Cellular Biomedicine: Strong Sell On CAR-T Failure, Dishonesty Allegations And Stock Promotion, -94.6% Downside

Summary

With paid stock promotion CBMG has achieved an unsustainable $500m valuation, and with $20m in stock sold and insiders stock registered to sell, I expect CBMG will continue to collapse.

CBMG “Car-T” technology was acquired for $1.8m, has experienced patient deaths and is worthless. CBMG recent R&D of just $4.9m makes the $500m valuation clearly absurd.

CBMG founders face dishonesty allegations, are responsible for alleged illegal offshore stem cell clinic, while partnered with John Mattera who is currently serving 11 years in prison for fraud (again).

Multiple accounting and financial integrity issues, CFO and Auditor turnover, “material weaknesses” and “inability to timely file” a full 50% of quarterly SEC filings raises accounting and financial integrity questions.

Assuming CBMG is “real” and generously valuing CBMG on fundamentals show -94.6% near term and imminent downside.

I believe Cellular Biomedicine (NASDAQ:CBMG) is another worthless Chinese reverse merger using paid stock promotion. Detailed research proves CBMG has imminent -87% to -94.6% near-term downside.

CBMG was previously focusing on Nintendo screens for RVs and Boats and then morphed into a consulting firm claiming to help Chinese companies access American investors. Now, along with “paid consultant” LifeTech Capital and a strange $1.8m acquisition, CBMG has seen its stock temporarily increase by nearly 400% to a $500m valuation based on a hype driven biotech story.

What investors don’t know is CBMG’s claimed CAR-T technology has in fact recently seen patients die, while detailed research indicates this technology is un-viable. Even more concerning, CBMG was apparently spawned from an alleged illegal offshore stem cell clinic named “WA Optimum,” charging $30k+ for treatments which famous Stanford scientists claim have “no scientifically valid reason” and that the Chinese government apparently made illegal.

Even worse, CBMG founders attempted to partner with a famous fraudster, John Mattera, who is now currently serving an 11 yearprison sentence for a “blatant fraud” involving the theft of over $12.6m. Before founding CBMG, Derek Muhs worked as a sales representative at the M1NT restaurant. M1NT publicly described Muhs as “extremely dishonest” and “untrustworthy.” Furthermore, CBMG co-founder Derek Muhs has no medical background I can find.

Lastly, the company has a confusingly complex web of offshore subsidiaries, recent CFO turnover, and a new audit firm- all while internal controls have experienced past “material weaknesses” with restatements. All of this raises serious questions about the integrity of the financial statements.

With paid stock promotion losing momentum and CBMG successfully having sold $20m in stock, shares have begun breaking down. Even if you believe CBMG is an honest company, optimistically adding up the value of their acquisitions and businesses, you still get more than -90.3% near term downside from the current price.

I believe a $500m valuation for a questionable team of people with minimal R&D spending and just $5.2m of cash spent on latest acquisitions, hyping worthless and un-viable biotech compounds simply does not make sense. As the primarily retail shareholder base realizes what is going on, I expect CBMG stock to continue imploding back to its recent stock price of $5.08 per share before eventually going much, much, much lower.

All research is cited and linked. I encourage you to research the following to form your own opinions and understand what is truly going on…

CBMG: Paid Stock Promotion

I do not suggest anyone invest in any company that pays to promote its stock. Time and time again we have seen how these stories end, and with 10k+ stocks in the US alone, there is no reason I can see to invest in any company of this poor quality. I recommend you read the research below and form your own opinions.

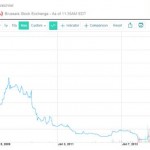

If you look at CBMG’s history you will see that from the start CBMG was initially working with Jeff Ramson of Proactive Capital. Jeff Ramson is famous for ties to exposed stock promoter “Tech Guru.”

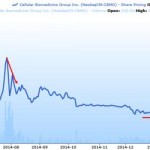

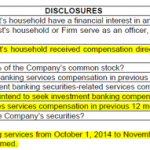

I believe the latest temporary move up for CBMG started February 2 this year when Boca Raton FL based “LifeTech Capital” issued a “report” with $23.75 price target. The disclosures in the fine print at the end of LifeTech’s report, however, prove clear compensation along with direct conflicts of interest.

(disclosure chart from LifeTech CBMG “report”)

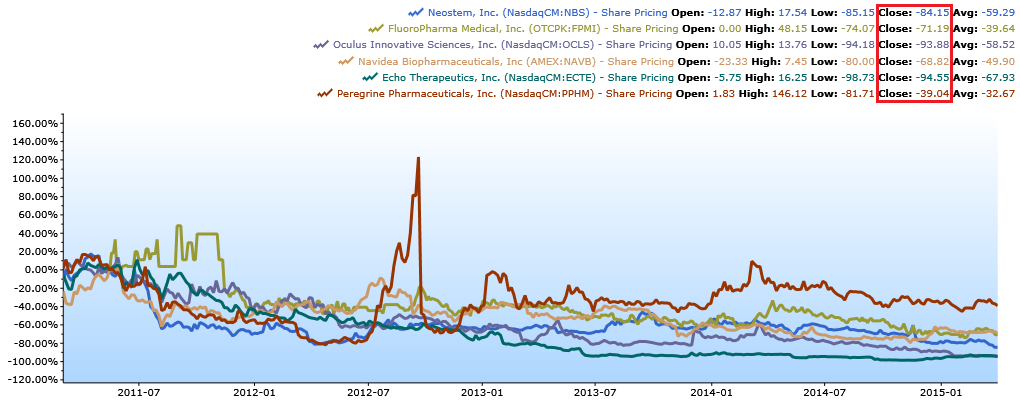

Unfortunately for LifeTech, their twitter feed is etched into internet stone for eternity. As an interesting template for CBMG let’s take a look at how some of LifeTech’s past stocks worked.

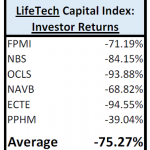

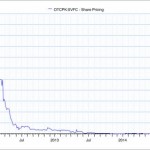

(Chart by author)

The most important part of the above chart is the red box showing % returns to shareholders over the timeframe, which I have summarized in the chart below of average returns to investors of these companies.

(Chart by author)

We can see shareholders who held these stocks over the above time frame lost -75.27% of their investment on average (so far, with probably a lot more downside). To give you context of how horrific this is, remember over the past 5 years biotech stocks as a sector are literally having the best bull market they have ever experienced. Over the same time frame the diversified IBB biotech ETF (NASDAQ:IBB) has increased +226%.

How could anyone possibly produce a return that bad during the biggest biotech bull market of history? To understand how LifeTech is so bad, we can dig a little deeper into the LifeTech Sr. Managing Director and analyst Stephen Dunn with firm Aurora Capital. If we look at his FINRA registration we can see Stephen Dunn is employed by both Aurora Capital (parent co of LifeTech) and also “NextWave Research,” which apparently “provides company sponsored research” and is run from Dunn’s house. We can also see Stephen Dunn was at Jesup & Lamont Securities Corp in 2009. The firm was expelled from FINRA in 2010.

Looking at Aurora Capital’s FINRA disclosures also shows an interesting set of regulatory disclosures including fines for “inaccurate financial books and records” and “failing to maintain minimum capital requirements.”

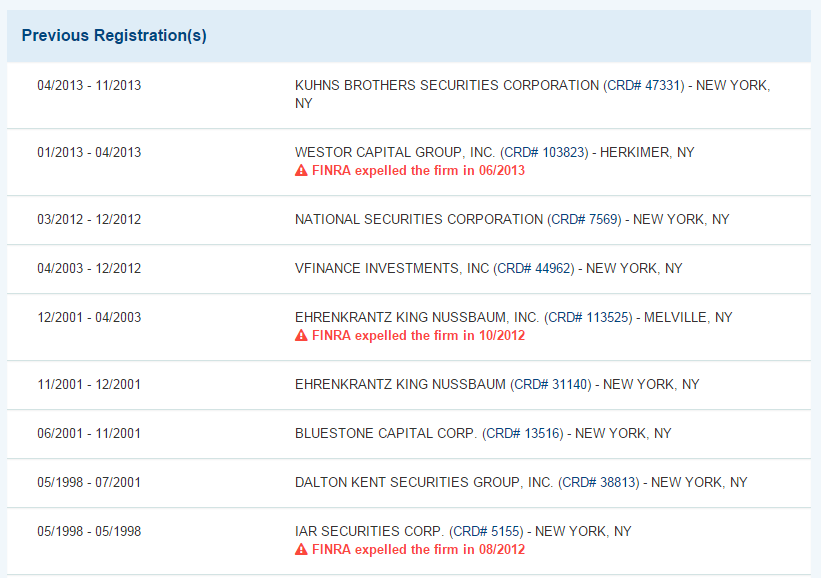

Perhaps most interestingly though, Stephen Dunn just days ago announced an attempt to fold LifeTech into “Newbridge Securities Corporation” and terminated coverage on CBMG (unlikely to be a positive for CBMG stock).

Newbridge Securities Corporation FINRA disclosures are shocking (emphasis mine). Allegations include “a former Newbridge representative converted over $160,000 from two newbridge customers accounts by wiring the funds from their accounts to bank accounts he opened in their names,” plus a $600k fine regarding “facilitat[ing]the manipulative trading of the stock of a company created as the result of a reverse merger.” Furthermore, Newbridge allegedly “execute[d]pre-arranged in-house agency cross and wash transactions that were intended to generate volume and support the price of the stock” as well as “registered representative used NewBridge’s market making capacity tomanipulate the shares of securities.” This SEC lawsuit is interesting background reading on NewBridge as well.

I also find Stephen Dunn’s disclosure on this 2/19/15 CBMG storyabout “no financial relationship” with CBMG puzzling when his 2/2/15 LifeTech report disclosure above clearly states he was paid and expecting to collect fees.

Given LifeTech’s history of investor financial disaster and association with a firm with allegations of manipulating stock prices of reverse merger stocks, I would not listen to Stephen Dunn, LifeTech or anything they are involved in.

It’s not only Stephen Dunn and his group involved with CBMG though, the SeeThruEquity shop has been involved in promoting CBMG. The comically bad StockNewsNow.com, which promoted CBMG, also seems to be a paid stock promotion website given their disclaimer about company compensation. Another paid stock promotion firm “Wide World of Stocks!” was also apparently paid to promote CBMG with host Damon Roberts, famous for his extensive infomercial experience.

In fact, CBMG’s 10k discloses that expenses decreased driven by a “Adecreasein investor relations expense of $1,543,000.” That means just the decline, a full 20% of their G&A the previous year, was pure “investor relations” cost! If their investor relations expenses declinedby over $1.5m in one year, what was the total?

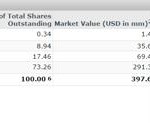

One important red flag is when a biotech stock with theoretically half a billion in (temporary) valuation has essentially no intelligent institutional investors involved. We can see 73% of CBMG’s shareholders are unsophisticated retail investors with no known sophisticated institutional investors noted. If CBMG is such an amazing opportunity, why the weird reverse merger and paid stock promotion? Why no partnerships with credible pharma companies or well-known biotech investors?

(Chart from CapIQ using public information)

The CBMG Ecosystem: Fraud, Prison, Alleged Illegal Stem Cell Clinics, and Financial Disaster

When investing in small speculative biotech companies, we all agree founders and management are the single most important factor. Therefore investment success is absolutely reliant on ensuring you understand the past and quality of the people in charge of your investment.

In order to understand CBMG I think you need to look at the mysterious history of CBMG’s founders, management and the crew of questionable individuals which collaboratively allow this “business” to exist.

Unfortunately the CBMG team faces: multiple allegations of dishonesty with many disclosure questions, connections to alleged illegal offshore stem cell clinic WA Optimum, plus direct partnerships with a convicted fraudstercurrently serving an 11 year sentence in prison.

Derek Muhs co-founded both CBMG and WA Health Care in 2009. He is shown below with CBMG founder Shu Li and CBMG CEO William Cao.

(pic from WA Health Flickr)

It appears Derek Muhs’s previous job before founding CBMG was working as a sales representative for Shanghai restaurant M1NT. Muhs seems proud of this, as we see in his online profiles. His profile on Bloomberg says, “he was instrumental in establishing M1NT” while his bio here states: “In 2008 heworked with a select group of international investors to launch M1NTShanghai.”

Also here (click Read More under his Biography section):

“Derek completed his work operationally at M1NT and continues as a shareholder and ambassador” while touting “He was one of the founders of the Atlantic International Property Group, Managing Director and he served on the Board of Directors.”

However, if we go to M1NT we find M1NT’s website states (emphasis added):

Mr Treamer worked for Mr Muhs in a failed Spanish property company that sold time share property to British clients until 2007. Mr Muhs sought employment with M1NT as a sales representative and accepted a salary of RMB22,000 per month from May 2008. During his employment Mr Muhs caused significant disruptions and the Directors of the company willingly accepted his resignation 10 months later and were most pleased to see him exit the business.

At no time was Mr Muhs a Director of the company nor a Founder or Managing Director as he has claimed in the media and represented.

M1NT’s Directors seriously caution any individuals or businesses against entering into dealings with Mr Muhs and in no way supports his claims or credentials. We found him to be highly dishonest and extremely untrustworthy and in no way would recommend him to any enterprise wishing to uphold a respectable standing within its industry sector.”

Furthermore, I note Derek Muhs apparently has zero biotech or healthcare background I can find but, just months after departing a sales job at a restaurant (earning barely ~$3,600 per month) he confusingly was founding an ostensibly $500m Chinese stem cell biotech company.

Apparently CBMG co-founder Shu Li directly invited (click Read Full Background) Derek Muhs’ involvement, and then Derek became CEO of WA Health. Interestingly Derek Muhs does not disclose on his Linkedin involvement as vice Chairman of “Global Health Investment Holdings Ltd.” (previous owner of 44.98% of CBMG). Notably, through this obscure and opaque Virgin Islands Shell, Derek Muhs and Shu Li own 16.2% of CBMG. This press release also indicates Derek Muhs is involved in helping WA’s “China Biotech Group” expand.

Derek’s other recent company appears to be a Chinese membership subscription offering called Affinity. Here is a picture of John Mattera (more on him shortly) and his wife at an Affinity event.

(Pic credit to Affinity)

Shu Li’s LinkedIn lists himself as founder of CBMG but also does not list his involvement as Chairman of “Global Health Investment Holdings, LTD” the BVI shell which held an enormous amount of CBMG stock and is a business partner to CBMG.

Dr. Shu Li apparently also thought it was worthwhile to research and pay to file this hilarious patent regarding sleeping with your head below your feet in order to live longer and increase “longevity.”

Even more interesting, there is a curious lack of detail in regards to Shu Li’s involvement with WA Optimum Health Care and WA Regen. Shu Li’s Bloomberg profile however lists him as the founder and Chairman of WA Optimum, while CBMG’s current CEO William Cao is also noted as the COO and CTO at WA. In fact nearly the entire CBMG team is connected to the WA Health Care venture.

Below we see previous CBMG CFO and current VP of Business Development Andrew Chan seems to make no mention of his involvement with WA Optimum on his CBMG website bio, while his Bloomberg bio states he is currently the CFO at WA Optimum. Is Andy Chan still the current CFO at WA Health?

(pic credit to WA Optimum)

Also below is current CBMG director Nadir Patel (in the back) speaking at the ribbon cutting for WA Optimum with Shu Lia and Derek Muhs.

(pic credit to WA Optimum)

International Weekly Journal of Science: Nature exposed WA Optimum as an apparent offshore stem cell shop allegedly operating illegally while claiming to treat everything from Alzheimer’s to autism with fat refined stem cells at the bargain price of ~$35k+.

A world-famous Stanford autism expert had this to say about the treatments:

neurobiologist Ricardo Dolmetsch, an autism researcher at Stanford University in California, says, “The consensus in the autism research community, as well as in the stem-cell community, is that there is no scientifically valid reason for using stem cells to treat autism spectrum disorders“. He worries that, without the proper safety studies in place,the treatments could “lead to serious complications like cancer and autoimmune disease”

Hard to believe, but it actually gets more worrisome as the WA Optimum Health debacle continues:

“lists Li Lingsong, director of the Peking University Stem Cell Research Center, as a member of its (WA Optimum’s) science and technology board. Li denies this. “I have so far nothing to do with WA,” he toldNature, adding that he has asked the company to remove his name. WA also claims a strategic alliance with Harvard Medical School, althoughneither the medical school nor the Harvard Stem Cell Institute is aware of any such connection. Likewise, the University of California, Irvine, where WA claims to have research facilities, denies any formal relationship.”

Also note that WA optimum seemingly opened after the Chinese government had banned unregistered stem cell clinics. Do you feel CBMG’s founders are honest, trustworthy people who respect the law after reading this?

Just in case you don’t think all this is directly relevant, note CBMG seems to have been born out of the WA group per Hong Kong corporate records (and why did this company seemingly change its name 4 times in 15 months?)

(Chart from public HK company registry)

Just when you thought it could not get worse for the CBMG story….

Below is a Picture of John A Mattera (on the right between CBMG founders Derek Muhs and Shu Li) along with: CBMG VP of Business Development & previous CFO Andy Chanand John Mattera’s wife Lan Phan Mattera.

(pic credit from WA optimum)

The picture above was taken when the WA Optimum team invited Mr. John Mattera to become Executive Board Member and partner. Amazingly, when this picture was taken on 8/22/2011 Mattera was just months away from being arrested in 11/2011 for running a 2 year fraud and later being sentenced to 11 years in prison.

John Mattera has been jailed for fraud related charges multiple times, doing one year in FL jail as well as time in Kentucky. John Mattera just pleaded guilty for fraud and is now serving an 11 year prison sentence from accusations of everything from securities fraud to money laundering.According to the SEC lawsuit, Mattera and his crew defrauded investors of over $12.6m which:

“Mattera has simply stolen to subsidize his lavish lifestyle of private jets, luxury cars and jewelry.”

John Mattera already had four earlier convictions for fraud prior to being invited to work with the CBMG founders while literally 1 minute on Googleturns this information up immediately. How could CBMG’s Shu Li, Andy Chan and William Cao not know who this man was?

Even more concerning is if we use the WayBack Machine (remember, everything on the internet is there FOREVER) shows WA Optimum apparently offering SVF Knee Injection on their website as well as claiming to treat Liver Cirrhosis with stem cells back in March 2013 while still offering SVF treatment as well as claiming to use Autologous stem cells to treat Autism to this day.

Is WA Optimum using CBMG products through “Global Health Investment Holdings” to pursue these activities in China? While I could not confirm or deny this, it seems possible given WA Optimum’s statements on Twitter regardingCBMG’s iso facility information as if it is relevant to WA Optimum and the deep connections here with CBMG selling low volume of machines used in similar labs. If true this creates serious risk of potential financial disaster for CBMG if this is uncovered by the Chinese government, who recently stated “it would be making greater efforts to clean up the stem-cell business.”

Furthermore, recent CBMG board member Jeffrey H. AuerBack also has a questionable past including a tendency to have worked at firms FINRA expelled from the industry.

(pic credit Jeffrey Auerbach’s FINRA records page)

Among them is Westor Capital, with whom FINRA filed cease and desist (before expulsion) alleging “misappropriation and misuse of customer funds” while it appears Jeffrey had to recently settle an issue involving OTC stocks with alleged damages of $2m. Also interesting is that despite being a directorsince October 2013, Jeffrey Auerbach is listed in CBMG’s SEC filings as a director but not disclosed on their website as such?

CBMG is claiming to be running trials halfway around the world and is trusted by shareholders to honestly report the results. Based on what you have seen above do you trust what they have to say? Would you entrust your life savings with them?

But perhaps this strange team of people paying for stock promotion have accidentally stumbled on some valuable technology?

CBMG’s Autologous SVF Knee Treatment: Countless Other Companies Globally Already Doing This for Years, Technology is Worthless

In biotech unfortunately there are many unsophisticated investors who rely virtually 100% on what company management tells them without digging through the complex trials. With a company like CBMG I believe it is particularly critical to fact check what they say and make sure you understand their “technology” claims.

Let’s be clear: CBMG’s autologous fat stem cell knee injection treatment is something that has been around for many years and done around the world. In fact, the CBMG founders’ other company WA Optimum advertises they provide it right on their website.

Anyone with history in this niche will know there are literally dozens and dozens of other companies already established as the leaders in this space, many of which are already selling products and they have been financial disasters in their own right. To get you started look at Intellicel Biosciences, Tigenix here, RegenaStem, SC21, here, here, here and here. I could go on but there are countless. Assuming CBMG legitimately believes this is real, they are years behind and the service is offered cheaply all around the world already.

Dr. Mark Berman is a cosmetic surgeon from Beverly Hills, Ca who administersstem cell treatments and is one of the lead doctors at WA Health. Through WA Health, Dr. Berman is a direct associate of CBMG CEO William Cao, as we can also see in the picture below.

(pic credit WA Optimum)

Interesting from a disclosure perspective…

WA Optimum and CBMG CEO William Cao’s associate Dr. Berman is actually already administering these stem cell treatments and interestingly, he is very clear he uses the LipoKit and Maxstem units from South Korea (no CBMG products mentioned) and the whole process takes about two hours. There are even other Chinese clinics (aside from WA) that offer this, with many moreglobally.

We know these knee joint treatments are offered all around the world cheaply, and CBMG’s Shu Li, Andy Chan, Derek Muhs and William Cao are all closely associated with Dr. William Berman through WA Health. Therefore I find it interesting Dr. William Berman has publicly made his view on commercializing these treatments very clear, when discussing why big pharma does not seem interested he notes:

“it is hard to monetize and commercialize autologous cells.”

It seems this is exactly what CBMG is trying to do, though. Clearly CBMG founders believe Dr. Berman to be an expert or they would not have him as one of their lead doctors at WA. Furthermore, Dr. Berman is discussing the developed market of the US where IP protection is world class. If monetization of these processes is not viable in the US, how could it possibly be reasonable to try and do this in China where IP protection is nonexistent?

Further supporting this point, the shareholder returns for those invested in the Stem Cell OsteoArthritis companies (which all seem to be years ahead of CBMG) has been a disaster. Tigenix for example is already selling their product in Europe with real approval and collecting royalties. Despite that and during an incredible rally in biotech stocks, Tigenix shareholders have STILL lost -90% of their money.

(pic from yahoo finance)

Or IntelliCell, who stated they required no FDA approval but had filed Pre-IND in the US for SVF Osteoarthritis products last year after using their products for 5 years. The Intellicell product worked with just two ounces of fat and took only 30 minutes with worldwide patents and stated applications in osteoarthritis. Despite a biotech bull market the stock has fallen -99.7% and appears insolvent.

(from capiq)

I think we can all safely agree CBMG’s osteoarthritis pursuits are worthless, and even if they had value, CBMG could not possibly commercialize them successfully in China.

CBMG CAR-T: $1.8m cash paid, dead patients, obviously NOT worth $118m+

Reminiscent of dot-com days when a company would add “.com” to their name to see the stock soar, CBMG paid $1.8m in cash for this obscure CAR-T “technology,” and LifeTech immediately increased their price target valuation by $8.75 per share (with CBMG fully 13.2m diluted share count this is $118m in value, and recall CMBG has paid LifeTech). In response CBMG’s stock has temporarily soared, but I do not believe CBMG’s $1.8m acquisition of this questionable little technology nobody has heard of is worth $110m+.

(pic credit Saturday Night Live)

Let me explain….

Not all CAR-T therapies are created equal, and with big pharma spending billions per year on world-class CAR-T programs as they scour the tiny medical community in this oncology niche, I think it is safe to say CBMG spending $1.8m on this is probably not worth spending time elaborating on for obvious reasons. Notably, we have seen an interesting pattern countless times (OHR Pharmaceutical (NASDAQ:OHRP) is the latest example) where a random speculative biotech acquires a compound nobody cares about for a pittance, only to hype it up beyond reason, before the stock collapses on (not) surprisingly bad data.

First I note CBMG has essentially zero IP protection and the CAR-T space itself is notorious for questionable IP and intense competition. CBMG is located in perhaps the single worst country on earth for protecting IP and barely has any patents anyway. Even if this was valuable, there seems to be nothing stopping another Chinese company or hospital from stealing it.

Second, there are dozens of other companies in CAR-T trials right now, and if they are successful there is nothing stopping them from selling their drug in China or for the wealthy Chinese (only people in China who could afford this) to just fly to a country where the treatment is being administered. Similar to how some poor patients could fly to Shanghai for WA Optimum’s dubious $30k+ stem cell autism “treatments.”

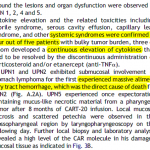

CBMG’s CAR-T acquisition is of CD19, CD20 and CD30 led by Wei Dong Han of PLA General Hospital.

The first red flag is, far as I can tell, Wei Dong Han has only published two studies on CAR-T with his other published studies spread across some pretty absurd topics including “rekindling hair loss” and some weird report studying the impact of crushing four old Chinese herbs with Diabetic Wounds. Where is the years of cancer and CAR-T expertise?

First study is involving ONE (singular) patient, aside from the fact that any study involving a single patient is clinically useless, if you read the study you will find see that the treatment seems to have quickly begun failing after just two weeks.

And even more concerning is the language about serious cytokine and immune system issues where the patient apparently died 13 weeks after treatmentafter florid disease progression occurring followed administration.

The only other published study on CAR-T from Wei Dong Han I found listed was a very confusing study. First of all, this study only enrolled 7 patients total, a number of patients that does not seem could possibly produce any statistically significant data. Second, the study looks very dangerous to me with one patient dying of “massive alimentary tract hemorrhage” while three of the patients developed continuous elevation of cytokines that had to be resolved by the discontinuous administration of corticosteroid and/or etanercept. The patients all seem to have experienced severe side effects while

The much touted sole patient to show remission we find only had residual disease to begin with! It’s pretty easy to cure a patient if he is already cured…

The other study referenced in the CBMG press release apparently had a whopping TWO patients who received the allogeneic CAR-CD19 T cell therapy, and one of them (half of that small sample) seems to me the patient died from GVHD from the treatment!

“at the onset of graft-versus-host disease (GVHD). One of those patients eventually died of GVHD, but the other gradually reached a complete hematologic remission and a partial regression of her extramedullary leukemic lesions.”

When half the patients who receive your treatment die, this is not a reason to be optimistic. Given the numerous issues here, I can see why CBMG was the only successful buyer and why it only cost them $1.8m. Aside from promotional press releases, I think this acquisition is clearly worthless.

CBMG’s CSC Joint Venture: Limited Rights in Narrow Markets With Expiring Contracts

CBMG’s TC-DC, MNP and NP are in-licensed from the curious “California Stem Cell”.

I find this aspect of CBMG most interesting as CBMG’s narrow indications and limited geography is based on Neostem’s (NASDAQ:NBS) owned technology, which NBS paid just $36m in stock for all of CSC. Furthermore, CBMG has what seems to me to be a very narrow claim on CSC technology in just a limited geography so clearly that is worth a tiny fraction of the $36m total CSC value. Despite NBS demonstrable superiority on this aspect, NBS trades for 1/5 the market cap of CBMG! If an investor is so bullish on CBMG’s involvement with CSC why not just buy NBS for 1/5 the price?

Even worse, CBMG’s rights expire in just 6 years, at which point NBS/CSC can cancel the agreement. Considering it would take CBMG at least another 3 years to finish trials, this seems like a disaster. Even more ludicrous, for the MNP/NP collaboration the contract is only at 2 year intervals and at those dates can be canceled as well. These terrible terms and worthless technology is likely why CBMG only paid CSC a $1m milestone and why NBS bought CSC outright for just $36m and paid for it nearly entirely in overvalued stock.

That is all likely to be irrelevant though, because since CBMG originally signed, CSC was acquired by NBS and NBS failed their primary endpoint and collapsed. I believe NBS is another worthless biotech promoted by Patrick Cox and others. The technology which CBMG is partially licensing has already beendeconstructed in detail and shown to be worthless so I will spare you the gory details.

CSC also has a questionable past of its own that certainly creates some doubts about its legitimacy for me. This NBS press release from 4/14/2014 states that Dr. Hans Keirstead is the current CEO of CSC. Dr. Hans Keirstead had been involved with a host of shareholder disasters and curious companies.

Most notably, Keirstead was noted as partner to International Stem Cell Corp (OTCQB:ISCO) which was also promoted and then curiously dropped byPatrick Cox, and which marketed a stem cell anti wrinkle cream. We see below that ISCO investors have lost -97.81% of their money.

Dr. Hans Keirstead also seems to have been involved in GERN, which was also a disaster for shareholders during a raging biotech bull market and has lost -55% of its value so far.

I think CSC is worthless. But if for some reason you’re wildly bullish on CSC technology, why not just buy NBS for 1/5 the price?

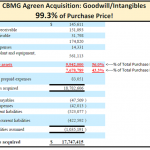

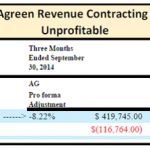

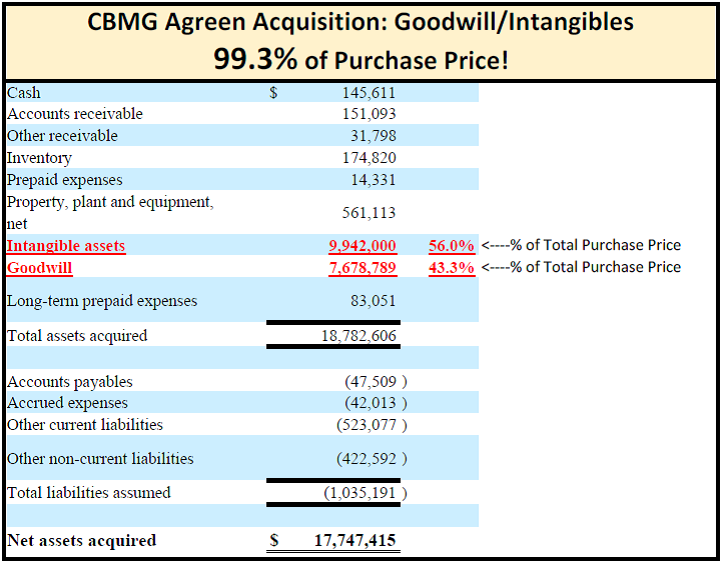

CBMG Agreen Acquisition: Defunct FL Company with Uncompetitive Offering Acquired at >16x Revenue?

CBMG’s largest acquisition to date was for “Agreen” which appears to be based off a failing FL based medical cell analysis and preparation Company run by a FL man whose listed address is this house.

I’m honestly not trying to judge because I’m not a particularly fancy person myself and I respect that. However, if Agreen had been a wild success worth $20m I think the owner would probably at least have landscapers watering his lawn?

From the CBMG purchase agreement of Agreen we can see Agreen isapparently the current interation of Biomed Immunotech, which seems to have failed in the US as it was started in 2003 but apparently not doing well 5 years later looking for subsidized office space in 2008. Repeated calls to their phone number showed not even an active voicemail, with a stale website and no updates other than an address change back in 2013 and the pricing list still from 2007. If you want to learn more about the “technology” it explains it all there but it seems this is a commodity process as there are many inexpensive competing services and products available to basically anyone that can perform this fairly basic lab function here, here, here, here and here, etc., which presumably is why Biomed failed in the US. I’m also confident if you call their old sales partners here, their sales people will be happy to show you products that can get the job done which are not from Biomed Immunotech.

Given the failed background, the acquisition price is jaw dropping. As a result, the accounting of this transaction becomes pretty tortured as in order to justify the ridiculously high price, CBMG’s accountants had to ascribe a full $17.6m or 99% of $17.7m purchase price to “goodwill and intangibles” which seems crazy because if you read the fine print of the purchase contract Agreen apparently had <$1m of registered capital (5m rmb).</p>

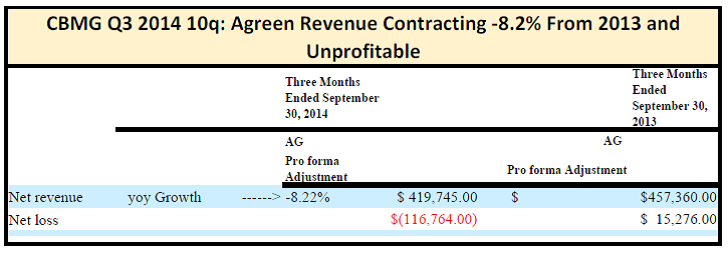

Agreen’s profits go to a Jilin hospital for awhile with only 40% to Agreen, which doesn’t even matter much since Agreen’s revenue is very small and has actually been declining and the company is losing money.

How could this possibly be worth nearly $18m? I think since this business failed in the US, it is likely to also fail in hyper competitive China where cost driven cut throat competition is everywhere and IP protection is non existent. Even more confusing is that med equipment businesses typically sell for 2-3x revenue so if you want to be optimistic, value Agreen at 3x the $1.1m in stated trailing revenue when acquired, or $3.3m total value, is a good place to start and I don’t understand how CBMG thought Agreen was possibly worth the huge price they paid.

CBMG Accounting and Financial Statement Issues

Complex BVI structures are commonly associated with fraud as are Chinese reverse mergers, with sharesleuth claiming 1 of 10 Chinese rtos in the US is fraud. With this context it is very important when investing in a company like CBMG that you can trust and understand the financials and accounting.

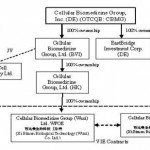

The first red flag that makes me concerned is, in my view, inexplicably complex corporate VIE structure which potentially leaves CBMG stockholders very vulnerable. Remember CBMG barely even has revenue and is a tiny speculative biotech with a small amount of cash invested where you could likely recreate their facilities for <$5m. So why exactly does this company require a spider web of a full EIGHT offshore subsidiaries around the world to operate?</p>

(from CBMG 10k)

Another red flag for me is that CBMG has been forced to restate their financials in the past while the 2013 10-K stated:

“Our disclosure controls were determined to be ineffective based on the errors and deficiencies in our internal controls over financial reporting as described below.”

Which included a lack of effective oversight of accounting function. During that same year CBMG’s auditor gave them a “going concern” statement and I estimate that of the last 8 quarterly 10q or 10k filings, CBMG has been forced to file a NT filing due to inability to complete their filings on time. While CBMG claims to have remedied some of these issues, I think this coupled with the quality of the team involved merits consideration.

CBMG’s previous auditor Tarvaran Askelon & Company was also shown by the PCAOB to have deficiencies regarding “potentially material misstatement in the audited financial statements” and “failure to perform sufficient audit procedures” and then again in the next examination a whole host of additional audit deficiencies were found.

CBMG Company Response:

I called CBMG literally more than ten times over the past weeks as I very much wanted to answer some of the questions I have. However, it appears their phone number goes straight to a voicemail and I was unable to ever get through to anyone.

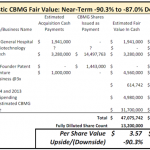

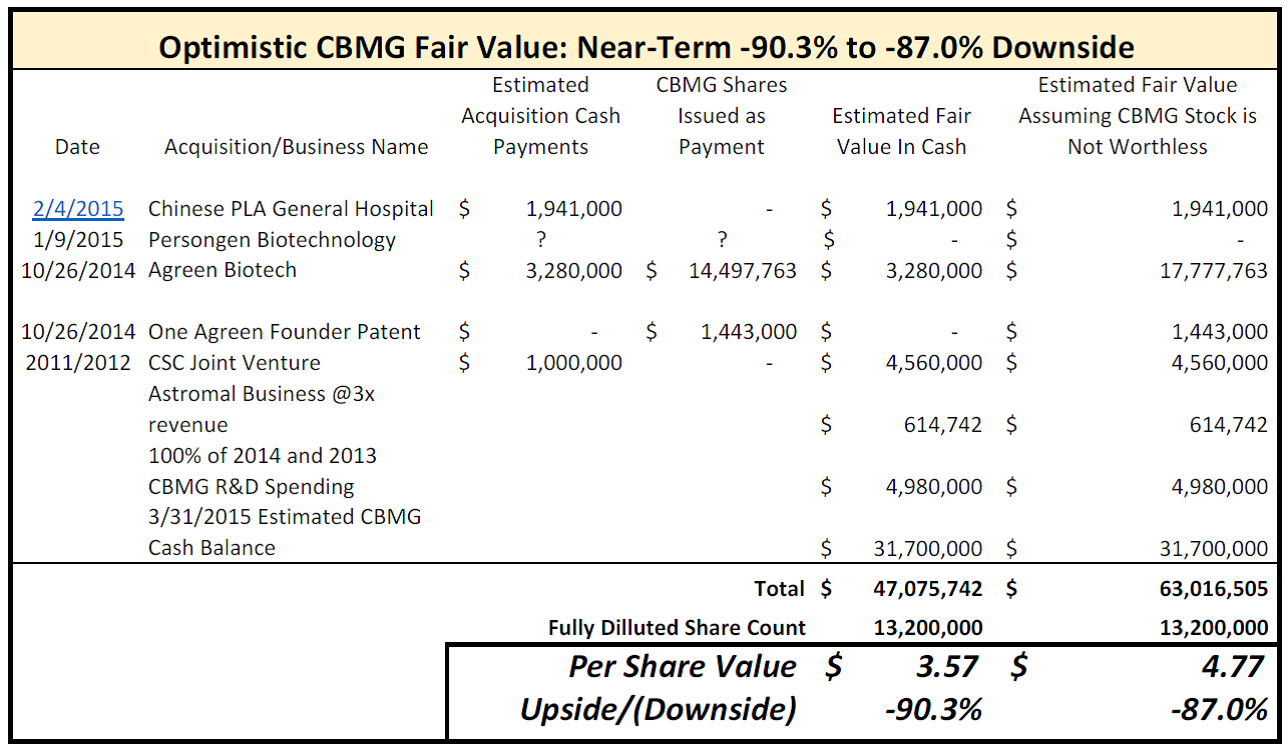

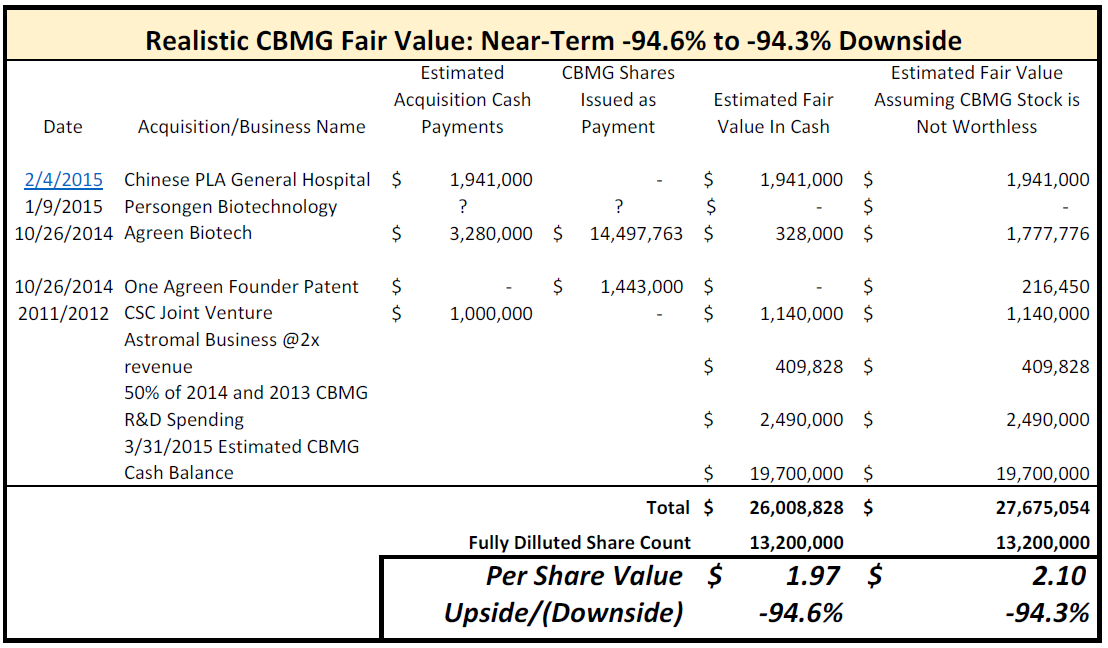

Optimistically Valuing CBMG: -87% to 94.6% Downside

In valuing CBMG I am going to make a number of very generous assumptions to demonstrate just how absurdly over valued CBMG stock has temporarily managed to achieve. In the analysis below I give CBMG credit for 100% of their R&D spending since end of 2012, and we all know R&D is probably not even worth $0.50 on the dollar. I am also going to give CBMG credit for 100% of their current cash value even though they are expected to burn $15m+ this year. I will also generously assume the lab assay Agreen business is worth the ridiculous 16x revenue CBMG paid for it and also assume the rest of their assets are worth what management paid for them. Even using this very optimistic analysis we still see CBMG has imminent near term downside of -89% if we average the two.

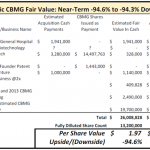

A more realistic analysis giving CBMG credit for 50% of the R&D spend, adjusting out the -$15m cash burn for 2015, valuing the Agreen and Astromal businesses at 2x revenue, discounting the Agreen patent and valuing the latest CAR-T acquisition at $0 (given patient deaths), we get an estimated fair value with -94.5% downside from today’s CBMG stock price. Note that in order to make money in stocks you typically have to buy them for a substantialdiscount to their fair value.

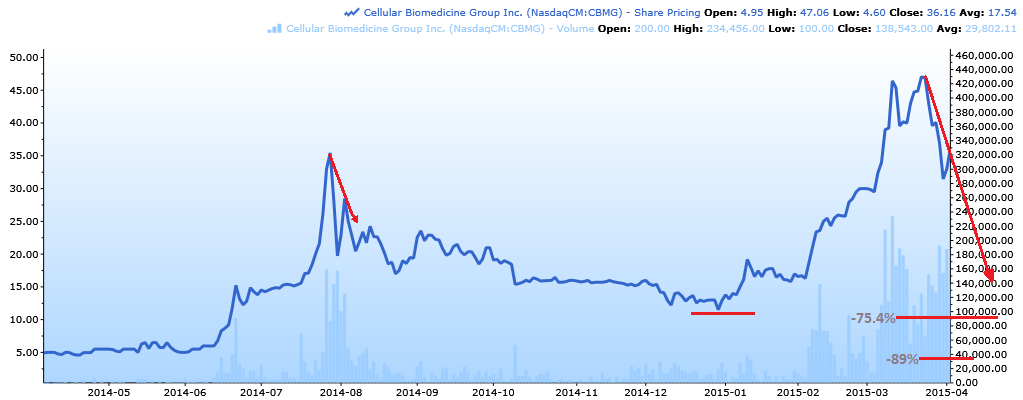

CBMG Stock Breaking Down Violently on Huge Volume

We all know what typically happens in the final innings of stocks with paid promotion and I think we are seeing that now with CBMG. CBMG stock chart is exhibiting classic technical broken-wedge pattern, note the huge increase in volume on the latest decline for confirmation. Last time CBMG stock broke down back in 2014 it fell -75% from the peak before finding support. We can see on the chart CBMG stock has no support near term until the $11 (-75.4%) area but given the shares outstanding have ballooned dramatically since then I think it’s clear the next potential support on the chart is back to the price level of $2.18 last year, for near term -89.18% downside.

These downside targets also line up well with the average -75% declines we see from LifeTech Capital stocks as well as the fundamental valuation analysis showing -90.3% downside as well.

Conclusion:

I genuinely feel bad for CBMG shareholders who may have mistakenly gotten involved because once you unravel what is behind the scenes and go through all the questionable disclosures, CBMG seems clearly worthless or at least very close. Even if you assume CBMG is an honest company, based on fundamentals alone there is at least near term -91% downside.

Furthermore, CBMG’s entire business model obviously doesn’t make sense as IP protection in China is nonexistent and I estimate CBMG has spent less than $12m in cash total for what they have acquired recently, which doesn’t come even close to justifying the ~$500m valuation. The stock has now begun breaking down violently and with insiders and large shareholders free to sell stock as benefit from stock promotion fades, I expect the stock will continue its implosion on the way towards true fundamental value of $0.00-$4.77 per share.

In my research and valuation I sincerely tried to be fair but best I can tell it seems there is virtually nothing of value at CBMG. In a nutshell I believe it is clear this group of extremely questionable people, running a weird shell structure where CBMG shareholders have limited claims to anything, only through paid stock promotion and hyping some weird and worthless acquisitions, have they temporarily convinced investors this is worth HALF A BILLION DOLLARS. This of course is absurd and is already falling apart.

On the PumpStopper “SCALE OF AWFUL” I rate CBMG a 1.41 out of 10, as CBMG Is not literally the single most awful thing I have ever seen (I’m looking at you GLRI) but CBMG gets impressively close. As a result I would like to dedicate this song to the CBMG team, because “you’ve earned it!”

*please see disclaimer on my website for relevant disclaimer and cautionary disclosures

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

About

Testing

Mail

|

Web

|

More Posts (3710)

Read this article:

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}