Does Earnings Growth Matter When it Comes to Stocks Trading …

Does Earnings Growth Matter When it Comes to Stocks Trading Below Liquidation Value?

By:

| Fri, Jun 20, 2014

The retail public enjoys the storytelling of growth stocks and the financial

press is more than happy to fill that void. It is easy for an investor to fall

into what finance professor, Jeremy Siegel, refers to as a “growth trap”, focusing

on stocks with rapid sales and earnings growth in new industries that are highly

disruptive. Humans have a predisposition to see patterns where none exist.

Connecting the dots and extrapolating above average growth trends far into

the future is an example of this pattern seeking behavior. Let’s take a look

at the evidence and see if past growth in earnings really does continue into

the future for stocks we want to invest in.

My former professor, Dr. Josef Lakonishok, reviewed the performance of stocks

that exhibit above average earnings growth over the recent past and found very

few of them were able to maintain this stellar earnings trajectory. Over the

study period 1951-1997, firms that managed to have a 5 year track record in

the upper 25% in terms of past earnings growth, only around 2% of them went

on to stay above the median firm growth rate during the next 5 year period.[1] Although

the retail public is enamored with growth and is handicapped in seeing growth

patterns where none exist, the evidence doesn’t seem to show an ability to

predict what companies will continue on with above average growth.

Predicting what high growth companies will continue their above average growth

trajectory is difficult. Can we tip the odds in our favor by including additional

filtering rules to be able to predict what high growth companies deliver above

average earnings growth into the future? Unfortunately, additional filters

such as size or book-to-market screens applied to high earnings companies still

fizzle out in terms of delivering those select stocks that continue on with

above average growth into the future. After 4 years, only around 2-3% of high

growth companies that are screened based on size or book-to-market continue

to stay above the median growth rate in terms of earnings. Practically none

of these companies still maintain a sales or earnings growth rate above the

median after a decade.[2]

So what if the earnings growth dwindles over time for companies that produced

above average growth in the recent past. If they outperform the broad market

average, aren’t they still worth buying? Not if you use only earnings-per-share

growth as your buying criterion. O’Shaughnessy in his book, What Works on

Wall Street, showed that a portfolio of 50 stocks with the highest previous

5 year earnings-per-share growth rate lagged the market over a 50 year study

period. Even breaking down the long study period into rolling 5 year periods,

growth companies still lagged the broad market average most of the time.[3]

So in summary, earnings growth can’t be predicted and purchasing historical

high growth stocks doesn’t seem to outperform the market over the long term.

What should investors do in terms of a rationale process that would be a better

use of their investment capital. The answer is invest in stocks trading below

liquidation value and abandon the earnings forecasting game all together.

By focusing your data mining activity not on the income statement, but on

the balance sheet of public companies, a better performance result is delivered.

A selection criterion outlined by value investing pioneer, Benjamin Graham,

called for purchasing stocks trading below net current asset value, an approximate

measure of the liquidation value of a public company. This criterion calls

for subtracting all liabilities including preferred stock from the current

assets listed on a company’s balance sheet. If this measure of liquidation

value of a company is significantly greater than the market value, purchase

the stock.

Below shows the average performance of stocks trading below 75% of net current

asset value over the 1956-2009 study period. No more than 10% was invested

in any one stock. If only a few stocks were available that met this stringent

value investing criterion, the balance of the portfolio remained in Treasury

Bills. As indicated on the graph, even with a portion of the portfolio being

handicapped by sitting idle in Treasury Bills, the long term performance is

excellent relative to a broad market average.

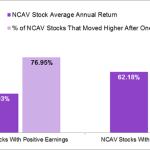

We know that stocks trading below liquidation value have good historical performance

regardless whether earnings are positive or negative. The chart below looks

at all stocks trading below 75% of net current asset value and divides them

into two groups: ones with positive earnings over the previous year and the

others with negative earnings. Both groups perform well, but the ones with

earnings losses over the previous year perform even better. This same conclusion

is also supported in another study by Tobias Carlisle and his colleagues showing

monthly returns of negative earnings companies that trade below 2/3rds of net

current asset value outperform ones with positive earnings.[4]

Unfortunately, the superior performance of net current asset value stocks

that lost money over the previous year comes with a price. As the chart shows,

a smaller percentage of stocks trading below net current asset value with negative

earnings increased their share price after a year. Average annual returns are

better for NCAV stocks that lost money in the past year, but only 57% of them

moved higher in price.

For investors willing to embrace a value investment philosophy and purchase

only stocks trading below net current asset value, it is better to focus on

the balance sheet of a company rather than earnings summarized on the income

statement. Stocks whose most liquid assets on the balance sheet exceed all

liabilities manage to outperform the broad market average over the long study

period from 1956-2009. Earnings growth is not only difficult to predict in

the future, but as a stand alone selection criterion it doesn’t add much value

in terms of superior portfolio performance. The long term evidence shows that

selecting stocks trading below net current asset value is a better use of your

time and energy than chasing the next earnings momentum stock touted by the

financial press.

[1] Louis K. C. Chan,

Jason Karceski and Josef Lakonishok. “The Level and Persistence of Growth Rates.” Journal

of Finance 58, no. 2 (April 2003): 660-661.

[2] Louis K. C. Chan,

Jason Karceski and Josef Lakonishok. “The Level and Persistence of Growth Rates.” Journal

of Finance 58, no. 2 (April 2003): 656.

[3] James P. O’Shaughnessy,

What Works on Wall Street, (New York: McGraw-Hill, 1998), 191-196.

[4] Tobias Carlisle, Sunil

Mohanty and Jeffrey Oxman. “Ben Graham’s Net Nets: Seventy-Five Years Old and

Outperforming.” February, 2010. Accessed June 10th, 2014. http://eyquemdotnet.files.wordpress.com/2013/09/benjamin-grahams-net-nets-seventy-five-years-old-and-outperforming-full-tables1.pdf.

Please enable JavaScript to view the comments powered by Disqus.

Author: Victor Wendl

Victor J. Wendl

President

wendlfinancial.com

Important Disclosure: Victor Wendl is the author of The Net Current

Asset Value Approach to Stock Investing. The book reviews the performance

over a 60 year time period of purchasing stocks trading below net current

asset value. The stock filtering criterion was popularized by Benjamin Graham,

the father of value investing, and a mentor to Warren Buffett who considered

his professor and former employer one of the most influential people in his

life. The Net Current Asset Value Approach to Stock Investing is available

for purchase on Amazon.com,

as well as for Nook and Kindle reading

devices.

Wendl Financial, Inc. is registered as an investment adviser with the state

of Missouri and only conducts business in states where it is properly registered,

or is excluded or exempted from registration requirements. Registration as

an investment adviser does not constitute an endorsement of the firm by securities

regulators. The information in this article is for general information purposes

only and should not be construed as personalized investment advice.

You must be aware of the risks and be willing to accept them in order to invest

in the stock market. Don’t trade with money you can’t afford to lose. This

is neither a solicitation nor an offer to buy stocks. No representation is

being made that any account will or is likely to achieve profits or losses

similar to those discussed on this Web site. The past performance of any trading

system or methodology is not necessarily indicative of future results. No representation

is being made that any account will or is likely to achieve profits or losses

similar to those shown.

Past performance results is not an indication of future performance. Wendl

Financial shall have no liability of whatever nature in respect of any claims,

damages, loss, or expense arising out of or in connection with the reliance

by you on the contents of our website.

Copyright © 2014 Victor Wendl

All Images, XHTML Renderings, and Source Code Copyright © Safehaven.com

Read the article –

Does Earnings Growth Matter When it Comes to Stocks Trading …

See which stocks are being affected by Social Media