GigOptix: A High-Speed Stock Trading At A Low-Speed Valuation …

Summary

The last straw for investors concerned about slowing growth and margin compression may have been the recent doubling of the authorized share count in connection with a recently failed acquisition.

Authorized shares are not the same as actual shares; concerns are overplayed given the recent top line growth, stable gross margins and the highest EBITDA in company history.

The fact that management walked away after GSI Technology refused to engage reinforces the disciplined M&A strategy that has helped fuel growth.

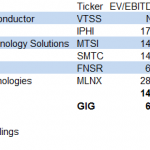

The 6.8x EBITDA multiple is significantly below the peer group median and provides a margin of safety.

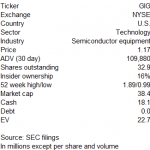

The failed deal may be an opportunity for another tender offer that could easily be funded given the $18.1 million of cash and no debt.

Company overview

GigOptix (NYSEMKT:GIG) is a fabless supplier of high-speed semiconductor components that enable end-to-end information streaming over optical and wireless networks. The products are used in the telecom, datacom, consumer electronics, defense and industrial electronics markets.

The high-speed communications (HSC) product line (69% of LTM revenue) provides high performance optical and wireless components including mixed signal radio frequency integrated circuits, 10 to 400 gigabit per second (or Gbps) laser/optical drivers and transimpedance amplifiers (TIA), power amplifiers and transceivers, integrated systems in a package solutions and radio frequency chips.

The industrial product line (31% of LTM revenue) provides digital and mixed-signal application specific integrated circuit solutions for industrial, military, avionics, medical and communications markets.

GIG trades near a 52-week low (and down ~40% since the high this spring) due to concerns regarding the sustainability of datacom growth (revenue quadrupled over the past few years), margin compression from the increase in commercialization and persistent lack of profitability on a GAAP basis despite the recent impressive top line growth. Specifically, although non-GAAP net income of $730,000 was the highest in company history in Q3’14, on a GAAP basis there was a net loss of $786,000 due largely to high stock comp (~$1 million quarterly run rate).

The last straw may have been the doubling of the authorized share count to 100 million in connection with the planned acquisition of GSI Technology announced in August 2014. However, the offer was withdrawn last month after the board of GSI Technology refused to engage and even implemented an expensive executive retention and severance plan in response.

However, the fact that GIG was willing to walk away (and did) rather than negotiate against itself (by raising the $6.50 per share offer – the same price as GSI Technology’s recently completed Dutch tender offer) or waste more time is actually encouraging for two reasons. First, this highlights the disciplined M&A strategy (focus on complementary targets that can be swiftly integrated), which has played a major role in the growth of GIG (six acquisitions since inception in 2007). Second, although this acquisition would have accelerated growth (revenue/cost synergies by combining high-performance memory products with high-speed communications components), going forward prospects remain bullish even on a standalone basis.

For example, in Q3’14, revenue increased 16% y-y (and 6% sequentially; above the high end of previous guidance), gross margins remained high at 59% and management projected 2014 revenue growth of ~12% on the Q3’14 conference call due to continued strong demand for HSC/industrial products.

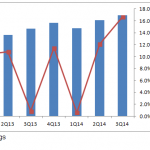

EBITDA increased to a record $1.4 million from $0.1 million (and the 13th consecutive quarter of EBITDA profitability; see chart below) due to this top line growth and lower cost structure as a result of multiple restructurings (lower headcount, relocation of manufacturing activities) over the past two years. As management tracks towards the 15-20% operating margin target (from 8% in Q3’14) over the next 3-5 years, this should enable utilization of the ~$42.9 million of federal NOLs (although they begin expiring this year).

The long-term bullish outlook is supported by multiple growth drivers, including the following:

M&A/JV. Through a Brazilian joint venture (BrPhotonics) announced in February 2014, GIG entered the silicon photonics market, in which revenue is projected to grow at a 24.5% CAGR to $411 million in 2020 due to the growth of cloud services, entertainment on-demand and big data processing.

An example of how the previously discussed successful M&A strategy is fueling growth is Tahoe RF Semiconductor, which was only acquired in June 2014, yet GIG announced a month later, a new global navigation satellite system (GNSS) RF Receiver developed by this team. Annual shipments in the GNSS industrial market (road, maritime, agriculture and surveying applications) are expected to grow 67% to 43 million devices.

New products. Although the contribution from the telecom side should gradually diminish compared to datacom (see below), growth on an absolute basis remains strong. In Q3’14, revenue increased 49% sequentially due to the introduction of a new 100 Gbps driver, while for the past two years, GIG shipped more 100 Gbps drivers than all of its competitors combined.

In February 2014, GIG introduced a new family of TIA products aimed at the consumer electronics markets where shipments for gesture sensing solutions used in smart devices such as smartphones, smart TVs, game consoles and PCs are projected to grow from <250 million units in 2014 to >1.8 billion units in 2018.

The increasing secular demand for bandwidth is responsible for the projected ~2x increase in datacom revenue in 2014 to >$8 million (which exceeded telecom revenue for the first time ever in Q2’14) and almost 2x increase in wireless revenue while the large total addressable markets provide plenty of white space.

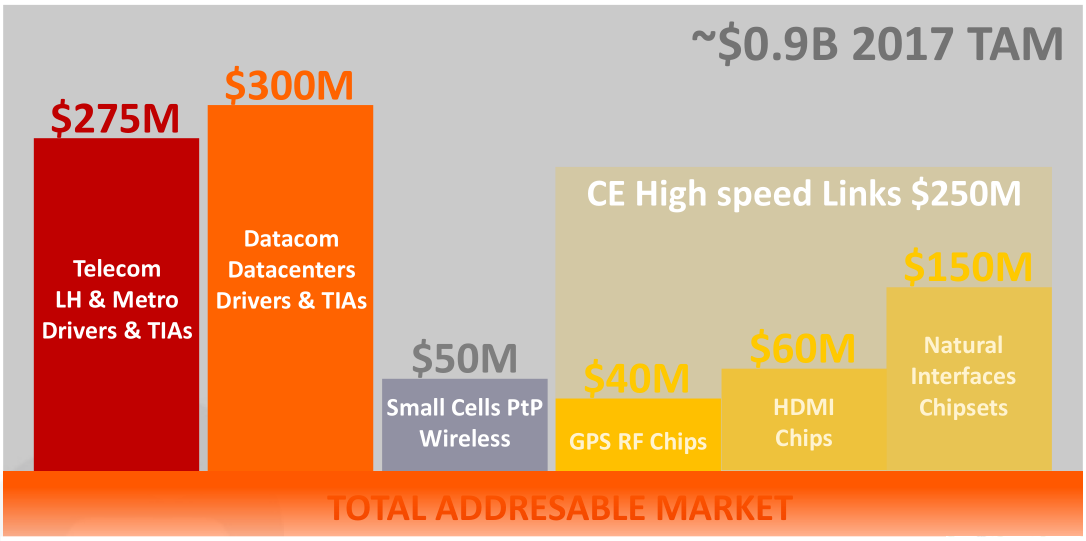

Source: Company presentation

GIG has multiple competitive advantages including proprietary technology (>100 patents), a broad product line that offers customers one-stop shopping and a long history of offering products that exceed customer performance, power, size, temperature and reliability requirements.

Risks

There is a fair degree of customer concentration (one accounted for 28% of revenue in the YTD period) due to the small number of network systems vendors.

GIG has a history of losses on a GAAP basis, which have been partly funded through equity issuance (the most recent being the sale of 9.6 million shares in December 2013). The outlook for cash burn in the short term is neutral as management projected an unchanged cash balance in Q4’14, while over the longer term, cash flow should improve due to the continued growth.

A downside of the fabless model is the potential for disruption due to quality or performance failures by its outsourcing partners.

The semiconductor industry is highly cyclical, subject to rapid technological change and provides little visibility while a downturn would likely result in inventory buildup and lower average selling prices (or ASPs). Competition is expected to increase due to consolidation as well as larger semiconductor companies (including OEMs) entering the marketplace.

A poison pill (with a low trigger at 10%) and staggered board may discourage activists who may be otherwise attracted to the positive fundamentals.

Valuation and price target

As shown in the chart below, GIG trades at an attractive absolute and relative valuation, which provides a significant margin of safety given the previously discussed concerns.

Investors appear to be equating a doubling of the authorized share count with the actual share count as the former merely provides flexibility and does not require GIG to issue more shares. Moreover, any new shares issued will most likely be used for an accretive deal (the GSI Technology acquisition would have been immediately accretive on an EBITDA basis) rather than to simply establish a rainy day fund.

The failure to consummate a deal may actually be a blessing in disguise for shareholders as the board could use it as an opportunity to conduct a tender offer similar to the one in May 2012 in which ~700,000 shares were repurchased. This option has zero execution risk, still puts to work the “lazy” balance sheet ($18.1 million of cash and no debt) and takes advantage of the depressed share price.

The price target of ~$1.70 (to be reached over the next 12-24 months) is based on a 12.5x EBITDA multiple.

From a technical standpoint, the stop loss should be placed below the recent low at $0.99. From a fundamental standpoint, investors should watch for signs of price erosion (in the form of lower ASPs or gross margin compression), a meaningful deceleration of growth in datacom (key in on sequential revenue growth) and progress towards becoming profitable on a GAAP basis. The first opportunity to evaluate the investment thesis will be the Q4’14 conference call, when management is expected to provide an updated 2015 outlook.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Source:

GigOptix: A High-Speed Stock Trading At A Low-Speed Valuation

Disclosure: The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it (other than from Seeking Alpha). The author has no business relationship with any company whose stock is mentioned in this article. (More…)

Jump to original:

GigOptix: A High-Speed Stock Trading At A Low-Speed Valuation …

{kind=link}

{kind=link}