Can The Stock Market Stand Naked? | Seeking Alpha

Summary

The U.S. stock market will soon face conditions it has not had to endure in more than three years.

Starting in November, it is projected that stocks will trade without the support of QE or Operation Twist for the first time since September 2011.

Thus, it is worth exploring whether the stock market can stand naked without the cloak of security so continuously provided by the Fed these past many years.

On November 3, the U.S. stock market is slated to face conditions it has not had to endure in more than three years. For it is on this date a mere five and a half months away and after an extended period of tapering that the Fed’s QE3 stimulus program is expected to come to an end. And with this ending, stocks are projected for the first time since September 30, 2011 to have to trade not only without the steady injection of liquidity through asset purchases from the Federal Reserve, but also without the duration extending support from their past Operation Twist programs. It is even open for discussion as to whether the Fed will continue to reinvest the principal payments associated with maturing agency debt and agency MBS on their balance sheet as they have in the past during the post crisis period. Given how dependent the stock market has been on Fed stimulus in the years since the financial crisis, this quickly approaching day raises an important question for investors. Can the stock market stand naked without the cloak of security so continuously provided by the Fed these past many years?

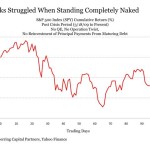

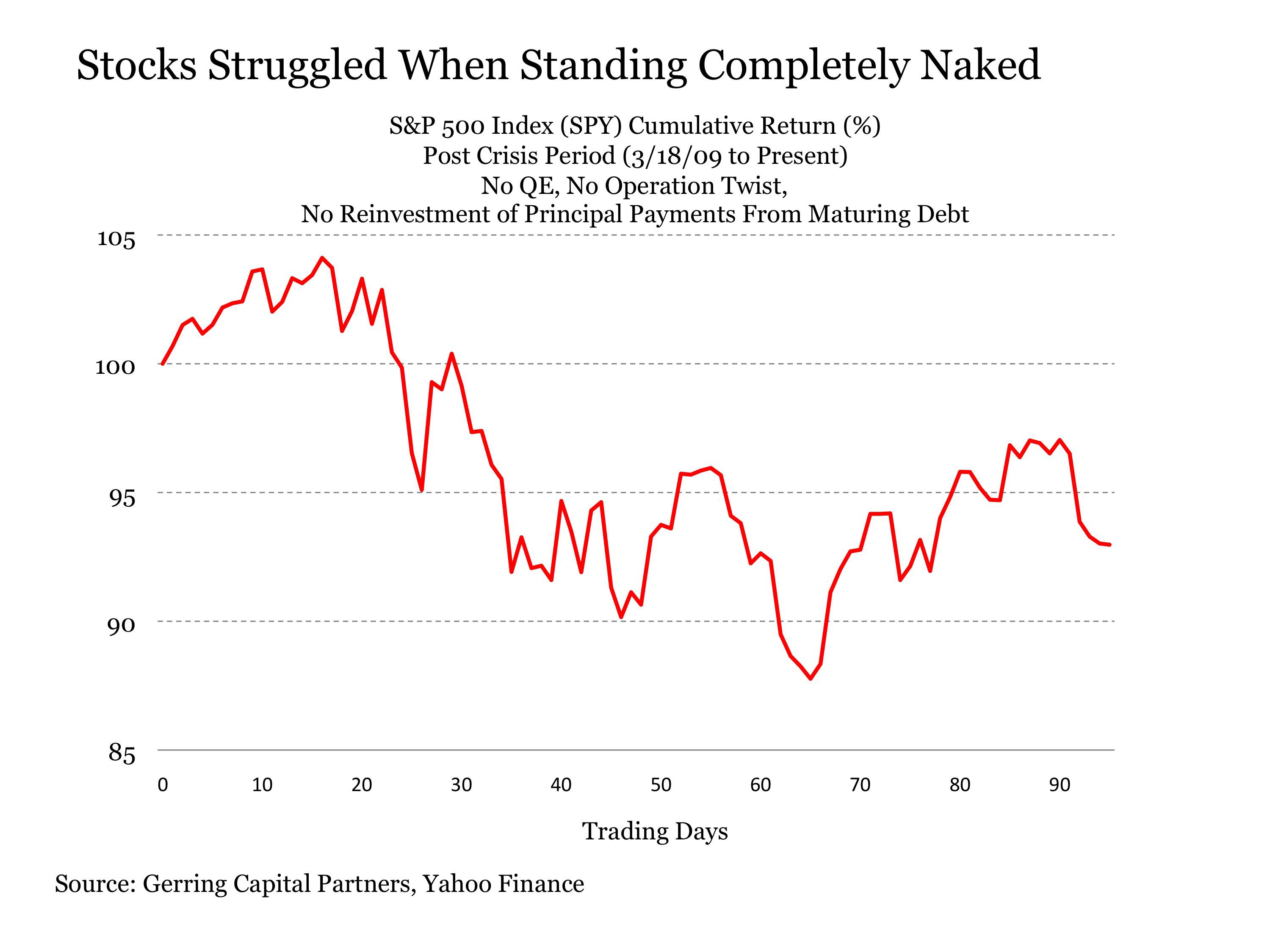

The market has been forced to go cold turkey on only rare occasion since the market bottom in March 2009. In the 1,301 trading days since the Fed first launched QE1 in earnest on March 18, 2009, the stock market (SPY) has only faced 95 trading days without QE, Operation Twist or the reinvestment of principal payments from maturing debt. All of these dates occurred during the period from April 1, 2010 to August 16, 2010, and the performance of the market during this period was less than stellar. After holding up well over the first two weeks, stocks rolled over and dropped by double-digits over the next two months in a phase that included the infamous “flash crash” on May 6, 2010. In short, the market’s results under these circumstances were generally poor.

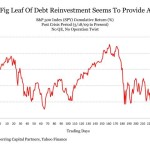

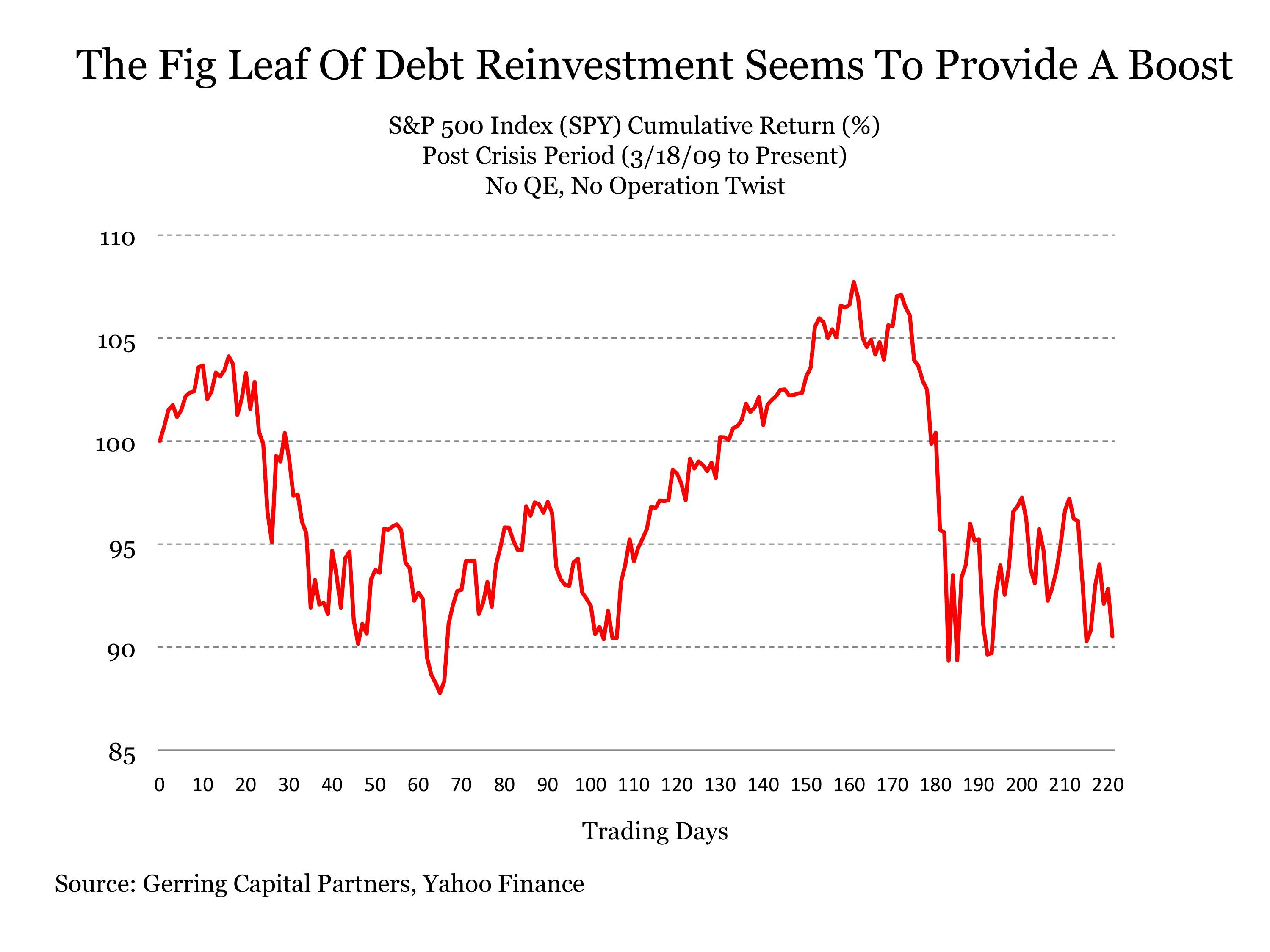

Suppose the Fed continues reinvesting principal payments from maturing debt once QE3 draws to a close. Has the market performed any better if these trading days are added into the equation? At first glance, it seems to have its moments when it helps the market. Over the combined 221 trading days under these conditions that occurred first from April 1, 2010 to November 11, 2010 and again from July 1, 2011 to September 30, 2011, the stock market struggled at times, but also showed phases where it could sustainably rally. Perhaps stocks with the fig leaf of debt reinvestment have the resilience to at least hold their own once the Fed ends QE?

The addition of an important caveat changes the perspective completely on this point. The bursts higher in the chart above were driven by one very critical factor, as they were sparked by explicit commitments from the Fed that more stimulus would soon be on its way. Former Chairman Ben Bernanke’s speech in Jackson Hole on August 26, 2010 was the first instance, and Bernanke’s exposing his wide range of policy tools following the August 9, 2011 FOMC meeting was the second. So during the Fed sparked rallies that followed, the market was standing virtually naked from an asset purchase standpoint but with the security knowing that a full new wardrobe of stimulus would soon be on its way.

So how then has the market performed both when it has been forced to stand virtually naked AND with the perception that it would remain naked without additional stimulus support from the Fed coming soon? This sample includes only 129 trading days first from April 1 to August 26, 2010 and then from July 1 to August 8, 2011. It is arguably the most relevant for consideration when projecting ahead to the post QE3 period that is projected to begin in November 2014, as the Fed seems intent this time around to exit the asset purchase game and turn its policy focus elsewhere. And the results during this group of 129 trading days, or roughly 10% of the entire post crisis period, are disconcerting.

Overall, stocks are down a collective -24% in post crisis trading under these conditions. And these past declines occurred during times when stocks were trading at a far more reasonable 12 to 14 times trailing 12-month earnings that is considerably below the 19 times earnings multiples in today’s stock market.

Does this mean stocks are destined to plunge once QE3 comes to its anticipated end in November? Not necessarily, for instead of shutting off the liquidity fire hose all at once as they did at the end of QE1 and QE2, which in retrospect for the Fed turned out to be massive and shocking tightening moves for the market, the Fed has been much more gradual and deliberate with their tapering strategy this time around. As a result, the correction may get underway well before the end of QE3, and it may take far longer to play out before markets find their final bottom. This is not necessarily a good thing for stock investors, however. For if the market correction is more gradual, the Fed will be under far less pressure to intervene with more stimuli to boost the market. A more gradual decline may also be far more detrimental to the typical stock investor, as one of the most dreaded characteristics of a creeping bear market is that it traps so many in the downdraft before they are even aware that a major correction is well underway.

How things play out come November will be interesting to see. But if the recent past provides any precedent, it is not a time that shapes up well for the complacent stock market investor.

Disclosure: This article is for information purposes only. There are risks involved with investing including loss of principal. Gerring Capital Partners makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made. There is no guarantee that the goals of the strategies discussed by Gerring Capital Partners will be met.

Source:

Can The Stock Market Stand Naked?

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More…)

Additional disclosure: I am long stocks via the SPLV and XLU as well as selected individual names. I also hold a meaningful allocation to cash at the present time.

Continued here –

Can The Stock Market Stand Naked? | Seeking Alpha

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}