal). The huge volume since last December also confirms the validity of the recent uptrend.

Figure 1. BAXS Stock Weekly Chart

3. Legal overhang is gone. No POD exposures.

In July 2013 BAXS reached a definitive settlement with DOJ regarding an investigation which had begun in October 2011, when the government issued a subpoena related to whistleblower allegations. The settlement removed uncertainties surrounding the company for two years and BAXS admitted no wrongdoing in the settlement.

DOJ recently started an investigation regarding physician-owned distributorship (POD). It is estimated that the POD takes 20% of the spinal market share, and many large companies are involved in the investigation. BAXS has mentioned in its earnings call that it does not have any POD exposures. It is even possible for BAXS to gain more market share that historically belongs to the POD related network.

4. Healthy balance sheet and low probability of share dilution in 2014

At the end of Q3 2013, BAXS has less than $5m debt with $11.6m cash. Furthermore, in last December it secured a credit facility of up to $15m from Hercules Technology Growth Capital, and entered into a stock purchase agreement with Lincoln Park Capital for up to $7m. I estimate that BAXS should have around $33m cash on a pro-forma basis. Assuming the current cash burn rate of $6m per quarter, BAXS should have enough cash to fund its operation for the rest of 2014. This gives the management enough time and flexibility to operate the company and show earnings and revenue improvements in 2014.

Industry Introduction

Figure 2. The Human Spine. (source: Google Images)

As shown in Figure 2, the human vertebrae are categorized into five regions beginning from the base of the skull: cervical, thoracic, lumbar, sacral and coccyx. The spine market is estimated at $6.5B in the US and $8B worldwide. BAXS focuses on the lower lumbar region of the spine, which market is estimated to be over $1B in the US and $3B on a worldwide basis. The US market is dominated by private payers (i.e., insurance companies). And in the past few years, there has been a significant push back on reimbursement. Therefore, the US spine market has seen little growth in the past few years. Since 2013, the spine market started to stabilize due to the economy recovery and more aggressive marketing from industry players and surgeons. It is estimated that the US spine market will grow 5% in 2014.

The Spine market is dominated by four large players: Medtronic (30% market share), JNJ/Synthese (26% market share), Stryker (8%), and NuVasive (8%). Most surgeons maintain relationships with multiple vendors, so the barrier for small players to enter the market is not high, but the competition is intense.

BAXS specialized in minimally invasive spinal (MIS) market, which currently is estimated at less than 20% of the overall spine market but has been growing much faster than the general spine market. Some research estimates that the MIS market share will increase to 80% within the next 10 years and becomes a standard care for spinal surgery. NuVasive, the market leader in MIS, has shown strong revenue growth in the last two years, which confirmed the fast growth of this sector. Although BAXS does not have the same scale and distribution network like NuVasive and other large players, it has its own advantages to succeed:

- It has a very low starting point. Because of the lack of physician reimbursement code during 2009-2012, the revenue dropped significantly during that period of time. After a new code in place and a growing sales team, it is expected that its revenue will grow significantly in 2014 and beyond.

- Most surgeons have relationships with multiple vendors, which lowers the barrier for smaller players to enter the market.

- After the merger between TranS1 and Baxano in 2013, BAXS now has a much broader product portfolio for the MIS market. Historically TranS1’s products had little overlap with Baxano’s products, so the merger significantly increased their client base and provided their sales team the opportunity to cross-marketing multiple products together. The management team mentioned in the latest earnings call that they have seen signs of the merger synergy to start to drive the sales growth.

- Some of BAXS’s products are unique and serve the market that is historically overlooked by larger players (e.g., iO-Flex is the only commercially available MIS decompression approach that is applicable to all types of stenosis).

- BAXS is one of the few pure MIS players. Multiple sources have confirmed that the MIS market will grow at a much higher speed than the general spinal market. So BAXS should benefit most from this fast growing sector.

Product Introduction

BAXS currently markets four main products. The company sells its products through a direct sales force, independent sales agents and international distributors.

- AxiaLIF family of products for single and two level lower lumbar fusion. It was first commercially released in January 2005;

- VEO lateral access and inter-body fusion system. It was commercially launched in November 2011;

- IO-Flex system, a proprietary set of flexible instruments used by surgeons during spinal decompression procedures. It was commercially launched in 2009;

- IO-Tome instrument, which rapidly and precisely removes bone, specifically the facet joints that is commonly performed in spinal fusion procedures. It was commercially launched in the fourth quarter of 2013.

Table 1 shows the revenue distribution among these products as of Q3 2013.

Domestic revenue:

(in thousands)

%

AxiaLIF

$ 1,617

29%

iO-Flex

2,654

47%

VEO

523

9%

Other

492

9%

Total US Revenue

5,286

94%

International Revenue

364

6%

Total Revenue

$ 5,650

100%

Table 1. BAXS Revenue Distribution across Products

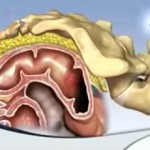

AxiaLIF: AxiaLIF is a minimally invasive alternative approach to traditional fusion procedures. AxiaLIF accesses the spine through the presacral region, which compared with other approaches, is free of critical structures, and does not require manipulation of supporting tissue, blood vessels, nerves or bone. The process begins with a one inch incision below the patient’s tailbone, providing access to the spine through the presacral region, a fatty area just above the bowel, which is entered percutaneously. Once the spine is accessed, the center of the degenerate discs is removed, and replaced with bone growth material, and disc height is restored with an AxiaLIF implant. The spine is then stabilized with posterior fixation that is similar to other approaches.

Figure 3. AxiaLIF (Source: Baxano Surgical)

There have been several clinical evidences that showed the AxiaLIF has a high rate of surgical success and low rate of complication. In addition, patients benefit from a less invasive procedure with significantly better recovery times: patients are typically released after 1 day in the hospital, with about 10% going home the same day versus two to four days for those open procedures. AxiaLIF patients generally return to work in one to two months versus three to six months for other approaches.

Open Surgery

MIS

PLIF

ALIF

TLIF

XLIF

AxiaLIF

Infection

0.4%-11%

0-3.2%

0-9.2%

0%

0%

Vascular Injury

0%

1.9-18.1%

0%

0%

0.10%

Visceral Injury

0%

0-6%

0%

0-12.5%

0.59%

Retrograde Ejaculation

0%

0-4.5%

0%

0%

0%

Dural Tears

0-20%

0.20%

0-19.6%

0%

0%

Neural Defect (Transient)

3.2%-8%

0%

0-3.9%

0-25%

<0.1%</strong>

Neural Defect (Permanent)

0-3.6%

0-2.6%

0-6.6%

0%

0%

Table 2. Major Complication Rates Comparison between Different Approaches

One major advantage of AxiaLIF is the economic savings the procedure is able to generate. BAXS has been compiling data to detail this through a health economic study and published in a reputable peer-reviewed spine journal (“Journal of Spinal Disorders and Techniques”) in December 2013. The study shows that there is a potential for a $4,500 per patient savings when using the AxiaLIF approach versus a TLIF. Given the reduction in morbidity and hospital stay times of one to two days, the short-term complication rate has been shown to be as much as 50% less using AxiaLIF. Based on the study, I believe it will drive both hospital and private payer’s adoption of AxiaLIF for lower lumbar spinal fusion procedures as the cost of its system is more than paid for.

VEO: VEO is an innovative lateral inter-body fusion system (XLIF), which provides direct visualization to lateral fusion procedures. XLIF is pioneered by NuVasive, and its success has spurred a large number of imitators. But VEO differences from other competitors in that it evolves the process by using a two-stage retraction system that allows direct visualization. This creative design not only makes the costly neuromonitoring optional, but also better preserves the sensory nerve above the psoas because the nerve cannot be detected by the neuromonitoring equipment.

IO-Flex: iO-Flex is a proprietary minimally invasive set of flexible instruments allowing surgeons to target lumbar spinal stenosis during spinal decompression procedures in all three regions of the spine: central canal, lateral recess, and neural foramen. Instead of cutting through healthy pieces of the spine, the iO-Flex System uses a fine surgical wire to guide the thin iO-Flex shaver instrument to the location of the overgrown bone and tissue to shave away the stenosis from the inside out. It is the only commercially available MIS decompression approach that is applicable to all types of stenosis, with established reimbursement. Although the iO-Flex’s ASP is lower than a fusion (e.g., $3,300 for an iO-Flex procedure versus $11,000 for a single level AxiaLIF), iO-Flex is not seeing the reimbursement pushback, and it is seen greater usage in degenerative disc patients who were deferred from fusion, which makes iO-Flex a great hedge for AxiaLIF.

Figure 4. IO-Flex (Source: Baxano Surgical)

IO-Tome: iO-Tome is a unique, fast, precise MIS tool for facet removal, used during TLIF procedures. The management team sees great market opportunities for iO-Tome to expand its reach with surgeons in conjunction with other XLIF and TLIF approaches offered by its competitors.

Financials and Valuations

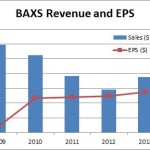

Figure 5. BAXS Revenue and EPS (source: author’s table, data from SEC filings)

Figure 5 shows BAXS’s historical revenue and EPS. It is clear that the revenue hit the bottom in 2012. I expect both the revenue and EPS growth will accelerate in 2014 according to the rationales explained previously in this article. Table 3 shows a more detailed income statement by each quarter.

Income Statement (Millions)

Income Sheet as of:

Sep-13

Jun-13

Mar-13

Dec-12

Sep-12

Jun-12

Mar-12

Currency

USD

USD

USD

USD

USD

USD

USD

Total Revenue

5.65

3.88

3.10

4.13

3.20

3.46

3.78

– Cost Of Goods Sold

1.51

1.30

1.03

1.56

0.84

0.91

1.00

Gross Profit

4.14

2.58

2.07

2.57

2.36

2.55

2.79

– Operating Expenses

11.44

9.40

7.76

7.96

8.11

8.84

8.51

Operating Income

(7.29)

(6.82)

(5.69)

(5.39)

(5.75)

(6.29)

(5.73)

– Non-operating Expenses

0.63

1.71

1.41

(0.33)

(0.15)

(0.03)

–

EBT Excl. Unusual Items

(7.93)

(8.53)

(7.10)

(5.06)

(5.60)

(6.26)

(5.73)

– Unusual Items

(0.03)

–

–

(6.91)

(0.26)

(0.03)

(0.03)

Net Income

(7.96)

(8.53)

(7.10)

(11.97)

(5.87)

(6.29)

(5.76)

– Extra Items

0.56

1.07

1.40

6.65

–

–

–

Net Income excludes Extra Items

(7.40)

(7.46)

(5.70)

(5.32)

(5.87)

(6.29)

(5.76)

Basic EPS

(0.18)

(0.26)

(0.26)

(0.44)

(0.22)

(0.23)

(0.21)

Basic EPS Excl. Extra Items

(0.16)

(0.22)

(0.21)

(0.19)

(0.22)

(0.23)

(0.21)

Weighted Avg. Basic Shares Out.

45.20

33.41

27.32

27.29

27.28

27.26

27.25

Table 3. BAXS Income Statement by Quarter

Like many small medical equipment companies, BAXS is still in its early stage and has never reported a profit. Therefore I used relative value analysis and estimate my price target based on EV/Sales ratio. Based on my analysis, 2013 is the transition year for BAXS and should mark the start of the growth of its revenue and earnings. With the successful integration of acquisition, unique MIS products and an increased sales force, I assume that the sales will increase by 25% in the next two years. I believe my 25% revenue growth rate assumption is conservative because

- It is estimated that MIS market is growing 10+% each year

- The integration between TranS1 and Baxano creates a larger market and the cross-marketing opportunity for BAXS

- BAXS can win more market shares from POD, which accounted for 20% of all spine cases billed to Medicare in 2011

- BAXS is pushing hard to get wider insurance coverage for AxiaLIF, and starts to win some success as mentioned in Q3 earnings call

Using 2015 as the target valuation date and apply a 15% discount rate, we apply an EV/Sales ratio of 4, which is comparable with other players in the spinal market. We get our target price of $3.2 based on the above assumptions.

Investment Risks

It is important to remind investors that investing in micro-cap stocks has much higher risk than investing in mid/large cap ones. These stocks are typically thinly traded and lack of institutional supports. Many micro-cap companies have unique or innovative technologies, but their small size constraints them from successfully competing with larger players in terms of efficient operation and execution. These risks are all applicable to BAXS, and I also want to point out certain specific downside risks associated with BAXS. I encourage each investor to evaluate these risks carefully before making investment decisions.

1. The integration between TranS1 and Baxano might be slower than expected.

As I mentioned earlier, the successful integration between TranS1 and Baxano not only brings cost savings, but also creates cross-marketing opportunities and increases the client basis. For these revenue and cost synergies to happen, BAXS needs to integrate its sales team and cross-train each salesperson to cover all products that BAXS can provide. This is a complicated process and any delay may cause pressure for the stock price. The company management mentioned in their latest earnings call that all integration progress is on target, and it is further confirmed by the preliminary Q4 results announced on January 13, 2014.

2. Insurance companies continue to push back for AxiaLIF reimbursement, and AxiaLIF might fail to gain surgeons’ wide acceptance

Since the new CPT code was established last January, the sales of AxiaLIF have been below expectation partly due to the lack of broad reimbursement from insurance companies. BAXS employed two strategies to expand the coverage for AxiaLIF. First, it collected all the clinical results and economic data on AxiaLIF and published them in reputational national spinal journals. Second, BAXS works with surgeons and leverages the positive clinical data to get insurance company to pre-approve procedures on a case-by-case basis. I think BAXS is doing all the right things to push for wider acceptance for its products. As evidenced in Q3 earnings call, their strategy showed early success by wining some insurance acceptances.

3. BAXS may need to raise additional capital in the future

As I discussed earlier, BAXS has enough cash to operate in 2014. But if its revenue growth cannot meet the expectations, it may need more capital and it is possible for BAXS to dilute its common shares.

Summary

I rate BAXS a strong buy with the target price of $3.2. 2013 turns out to be a successful transition year for BAXS. The company specializes in a fast growing sector-minimal invasive surgery (MIS) spinal market. With innovative technology, a growing and focused sales force, and successful integration, I believe we will see an explosive revenue and earnings growth for BAXS in 2014. The current $1.3 price provides investors an excellent entry point with high risk adjusted return opportunity to invest in this future market leader in MIS.

Source:

Baxano Surgical: A $3 Dollar Stock Trading At $1.

Disclosure: I am long BAXS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More…)

Original source:

Baxano Surgical: A $3 Dollar Stock Trading At $1. – Seeking Alpha

{kind=link}