Do stocks really trade for fractions of a penny? Sort of | Ben Walsh

When Nick Lemann’s New Yorker profile of SEC chair Mary Jo White came out, Felix took issue with this assertion:

In 2000, the S.E.C. permitted stocks to be traded in pennies or fractions of pennies, rather than the customary eighths or thirty-seconds of a dollar. That made it easier for traders to make money by placing very large orders for very small variances in the price of a stock.

Decimalization, Felix said, meant stocks traded in penny increments, not fractions of pennies.

Who’s right?

Felix and Lemann were both sort of right, and both sort of wrong. Stocks can in fact trade in fractions of pennies, but not because of the SEC’s 2000 rule change. Or, at least, not solely because of the SEC’s 2000 rule change.

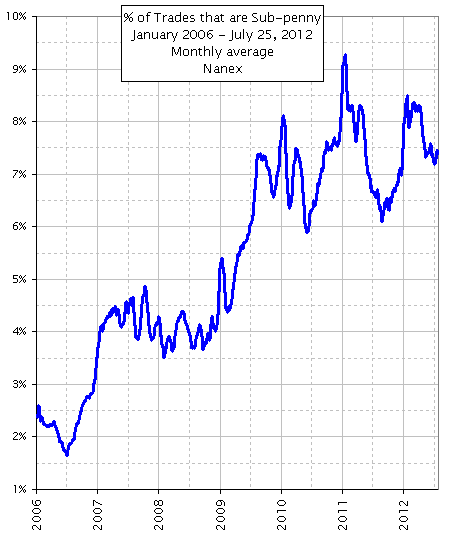

How common is it for stocks trade at sub-penny increments?

Less than 1 in 10 trades are done at sub-penny price increments. Here’s a chart from Nanex’s Eric Hunsader showing the percentage of stock trades that were executed at sub-penny increments:

Since mid-2012, there’s probably been a slight increase, but not back to the ~9.5% highs of 2011. (Also, although Eric begins his chart in 2006, the practice goes back further than that. More on that later).

How did this happen?

In 2000, the SEC allowed stocks to be quoted and traded on exchanges in penny increments. At the time, there were nine official exchanges, including not only the NYSE and Nasdaq but also anachronisms like the Cincinnati and Pacific (San Francisco) exchanges. (Exchange here has a very specific meaning: one of the exchanges registered under SEC Section 6). The change to penny increments, called decimalization, was completed on April 9, 2001. From then on, prices on exchanges were required to be quoted down to the $0.01.

Ok, but if prices on exchanges had to be in penny increments, how can stocks trade at sub-penny increments?

Interestingly, there was actually sub-penny pricing even before there was decimalization. Here’s the SEC discussing sub-penny trading as decimalization was rolled out in 2001:

For years, some electronic communication networks (“ECNs”) and Nasdaq market makers have permitted trading in increments smaller than that displayed through the Nasdaq system. This practice has continued in the decimal environment, with approximately four to six percent of trades in Nasdaq securities executed in sub-penny increments even though the quotations for these securities are at a penny increment.

What the SEC is describing is slightly complicated, but essentially is as follows: if a stock was being traded on an exchange (as strictly defined by the SEC), then post decimalization, it could trade at penny increments, but nothing smaller. Meanwhile on non-exchanges like the trading desks at broker-dealers, hedge funds with market making operations, or other electronic places like dark pools, things weren’t really changing at all. (Dark pools are defined by the SEC as “private trading systems in which participants can transact their trades without displaying quotations to the public”). Stocks traded at sub-penny prices before decimalization, and they continued to after the exchanges went to decimalization.

Why do I see stock prices down to the $0.0001 on my brokerage statement?

The vast majority of retail orders get sub-penny pricing through what is called internalization. Internalization is when a place like ETrade will fill one customer sell order with another customer buy order. For instance, one customer wants to sell Citigroup at $48.56. They have another customer that wants to buy Citi at $48.57. So, instead of sending those trades to the exchange, ETrade buys Citi from the customer that wants to sell at, say, $48.562. This is what is called priced improvement. because the seller got more than he was willing to sell for. ETrade than sells Citi to the customer who wants to buy at $48.568. Price improvement again, because the buyer pays less than he was willing to pay. Big banks operate a very similar process, rather than sending orders to the exchanges, and that’s one of the reasons exchanges have been losing market share.

Do all sub-penny trades happen off stock exchanges?

They used to, but not anymore. On July 3, 2012, the SEC issued a rule that allowed exchanges to trade stocks in tenth of a penny increments ($0.001). Under the new rule, stocks could trade at sub-penny increments if “price improving liquidity” was available at sub-penny levels. The NYSE, NASDAQ, and other exchanges, had lobbied for the change since 2010. The order allowing $0.001 pricing was originally meant to expire on July 31, 2013, but was extended until July 31, 2014.

The rule change allowed the NYSE to roll out its so-called Retail Liquidity Program (RLP), which is only available to retail customers and is the only way to get sub-penny quotes on the NYSE. Here’s the NYSE explaining how the program works:

RLP provides the potential for on-exchange price improvement to retail orders. Any NYSE or NYSE MKT member can enter an order to offer price improvement, as long as they are willing to improve the Protected Best Bid or Offer (PBBO) by at least $0.001… Anybody can see this indicator, and any approved retail order can access this liquidity. Retail liquidity takers must represent that their orders are not computer generated and originate from retail accounts.

One reason the NYSE may have ring-fenced the program in this way is because the exchange’s market makers may feel more incentivized to provide sub-penny quotes if they know they will be filled by retail orders, and not institutions. Individual investors, as a group, tend to be wrong about what they’re doing: if you take the opposite side of their trades, you tend to make money. Institutions, on the other hand, have a good chance of being smarter than you. So market makers are happier giving sub-penny prices to individuals than they are to institutions and algobots.

The NYSE is publicly positive about the program’s success thus far, but it’s unclear if it is pulling significant sub-penny volume away from non-exchanges. NASDAQ has a similar program it calls the Retail Price Improvement (RPI) Program.

Does this mean it’s easier for big investors to make money from small price changes?

No really. Contra Lemann’s assertion, smaller price increments make it harder, not easier, to capture moment-to-moment arbitrage opportunities. Buying and selling stocks just to capture the spread between the bid and ask becomes a lot less profitable when it can be measured down to the $0.0001. Historically speaking, execution costs for trading stocks — as represented by the bid-ask spread — are extremely, extremely low.

*Editor’s note: here’s the answer to a fascinating question you might not think to ask (or maybe you would, in which case good for you!). What’s the distribution of sub-penny pricing increments?

Eric Hunsader has the best look sub-penny price distribution:

Sub-penny prices are massively clustered right above and below penny increments. The result, according to Hunsader, is that “over half of all price improved trades (54%) involve an economically insignificant amount (1/10th of a cent)” or less.

Original source:

Do stocks really trade for fractions of a penny? Sort of | Ben Walsh

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}