Here's KKR's Outlook For The Stock Market And … – Business Insider

REUTERS/Shannon Stapleton

Henry Kravis of Kohlberg Kravis Roberts & Co.

Kohlberg Kravis Roberts & Co. (KKR) is out with its

.

“We believe that we are now entering the global synchronous phase of a long but bumpy recovery process that started in 2009,” wrote Henry McVey, KKR’s Head of Global Macro & Asset Allocation.

“However, unlike many other synchronized global recoveries, developed market central banks are—in aggregate—likely to remain accommodative in an attempt to offset some of the inherent volatility that accompanies de-leveraging cycles. Against this macro backdrop, our asset allocation view for 2014 is that investors should “Stay the Course,” retaining key overweight positions in global equities and alternatives, including private credit, special situations and real assets.”

Here are McVey’s macro themes and tactical asset allocation opportunities:

Remain Overweight Developed Equities: Developed Market Equities May Enjoy Another Decent Year.

Many Emerging Markets (EM) May Lag Again in 2014, But Look For Some Differentiation Within Emerging Market Equities in 2014.

Fixed Income: Stay Overweight Illiquid Credit as It Remains Attractive at This Point in the Economic Cycle; Avoid Potential Duration “Hangover” in High Grade Credit and Government Bonds.

Fixed Income: We Are Further Reducing Emerging Market Debt (EMD) to Zero.

Fixed Income: To Gain More Flexibility, We Are Switching Bank Loans and High Yield Into Liquid Opportunistic Credit; Also, Add Lower Volatility Fixed Income Hedge Funds.

Real Assets: We Are Selling More Gold and Avoiding Tradi- tional Commodity Notes and Swaps With No Yield; Staying Overweight Income-Producing Real Assets.

Overweight Traditional Alternatives: Adding a Little More to Distressed/Special Situations.

Dollar Rally May Continue, But With Greater Differentiation.

Hedges: Volatility May Increase in 2014.

Here’s a summary of the firm’s 2014 targets:

U.S. Real GDP Growth: 2.8%

U.S. Inflation: 1.7%

Euro Area Real GDP Growth: 1.1%

Euro Area Inflation: 1.0%

China Real GDP Growth: 7.4% to 7.6%

China Inflation: 3.0% to 3.5%

S&P 500: 2,000

S&P 500 EPS: $120

S&P 500 LTM P/E: 16.7x

U.S. 10-Year Treasuries 2014E Year-End Target Yield: 3.1%

U.S. 10-Year Treasury Total Return: 1.0%

U.S. High Yield Total Return: 5.8%

A massive run-up in prices and an above-average price-earnings ratio have many concerned that the stock market may have gotten ahead of itself.

KKR

While the logic may be sound, the historical evidence shows that stocks can go higher and earnings multiples can expand further.

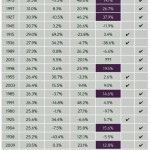

Indeed, 2013’s 29.6% surge represent the 12th strongest year for stocks since 1900. And on average, the stock market has returned an average 7.6% after a 20%+ year, which compares to an average 5.1% after all years. (See exhibit 44 to the right.)

“On the multiple front, we are using just north of 16.5x to reflect our view that real rates are likely to remain positive over the remainder of this economic cycle,” said McVey. “Indeed, …investors tend to place a significantly higher multiple on stocks when real rates turn positive as they have just done. Moreover, given that we expect slightly higher GdP growth on a go-forward basis in the 2014-2016 period, we gain comfort that some additional multiple expansion may be warranted. That said, we think the 17.9x projected multiple that typically accompanies a 2-3% 5-year trailing GdP environment may be too ambitious given the sizeable risk premium associated with exiting the historic amount of Fed-driven liquidity in the system.”

While McVey is bullish on U.S. stocks, he actually see greater opportunity abroad:

From a regional perspective, our view for 2014 is to have over- weight positions in Asia and in Europe, while we are equal-weighted the U.S. and Latin America in our target asset allocation. Key to our thinking is that, despite the strong increase in Japan during 2013, the stock market has actually gotten cheaper in absolute terms (i.e., EPS has increased more than prices; meanwhile, consensus annual EPS growth for 2014 is a solid 19%). We are also now more constructive on china (consensus EPS is for growth of 14%). In the euro area, we expect earnings to grow a full 21% year- over-year. by comparison, in the U.S. and Latin America, we expect earnings to grow 9% and 13-15%, respectively.

This is just scratching the surface of McVey’s report. Read the whole thing at KKR.com.

See original article:

Here's KKR's Outlook For The Stock Market And … – Business Insider

See which stocks are being affected by Social Media