How to Pick Companies to Pitch in Hedge Fund and Private Equity Case Studies in 5 Simple Steps

Some decisions in life deserve serious, thoughtful contemplation.

Other times, you have to make a split-second decision and live with the consequences.

Picking companies to pitch in hedge fund and private equity case studies falls somewhere in the middle.

If you already have a few companies in mind, you need to decide on one quickly – but if you have no clue where to start, then you need more time to consider your options…

…but not too much time, or you’ll never finish the case study.

But it’s also tricky because a company that’s good to invest in (in real life) is NOT necessarily good to use in a case study or stock pitch.

To illustrate how this process works, I’m going to walk you through how we decided on one of the companies in our main valuation case study – Jazz Pharmaceuticals – and why we rejected dozens of other candidates in the process.

By the end, you’ll have a 5-step process you can use to select companies for your case studies in any industry:

The Punch Line

I have to start with the punch line: you are somewhat screwed if you get a case study or stock pitch and you don’t already have a company in mind (or they don’t assign one to you).

It takes a fair amount of time to screen companies and pick a good one – and the more time you spend on screening, the less time you have for your model, write-up, and presentation.

The time required to find companies is more of an issue with hedge fund and asset management case studies, since the “instructions” often consist of: “Pick something – anything – and pitch it to us.”

In 90% of private equity case studies I’ve seen, they give you a company, an offering memorandum, or a set of documents they want to analyze.

Regardless of what you interview for, though, you should have a few companies “in your back pocket” from your industry or your deals.

Case studies and stock pitches, of course, are the critical component in buy-side interviews because they’re the closest representation of what you do on the job.

But picking the right company to pitch is the first, and most important, step in the case study.

Get that wrong, and nothing else – not even your fancy multi-stage DCF with 500 sensitivities – matters.

Real Life vs. Case Studies

In the previous series on hedge fund stock pitches, our interviewee laid out some of the criteria required for a good pitch:

Mispriced Asset – The stock, bond, or other asset has to be mispriced in some way, which you demonstrate with a valuation.

Reasons Why No One Else Has Noticed It – Why have you found this mispriced asset that no one else has discovered yet?

Catalysts – And then there must be specific events in the next 6-12 months that will push the company’s share price closer to its intrinsic value.

Risk Factors and Mitigants – Finally, you acknowledge why you might be wrong and explain how to reduce the risk with call/put options or other investments.

If you have the time or you’re putting real money into it, then yes, follow these criteria.

But if not, and you’re under time pressure, you should think about a different set of criteria for case study purposes.

The main difference is that your recommendation does NOT need to be correct.

It just needs to be finished, and you need to be able to present it effectively.

No hedge fund manager is going to wait 12 months to see if your stock pitch was correct; they make decisions quickly, largely based on your analytical and communication skills.

So I recommend this alternate set of criteria:

Industry You Know Something About – You might think it’s a good time to learn about airlines or oil & gas companies or commercial banks, but trust me: all of those are really bad industries to pick if you don’t know much about them. Pick an industry you know well, or one with few or no industry-specific metrics and valuation methodologies (consumer/retail, technology, media, etc.).

Small to Mid-Size Company and Relatively Pure-Play Business – In other words, don’t pick a conglomerate like GE or Vivendi or Samsung that does everything imaginable. Go for companies with revenue in the hundreds of millions to low billions USD that have only a few business lines – they will be much easier to analyze and present.

No More Than 3-4 Key Drivers – Do not pick a company with 20 different business lines where each segment depends on entirely different assumptions. An industry like consumer/retail is great for limiting the number of drivers because revenue depends on the number of stores and the average sales per store. Something like the maritime / transportation industry is not ideal because you need to make granular assumptions for different types of ships in the fleet.

Straightforward Financial Statements – The LAST thing you want is a company with “messy” financial statements. Think: a Cash Flow Statement that’s four pages long, or an Income Statement with 13 non-recurring charge categories, or a Balance Sheet with dozens of small items with impossible-to-distinguish names. Messy financial statements will drive you crazy and suck up your time, which is why we cleverly avoid them (for the most part…) in our courses.

The Possibility of Solid Catalysts – This one is less important than the three criteria above because your catalysts do not actually need to transpire. But companies in some industries do tend to have solid catalysts – pharmaceuticals is a good example since new products are always launching – while others, like retailers, tend to have fewer potential catalysts.

If you have a complicated, brilliant stock pitch for a reverse merger, divestiture, or multi-company acquisition, good for you!

Go ahead and use it if you feel you can explain it well.

But if you’re short on time or you don’t have existing work to draw on, keep it simple.

The Actual Process We Used to Pick Jazz Pharmaceuticals

With most of the original BIWS courses, I did 99% of the work myself.

With this new Fundamentals course, though, that wasn’t possible because I wanted to use a different company in a different industry in a different geography for each topic area.

This approach made for a better course, but it also increased the amount of work by 10x.

It also resulted in a few bald spots on my head, but we’ll save that story for another time…

I knew from the start that I wanted to cover biotech or pharmaceuticals because:

We had received a ton of questions on it.

There was no coverage in the existing lessons, except for one bonus case study.

And it was a perfect industry for valuation / stock pitch / equity research case studies.

So I had another team member, who helps me with research and Excel work, sift through 50+ pharmaceutical companies, make notes about their financial statements, and rank each one:

He made notes on everything from the “messiness” of each company’s financial statements to other potential problems, like a share price under $2.00:

Then, I did additional research on each company with a “1” ranking.

I spent five days looking through public filings, investor presentations, and Fairness Opinions to narrow this list down to 3-4 candidates.

You will not have enough time to use this same process.

Often, you’ll only get a few days to a week to pick your company, build the model, write your recommendation, and then present it.

However, you can apply many of the same principles – in abbreviated form – to pick your company.

Here’s the 5-step process I recommend:

Step 1: Pick an Industry

An industry you’re familiar with is definitely the best bet.

If the fund you’re interviewing at happens to specialize in, say, technology stocks, and you know nothing about technology, then pick something you know better and use that.

If you know about a tangentially related industry, like media or telecom, then a company there is better than one in an entirely different industry (e.g., energy).

In this example, I’ll assume that you know something about healthcare and biotech / pharmaceuticals, so you’ve picked that for your sector.

Step 2: Find an Initial Set of Companies

Next, you need a starting point: an initial list of firms.

To do this without Capital IQ or Factset, use Google Finance or Finviz.com.

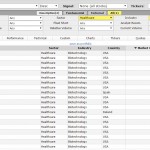

For example, here’s the initial set in the “Pharmaceuticals” category, which I’ve sorted by revenue:

To find this, type in the name of a company (e.g., “Johnson & Johnson”) in the industry and click on Sector: Healthcare > Industry: Pharmaceuticals – NEC at the bottom:

You could then click on the “Healthcare” top-level grouping, then go to “Pharmaceuticals & Medical Research,” and then go to the separate “Pharmaceuticals” and “Biotechnology & Medical Research” groupings.

You could keep clicking around within each category, but it’s more helpful to screen by revenue at this stage.

After all, it doesn’t make sense to pick a $50 billion revenue company, nor does it make sense to pick a $30 million revenue company… so you can eliminate A LOT of possibilities like that.

I looked at the companies and decided that a $500 million – $2 billion revenue screen made sense.

Within just the “Pharmaceuticals” category, that give me about 10 companies: a good number, but not an overwhelming one.

Included in this set were companies like Salix Pharmaceuticals (SLXP) (acquired by Valeant), Cubist (CBST) (acquired by Merck), BioMarin (BMRN), and The Medicines Company (MDCO).

Interestingly, Google Finance did not list JAZZ as a “Pharmaceutical” company.

On the other hand, if you use finviz.com for this screen, you get an arguably more accurate set of businesses that also includes JAZZ:

While finviz.com sometimes has more useful groupings than Google Finance, it also has some odd quirks (such as no ability to sort by sales, unless I am missing something)… so your mileage may vary.

Step 3: Weed Out Companies with Messy Financial Statements

Regardless of where you find your list, though, you should start by eliminating companies with messy financial statements and confusing line items.

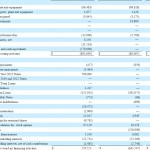

Here’s an example of one company I eliminated in this step – Endo Health Solutions.

While its Income Statement and Balance Sheet are relatively straightforward, its Cash Flow Statement is not – as you can see below:

Truthfully, this CFS is not even that bad since you could consolidate many of the debt-related line items… but the company wasn’t ideal, either.

This same thought process eliminated quite a few companies.

Nothing had terrible financial statements in the same way many REITs do (hello, 3-page Cash Flow Statements!), but some were more suitable than others.

Step 4: Look for Straightforward, Yet Potentially Interesting Companies

Once you’ve eliminated companies with less-than-ideal statements, turn your attention to the business segments (2-3 is much better than 10) and potential catalysts.

For catalysts, acquisitions work well, as do imminent product launches or even longer-term product launches that might be affected by short-term news (e.g., clinical trial results).

Product launches work especially well for bio/pharma companies because you could always argue that prices will rise more quickly or more slowly than expected, or that the total addressable market differs from market expectations.

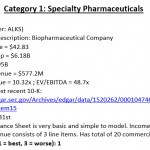

Here’s one company I eliminated in this step (Alkermes) on the basis of business segments:

This business isn’t terribly complex, but I felt that 7-8 product lines were too many, especially since many of them were about the same size.

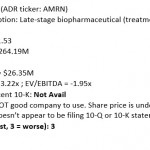

On the opposite end of the spectrum was a company like Questcor, which had simple financial statements, but a different problem (quote from the 10-K below):

“Over 95% of our net sales in each of these years were from Acthar.”

I wanted something “in the middle” – not a one-trick pony, but also not a company with 7-8 product lines.

I also cut any companies that were in the process of being acquired (due to limited upside and downside).

Finally, I did a quick search on Google News for press releases just to verify that there would be something to use as a catalyst for each company.

I went through this process with the other companies we found, eventually narrowing the list to just 4 candidates: Jazz Pharmaceuticals (JAZZ), ViroPharma (VPHM), Alexion (ALXN), and Auxilium (AUXL).

Step 5: Decide!

Once you have 3-4 good candidates, it comes down to personal preference.

I picked JAZZ for one simple reason: its products were the easiest to explain.

Specifically, everyone understands what its key drug Xyrem treats: “excessive daytime sleepiness.”

The other companies had more esoteric drugs for rare disorders like “Dupuytren’s contracture.” Yes, go ahead and Google that one now – I know you want to.

Especially when you present to people without a biotech/pharma background, companies with easier-to-explain products and services tend to work better.

The Case, the Thesis, and the Pitch

If you’ve been through the new course, you already know the outcome of this research. We picked JAZZ and made a simple argument for the investment thesis:

- Pricing on Xyrem can go much, much higher – from $50,000 – $60,000 per year to $120,000 per year, based on price escalation for other orphan drugs (oh, and the completely broken health insurance industry).

- The drug will also get a higher-than-expected number of patients due to the success of the company’s marketing campaigns.

- And generics competition will enter the market later than expected.

Based on all that, plus a 10-year DCF and other analysis, we said the company was worth $180 – $200 vs. a share price of ~$130 at the time.

And as I write this, the stock is up to $181.71.

But the important part is that this was a very simple argument, and we based it on a straightforward company with clean financial statements.

If you had only a few days, you could not have come up with the 20-page stock pitch and the same detailed analysis we used in the course.

But you could have easily picked the same company and used simpler analysis to reach a similar conclusion.

Case Studies: Natural Selection?

One of my favorite quotes on this topic comes from Napoleon:

“The amateurs discuss tactics. The professionals discuss logistics.”

You might be mistakenly focusing on the tactics when completing case studies.

Have you run every sensitivity imaginable? What about a 10-year DCF with all the bells and whistles? Did you estimate the exact per-share impact if risk factor #12 comes to pass?

Or, even worse, you might be jumping into Excel right away without reading enough to come up with an intelligent view of the company first.

But none of that means anything if your logistics are dysfunctional – in other words, if you’ve picked a firm that’s not suitable for a stock pitch.

Pick the right company, though, and you’ll come out ahead of your competition, even if your tactics aren’t quite as fancy.

It’s just the professional thing to do.

View original article:

How to Pick Companies to Pitch in Hedge Fund and Private Equity Case Studies in 5 Simple Steps

See which stocks are being affected by Social Media