Gold and Silver Sentiments Violently Diverged in 2013 | Zero Hedge

by Keith Weiner

There are two reasons why people buy gold and silver. The first is that they’re the monetary metals. Many people don’t want more than a certain exposure to the risks of the banking system. They hold dollars for liquidity and beyond that exchange them for metallic money. This money is not for trading.

The second is to trade or, more specifically, to speculate. They buy with the expectation of a rising price. The gold price, measured in dollars, is really just the inverse of the dollar price measured in gold. As the Fed abuses its credit, the quality of its liability falls. This liability—the dollar—has been falling in quality and price for 100 years. Measured in gold, the dollar is now just under 26mg. Or, measured in silver, it’s around 1.6 grams. Most people look at the inverse, the dollar prices of the metals, currently around $1200 and $19.50.

It makes for a great speculation, that the dollar will continue to fall. At least, it did until 2011. The gold price peaked in 2011 at $1900, and has since dropped 37%. The silver price dropped 60%.

One speculation strategy is to buy when something is going up. Today, there is clearly no upward momentum in gold and silver. The other approach is to try to buy when there’s blood in the streets, as the old trader’s saying goes. OK, but is there blood in the gold and silver streets?

I write the Monetary Metals Supply and Demand Report, a free weekly letter that provides data and analysis of the constantly changing fundamentals of the gold and silver markets. The data shows that gold is significantly scarcer to the market than silver; gold has a small backwardation and silver does not.

For months, I have discussed my hunch that there just has not been the final capitulation in silver as in gold. I have seen the comments on my own and other articles, and in other online forums.

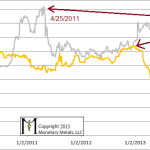

I couldn’t prove it, but it kept nagging at me. Then I put together this graph of inventory held in the two big Exchange Traded Funds: GLD and SLV.

Tonnes of Metal Held by the ETFs, Jan 2009 through Dec 2013

The picture in gold is what you’d expect. Gold metal begins to move out of the GLD inventories around the start of this year, and it has been almost a straight move down. There is no sign yet of a bottom. Gold inventory is down 40% from its peak one year ago.

Silver violently diverged. As one might expect, silver held by SLV peaked on April 25, 2011, the day the price peaked. Metal began moving out of the ETF the next day. The level quickly dropped by 14%, but then stopped falling. Then, at the end of 2012, inventory began to rise. Though the silver price is down 60%, silver holdings are down only 9%.

The reason for metal to flow in or out of an ETF is counterintuitive. It has nothing to do with price moves. The flow of metal depends entirely on the spread between the prices of the ETF and the metal itself. Arbitrageurs buy metal and sell new shares, whenever the share price is above the metal price. They sell metal and buy back shares when the share price is lower.

The graph shows a one-way flow of gold out of GLD. This means that the price of GLD shares has consistently sagged below the price of gold. This corresponds to negative sentiment regarding this metal. By contrast, more metal has flowing into SLV than out.

In general, I caution against just this sort of analysis. It is easy to focus on a highly visible corner of the market and ignore numerous low-profile corners. Both gold and silver have vast inventories; there is no such thing as a shortage or a glut. Metal can move from one corner to the other without necessarily impacting price or anything else.

But in this case, the reason to study this chart is to understand sentiment among speculators. I suggest that sentiment in silver has not made its nadir, and that silver speculators yet cling to hope against hope that its price will shoot to the moon.

The irony is that my statement is controversial and contra the accepted wisdom in the silver community. If speculators had turned truly pessimistic about silver, then my statement would be uncontroversial, but advising people to buy silver would spark controversy.

One can never be certain about sentiment changes, but it’s a strong possibility that silver speculator pessimism rises to match that in gold. If this happens, the silver price could drop several more dollars. This is a time to be cautious with silver, though I never advise naked shorting a monetary metal.

(C) 2013 Monetary Metals

Average:

3.727275

Your rating: None Average: 3.7 (11 votes)

Originally posted here:

Gold and Silver Sentiments Violently Diverged in 2013 | Zero Hedge