Gold Stocks: The Great Contrarian Trade Of 2014? | Zero Hedge

In my experience, one of the singular best investment strategies is to buy assets/asset classes which are most reviled by investors. By reviled, I mean assets where a mere mention of you wanting to invest in them generates nervous sniggers among others, if not howling laughter. Where upon their mention, people hand you business cards, not their own but of nearby psychiatric centres. And where even friends start to doubt your sanity.

Examples include the Indian rupee, in free fall just four months ago on QE taper speculation and current account issues. It’s up 12% versus the U.S. dollar since bottoming, as shown below.

European stocks and bonds in mid-2011 too. At that time, European stocks neared 2008 lows amid concern about a possible European Union break-up. Since then, the Euro Stoxx index is up ~45%. And investors are now clamouring for their piece of Europe.

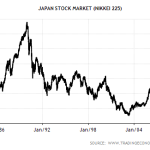

Then there’s Japanese stocks. In mid-2012, there wasn’t a more hated asset class. A 22-year bear market, with stocks down almost 80% from peaks reached in 1990. Since mid-2012 though, the Japanese stock market doubled before recently pulling back.

It’s worth asking then where the next great contrarian trade may be? Some investors are pushing emerging market stocks as they scour for laggards in a maturing bull market. While others are suggesting emerging market bonds may be worth pursuing for similar performance/valuation reasons. Both of these ideas have some merit but they probably don’t quite qualify as true contrarian trades.

No, instead, Asia Confidential thinks commodities may be a more prospective potential area. More specifically, gold stocks, or better yet, junior gold stocks. The junior gold miners have been obliterated, down around 80% since the 2011 peak. Causes include a declining gold price, production shortfalls, cost blow-outs, dilutive capital raises and too many snake oil salesmen disguised as CEOs.

There are signs though that some of these things may be turning around: bad management is being given the boot, capital expenditure programs are getting slashed, fewer capital raises are taking place given a lack of market appetite and boards are placing greater weight on shareholder returns over growth. Moreover, the valuations of many quality junior gold miners appear compelling. A number are discounting gold prices of less than US$700/ounce into perpetuity. That means even if gold prices don’t rise from here, the downside on these stocks seems relatively limited. Higher gold prices would just be gravy.

Gold: where too from here?

The gold price has had a tremendous run that’s about to end. It’s been up for 12 straight years in U.S. dollar terms. Unless something dramatic happens, that incredible record will end in 2013.

Regular readers will know that I remain relatively bullish on gold in the long-term. But I’m not dogmatic about it. There’s nothing certain in this world and that includes the future of the gold price.

And there are a number of things which should concern gold bulls at this point. In my view, there are two key drivers for gold prices:

1) The so-called fear trade. That is, the prospect of the financial system breaking down and currencies again being backed by gold.

2) Negative real bond yields. Thereby the opportunity cost of holding gold is negative.

Both of these factors are turning, making gold appear a less attractive asset. At least for now.

Supply and demand for gold also appears to be turning unfavourable. The World Gold Council says gold mining production increased by 4% in the third quarter versus a year ago. Residual gold projects are still going ahead even though the gold price has headed south. It’s true that overall gold supply declined in the third quarter due to reduced recycling, but still…

And demand for gold is softening. Particularly in what was recently the world’s biggest gold market, India. The Indian government has implemented higher excise duties and import payment restrictions. It’s done this to reduce gold imports and thereby improve the country’s current account balance (which is in serious deficit and hurting the currency).

The government’s actions resulted in gold demand in India slumping 32% in the third quarter of this year. And there could well be steeper falls in the fourth quarter. India now accounts for 21% of total gold demand versus a five-year average of 38%.

Lastly, gold bulls have been in denial about the enormous technical damage done to the gold price mid this year. There are a number of respected technical analysts previously positive on gold who believe the damage was such that it marks the end of the bull market.

So is it all doom and gloom for the yellow metal then? Not quite. We’re of the view that the financial system is more vulnerable today than during 2008 due to the extraordinary policies initiated by central banks around the world. No-one knows what the end-result of these policies will be, including the central bankers.

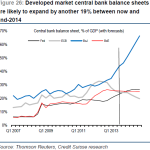

Those extraordinary policies will continue through 2014. Even with potential U.S. QE tapering, other countries are expected to pick up the slack. Credit Suisse estimates developed markets will expand their balance sheets by a further 19% by end-next year.

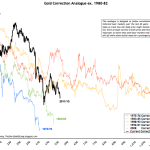

More importantly, the recent drop in the gold price from the highs of September 2011 isn’t out of the ordinary. In fact, similar falls have occurred during every gold bull market of the past century. This time, the price declines haven’t been as steep as the mid-1970s, but they’ve lasted longer, as highlighted in a recent post by The Daily Gold.

Lastly, gold valuations don’t appear elevated. The current price remains way below the 1980 inflation-adjusted peak price of close to US$2,400/ounce. You can also value the gold price assuming the world reverts back to a gold standard. With approximately 12.5 trillion in physical and electronic currency reserves and around 155,000 metric tonnes of gold above ground, that results in a gold price of US$2,500/ounce if all of the world’s reserves were to be backed by above-ground physical gold.

Gold bugs could well yet have the last laugh…

Why gold miners are so hated

Show me a bull market and I’ll show you a good time. And gold mining companies had a great time up to 2011, often at the expense of their shareholders. That resulted in serious under-performance versus the physical metal.

Production misses became the norm rather than the exception. Gold ore grades disappointed, along with the fluff known as sales estimates from companies.

Managements of gold companies spent ridiculous sums during 2010-2011 after getting false signals on demand from the massive stimulus package out of China. National Bank Financial in Canada estimates global capital expenditure/tonne/day increased by close to 10% p.a. in the seven years to 2011.

Also, cost blow-outs were a recurring theme. CIBC estimates cash costs/tonne increased by 80% in the six years to 2012. Resource nationalism didn’t help the cause as countries increased taxes to get their slice of the large pie.

And equity issuance skyrocketed. It peaked at US$120 billion globally in 2009, up from less than US$20 billion in 2005.

As gold prices pulled back from September 2011, to say that gold miners became a hated breed would be an understatement. Institutional shareholders wanted blood and got it. A quarter of CEOs at Canada’s top 20 gold mining companies were turned over in 2012 alone.

Uneconomic projects were shut down. Capital expenditure budgets were slashed, and exploration along with it. Offices were closed down. Costs of undertaking mining were trimmed.

Dividend payout ratios were raised. And stricter return on capital targets were enforced.

In sum, an undisciplined industry full of cowboys has had to shape up. And previously sleepy boards and shareholders are scrutinising their every move.

Overall, the changes are very positive for future prospects.

Which miners appear ok value

There are three ways to play gold mining companies. You can bet on those exploring but not yet producing. These are the high risk but highest reward options.

You can bet on higher gold prices and invest in gold producers where current prices are making their projects uneconomic. Thereby if prices rise, these projects will make decent profits and depressed share prices should react accordingly.

The safest route is to invest in producing companies with long-life, low cost assets. Ideally with shareholder-focused management and minimal debt. These companies may not benefit as much from rising spot prices, but will hold up much better if prices remain under pressure.

We prefer the safest option but are not adverse to alternatives should the price be cheap enough.

There is plenty of value on offer with the large mining producers. The share prices of most of these companies have been smashed. For instance, the world’s largest gold producer, Barrick Gold (NYSE: ABX) in Canada, trades on just 3.5x forward cash flow. This is a company with several high quality, low cost assets. Yes, management has done some dumb things, but the valuation is extraordinarily depressed. This article makes a good case for Barrick.

In our neighbourhood, Newcrest Mining (ASX: NCM) in Australia, is worth looking at, perhaps at slighter lower levels. The company has two of the world’s seven largest gold mines. The company’s share price is down ~75% from the peak given years of mismanagement. Current prices factor in a gold price of around US$950/ounce into perpetuity. Cheap, but not obscenely cheap.

To get the more obscenely cheap, you need to look at companies with smaller market capitalisations. The so-called junior gold stocks. We like Medusa Mining (ASX: MML), an Australian-based company with mostly Asian assets. It’s the lowest cost Australian gold producer, with fantastic future production growth and minimal debt to boot. It also trades at valuations which discount a gold price of close to US$700/ounce into perpetuity (this via conservative discounted cash flows, the maths of which I won’t bore you with here).

Among the gold exploration companies, there are many which look stupidly cheap. Bob Moriarty at 321gold does a great job hunting them down. He’s been banging on a Canadian-based company, Novo Resources (CNSX: NVO), for a while and with good reason. It’s a junior with a mine which could contain the world’s largest gold deposit. It helps that the astute, Newmont Mining, recently took a 35% stake in the company. The upside appears enormous even if deposit estimates are half right.

These are but a few ideas. Of course, you could always take the easy option and buy the US-based ETF of junior gold mining companies too (NYSE: GDXJ).

Caveats

Now, a post on gold miners would be remiss without certain caveats:

In the short-term, the technical picture on gold looks shaky and that could mean spot prices head down towards US$1,000/ounce. If you buy gold miners, you take on that risk.

Gold miners are leveraged ways to play gold. That means they should outperform spot prices on the upside but also underperform on the downside.

Beaten down stocks can stay beaten down for a long time. Look at Japan. Gold stocks could well be in that camp.

Don’t rely on others, including your author, for stock tips. Do your own homework.

This post was originally published at Asia Confidential: http://asiaconf.com/

Average:

5

Your rating: None Average: 5 (3 votes)

Source:

Gold Stocks: The Great Contrarian Trade Of 2014? | Zero Hedge

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}