How Do Net Current Asset Value Stocks Perform When Buffett's …

How Do Net Current Asset Value Stocks Perform When Buffett’s Favorite Valuation Indicator is Expensive

By:

| Tue, Jun 3, 2014

Warren Buffett, a former student and employee of value-investing pioneer Benjamin

Graham, commented recently on how expensive the overall stock market is currently.

One of the metrics Buffett uses to describe the valuation of stocks is to compare

the market value of stocks to the size of the U.S. economy. The metric used

to measure the size of the economy is the Gross Domestic Product (GDP). Sometimes

Mr. Market bids up stock prices to lofty levels relative to GDP, and at other

times stocks become depressed relative to the size of the overall economy.

This valuation ratio is not a short-term market-timing tool, but it does provide

guidance as to whether returns will be above or below the average over the

longer term.

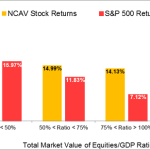

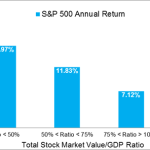

The chart below illustrates the performance of the S&P 500 at different

valuation levels. As the overall stock market becomes more expensive relative

to the size of the U.S. economy (GDP), average annual returns over the next

5 years trend lower. The current reading on the stock-market-value-to-GDP ratio

is currently more than 100%. Historically, this has not been the greatest entry

point for someone putting new money to work in a broadly diversified stock

fund, even one that charges low fees.

Unlike the S&P 500 Index, the disappointing stock performance at lofty

valuation levels does not seem to be the case if one follows Benjamin Graham’s

rule for enterprising investors by only purchasing stocks trading below net

current asset value.

Net current asset value (NCAV) is a simple calculation used to describe the

minimum liquidation value of a firm. The calculation is made by subtracting

all liabilities — including preferred stock — from the most liquid assets

on a company’s balance sheet and converting the figure to a per-share basis.

If a company is found trading below net current asset value, the performance

of these out-of-favor stocks is excellent. The chart below assumes an investor

puts no more than 10% in any one stock trading below 75% of net current asset

value and holds the stock for a 5-year period. Using Buffett’s favorite indicator

for overall stock valuation, even when stocks are lofty in price relative to

GDP, the performance of net current asset value stocks holds up.

Why is it that stocks trading below net current asset value outperform even

during time periods when the overall market is expensive? One reason is the

superior selection criterion of investing in stocks trading below liquidation

value. The other reason is having the discipline to let some funds sit idle

during time periods when the stock market is expensive. There are fewer stocks

trading below net current asset value when the market is at an extreme high

relative to GDP. By restricting purchases to no more than 10% in any one stock,

our net current asset value portfolio sat partially in Treasury Bills more

than half the time when the stock- market-to-GDP ratio was more than 100%.

Many investors feel a psychological comfort in joining the collective conscious

and purchasing stocks when everyone else seems to be buying. Those time periods

seem to coincide with lofty stock valuations. During time periods when stocks

are expensive, investors embracing a value investment philosophy are tempted

to relax their buying criterion and load up on stocks. Having a portion of

your funds sitting on the sidelines, waiting for more stocks to trade below

liquidation value is hard to do when stocks continue to bubble higher. The

illustration above shows that investors who can discipline themselves to remain

partially in low-interest-bearing Treasury Bills when stocks are expensive

can still do well over the long term in terms of portfolio performance.

Enterprising investors should avoid the temptation to purchase stocks trading

at a higher valuation than net current asset value, regardless of where the

overall market is trading relative to GDP. When stocks are expensive relative

to GDP, spending time pursuing other activities might be more productive than

abandoning the strict value-investing criterion and wandering into the area

of pure stock speculation.

Please enable JavaScript to view the comments powered by Disqus.

Author: Victor Wendl

Victor J. Wendl

President

wendlfinancial.com

Important Disclosure: Victor Wendl is the author of The Net Current

Asset Value Approach to Stock Investing. The book reviews the performance

over a 60 year time period of purchasing stocks trading below net current

asset value. The stock filtering criterion was popularized by Benjamin Graham,

the father of value investing, and a mentor to Warren Buffett who considered

his professor and former employer one of the most influential people in his

life. The Net Current Asset Value Approach to Stock Investing is available

for purchase on Amazon.com,

as well as for Nook and Kindle reading

devices.

Wendl Financial, Inc. is registered as an investment adviser with the state

of Missouri and only conducts business in states where it is properly registered,

or is excluded or exempted from registration requirements. Registration as

an investment adviser does not constitute an endorsement of the firm by securities

regulators. The information in this article is for general information purposes

only and should not be construed as personalized investment advice.

You must be aware of the risks and be willing to accept them in order to invest

in the stock market. Don’t trade with money you can’t afford to lose. This

is neither a solicitation nor an offer to buy stocks. No representation is

being made that any account will or is likely to achieve profits or losses

similar to those discussed on this Web site. The past performance of any trading

system or methodology is not necessarily indicative of future results. No representation

is being made that any account will or is likely to achieve profits or losses

similar to those shown.

Past performance results is not an indication of future performance. Wendl

Financial shall have no liability of whatever nature in respect of any claims,

damages, loss, or expense arising out of or in connection with the reliance

by you on the contents of our website.

Copyright © 2014 Victor Wendl

All Images, XHTML Renderings, and Source Code Copyright © Safehaven.com

Link:

How Do Net Current Asset Value Stocks Perform When Buffett's …

See which stocks are being affected by Social Media