Has The Stock Market Become Dysfunctional? [SPDR S&P 500 ETF …

While it’s great fun and can be extremely rewarding to play the stock market (our own tips have performed pretty well as well), the main function of the stock market is to allocate capital.

The joint stock company with public listing of shares started in our native Amsterdam at the beginnings of the 17th century, and it was clearly a very useful institutional innovation as it allowed companies to tap risk capital and investors cheaper ways to diversify and liquidate.

However, despite enormous growth, the stock markets isn’t without its critics, especially in its recent incarnation. A first remarkable thing to notice is that if a market listing is so wonderful, why don’t more companies list?

There are 2.34m companies in the UK, but only 1,904 quoted on the stock market. That’s less than one in a thousand. Professor Ljunqvist says the proportion is similar in the US. [Investors Chronicle]

So for 99.9% of the companies, the cost of listing (depending on the platform) are apparently outweighing the benefits. But the remarkable facts don’t stop just there (from the same IC article):

In the US, things have been worse. In the last 10 years, non-financial companies have been net buyers of shares – to the tune of $345bn (£225bn) a year on average.

This is a remarkable figure, especially considering that there has been a rather terrible recession in those 10 years, and sub-par economic growth after it. More importantly, it seems to indicate that the stock market has lost its primary function, that as an efficient way to fund enterprise.

Now, you could argue that the last 10 years haven’t been ‘normal’ circumstances:

Companies have (recession years apart) been very profitable and flushed with cashDeleveraging households produced subdued demand and excess capacity, so little incentive to invest and expand production capacityDeleveraging households produced excess savings and record low interest rates, making alternative routes of financing more attractive (indeed, Icahn is urging Apple to borrow money in order to buy back shares!), although deleveraging banks, reluctant to provide credit, might have clogged this to some extent.

So it remains to be seen whether this is a long-term trend or just an aberration, albeit one that has lasted for a decade already. But there is more. According to research by Ljunqvist, Asker and Farre-Mensa of the HBS, companies that are listed on the stock market invest substantially less than private companies.

The difference, they found, is most pronounced in industries where share prices are most sensitive to fluctuations in current earnings. This, they say, suggests that listed companies are victims of short-termism. Managers try to impress investors by maintaining short-term earnings, and they do so by avoiding the costs of capital spending and by neglecting long-term projects. [Investor Chronicle]

The short-term focus of the stock market was an issue which used to be put forward by people who were against ‘Anglo-Saxon’ shareholder capitalism, and in favor of ‘patient capital’ stakeholder capitalism. These people used to point out that whilst the US was very good at innovating (the transistor, integrated circuits, etc.), other countries (like Japan) used to have the patient capital and institutions to build industries on these.

After Japan bubbled itself out of contention in the late 1980s, early 1990s, these arguments largely disappeared from the limelight, but that doesn’t mean there wasn’t anything in them. Speaking of innovation.

Start-up capital

The stock market still functions as a means for financing start-ups, although not really in the first stages. These seems to have been taken over for quite some time already by angel investors and venture capital, although one could argue that venture capital wouldn’t nearly as interested in start-ups if there wasn’t the efficient route of receiving a return on their investment via IPO’s.

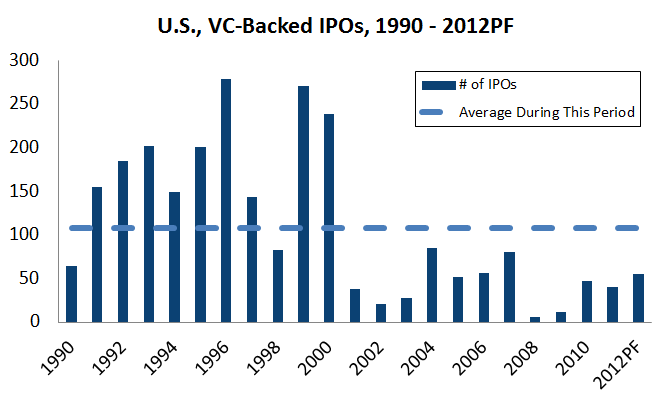

But even the IPO market is down considerably from the 1990s:

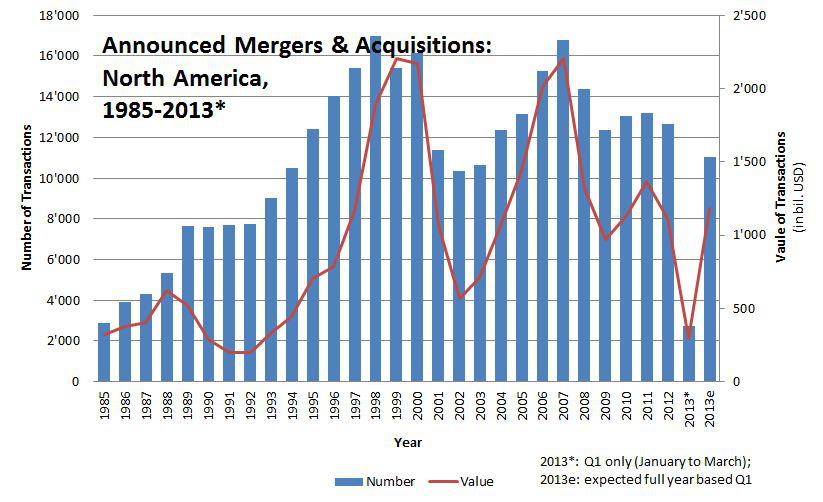

Instead, mergers and acquisitions have grown considerably and there can be little doubt that a public market makes that process a lot easier.

(click to enlarge)

But whether that is a good thing, considering the high failure rate of M&A’s, is quite another thing:

Experts such as the Wharton School of the University of Pennsylvania’s Harbir Singh and Harvard University’s Clayton Christensen have recently reported a historically distressing level of M&A failure, citing failure rates as high as 90%. [CNBC]

And we have a feeling that the number of companies that de-list from the markets is higher than the number of new listings.

Another recent practice of dubious benefit is the emergence of software driven high-frequency trading (HFT). These automated, very short-term trades are a distinctly zero-sum activity (my win is your loss), and could in fact constitute a net bad to the economy (insofar as they attract the best and the brightest from more productive activities, scare other investors away from the markets, engage in dubious practices like quote stuffing, etc.).

We can preliminary conclude that apart from a relatively small number of new companies, the stock market has largely ceased to be an important source of capital for companies, supposedly it’s most important rationale. In fact, it seems to have become the reverse, money flows from companies to investors.

Listing, by focusing companies on the short-term, seems to act as a disincentive to investment, rather than an enabler and financier, and much of the stock market activity itself consists of a distinctly zero-sum, and perhaps even negative sum game called high frequency trading.

A sort of vicious cycle

While a stock market boom creates a wealth effect, but 80% of that goes to the top 10% of earners, so how much of that will be spent remains to be seen. At present, there is a shortage of demand because:

Households lost $9+ trillion in house value, whilst debt largely remainedUnemployment went up and labor force participation went down strongly suggesting unemployment is considerably higher than the official figuresMost wages are stagnant or even falling

The resulting demand shortfall produces considerable excess capacity (in plant, as well as excess labor). Now here’s the thing. Companies react to this by reducing investment in new production capacity, as the tepid demand makes top-line growth difficult to achieve.

In order to increase the bottom line and satisfy shareholders, companies concentrate their efforts on cost cutting. Since labor is in a difficult negotiating position, due to high unemployment, this meets little resistance. More people get laid off, wages decline. There is some counterweight, as US competitiveness improves, but international trade too small in relation to the US economy.

So basically what we’re saying is that while the US economy already suffers from insufficient demand, there is a mechanism via the stock market that creates a bit of a feedback loop in which, due to insufficient demand, companies cannot grow the top-line much, focus on the bottom line by cost cutting which, while great for profits, reinforces the demand problem as:

Companies don’t create much new production capacity (despite record low interest rates, record profits and record cash balances)Try to be as lean as possible by not hiring many new people and/or cutting wage cost.

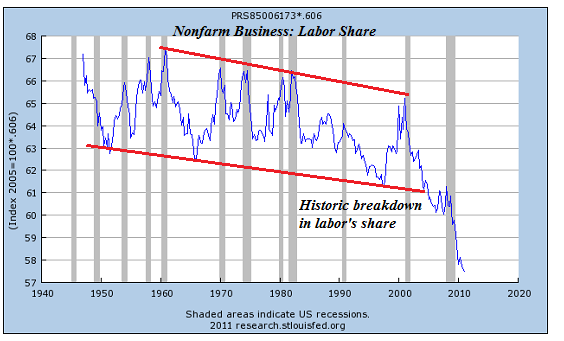

This basically redistributes income from labor to capital and this is quite visible in the data. Profit shares have risen to record highs, and the labor share fallen a lot, to such an extent that even The Economist is taking notice.

Conclusion

Apart from funding some start-ups, the stock market seems to have lost its main function as a source of funding for companies. Instead, it has become a channel for companies to fund investors, the reverse. Stock market listing also seems to be detrimental to investment levels due to the short-term outlook.

These developments have redistributional consequences, it reinforces a shift from labor to capital, just at a time such shift is already ongoing. This reinforces the main economic problem we suffer, insufficient demand, and it creates something of a feedback loop here.

While individual actors are rational (it’s imperative for companies to be lean, there is little reason to invest in new capacity when the demand for its products is not there, excess cash should paid back to shareholders, etc.), the end result clearly leaves a lot to be desired. In a follow up article, we’ll investigate what can be done to improve this situation.

Source:

Has The Stock Market Become Dysfunctional?

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More…)

Originally from –

Has The Stock Market Become Dysfunctional? [SPDR S&P 500 ETF …

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}