Huttig Building Products: A Housing Stock Trading … – Seeking Alpha

Huttig Building Products (HBP) is a large distributor of doors, decking, and millwork. They sit as a middleman between manufacturers and companies like ProBuild who cannot carry such a large array of inventory. Prior to the downturn, this is a company that saw nearly 130 years of consecutive profitability. Huttig was spun out of Crane in 1999/2000 time frame. Michael Burry did a nice write-up which can be found here which gives some historical background and is a good jumping off point.

Of course, the housing market fell apart several years after Burry’s write-up and the company went well off the radar for most investors after they delisted and fell below $1 a share. However, solid management with a decent chunk of equity (CEO Jon Vrabely owns around 5% of the company) began cutting costs in the back half of 06′ – way before many other operators. They were nearly completely finished by 2009. This allowed the company to pull through and stay alive. HBP trimmed their footprint from 47 facilities all the way down to 27. They took people from 2,200 down to 1,000. The company maintained a large footprint in the coastal areas so they can continue to serve 80% – 85% of their markets. In most cases, they did not completely exit markets even though they shuttered facilities. For example, the company can still touch Atlanta out of South Carolina. Also, most of the closed locations did not represent a significant piece of the business to begin with.

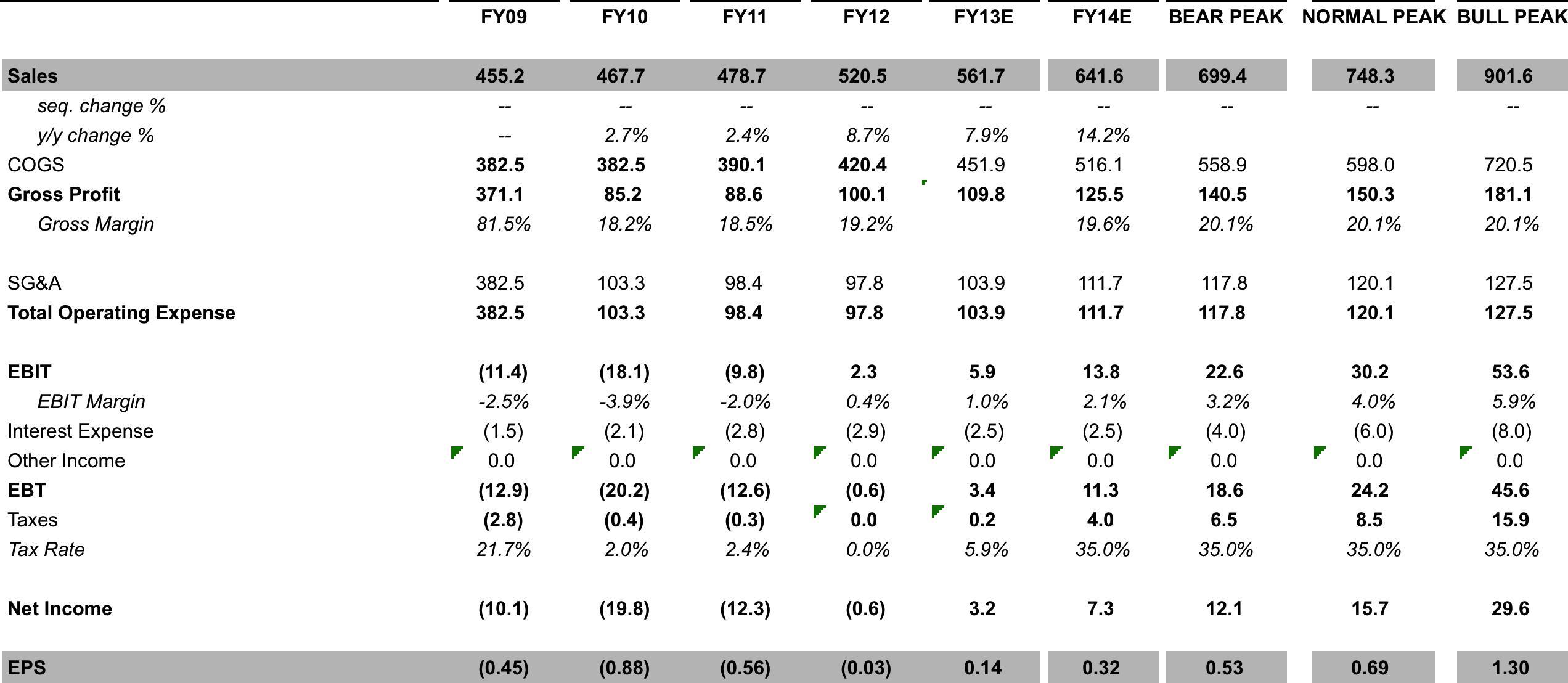

Fully taxed, earnings should reach nearly .70 at sales 30% below prior peak levels (assumes 1.4M starts vs. peak 2M). Phil Keipp, the CFO was brought out of retirement in 2006. Prior to HBP, Phil was with HD Supply where he was CFO of their largest division – the water works business. This was a $3.5B business with 240 locations and HD Supply’s largest business group. Phil is bringing a level of financial discipline to the company which they didn’t really have before. Prior to HD Supply, Phil was with KPMG for 11 years. In the prior peak, EBIT margins hit 3% but this time around the company should be able to achieve much greater profitability. The company got out of some lower margin businesses as well. For example, they had a business in Kansas City where they sold product directly to builders. This was abandoned (doesn’t make their other customers very happy either to be cut out of the process). Key competitors include BlueLinx Holdings (BXC) and Boise Cascade Company (BCC), but both have a lot of lumber business and are susceptible to changes in the price of wood so margin compares are difficult. There are also some local and regional competitors but they are private so we can’t draw much from them either.

The revenue is split 45% Millwork and 45% wood products. Around 10% of sales are tied to storm driven roofing. Sales will be driven by a mixture of new construction (primary) of single family homes and also remodeling. Millwork tends to lag in a recovery as it is not the “go to” fix-up like a new kitchen or a new bathroom which are perceived to add value to a house. Both Home Depot (HD) and Lowe’s (LOW) on their recent conference calls have reported that Millwork sales are below the company average; however, in time this too will recover.

Uplisting: As noted above, the company recently listed themselves on the Nasdaq after having traded on the OTC for some time. Prior to delisting, the company was listed on the NYSE. The up-listing should enhance visibility and act as a catalyst. Management is talking about doing more on the IR front but still feels it’s a bit too early. However, six months ago they thought up-listing would come in two years and that happened way earlier than expected.

Buyback: About a year ago, C-MEX a large shareholder with 2 board seats sold out of their holding. They held 5.8M shares. HBP bought back 1 million shares and a consortium of other buyers came in a scooped up the remaining 4.8M. C-MEX relinquished their board seats.

Prior peak sales were near $1.1B. This model assumes a bullish peak of $900M and near 6% EBIT margins. To get there, the company will have to execute flawlessly and we will need a really nice recovery in housing starts. However, even at the bear case assumptions of an unremarkable 25% increase in sales, the stock is cheap. It is cheap even under the most conservative earnings assumptions.

.53 .69 1.30

8X $4.24 $5.52 $10.40

10X $5.30 $6.90 $13.0

12X $6.36 $8.28 $15.60

15X $7.95 $10.35 $19.5

At the height of the housing bubble, HBP sold for an enterprise value of $275M. Today, it’s a leaner/better company. It does not take any heroic assumptions to arrive at an enterprise value that is higher than the current one.

Risks:

– A large ramp in sales does not translate into significant bottom line leverage due to poor execution.

– Housing recovery gets derailed. We think the risk of this is low given continued interest on the part of the fed to keep mortgage rates low. Population growth of 1% – 2% a year pretty much assures the recovery will happen, it’s just a matter of timing.

– Consumer starts saving and stops spending. We think this is the greatest near term risk to the story.

– CFO leaves. We don’t think he has any intention to retire but he retired once before so its always a possibility.

– Competition. HBP competes mostly on price and relationships. There isn’t much here in terms of differentiated products/moat. Having said that, the company has been around for over 128 years and we believe it is in a better position now in terms of ability to gain meaningful operating leverage than at any other point in time.

– Liquidity. This is a small cap name with limited volume so it can be hard to get in and out. In a bad market sell off the name could get hurt more than others.

Catalysts:

– Recent uplisting to Nasdaq

– Improving housing starts

– Increased spending on remodeling

– Recovery in manufactured housing (10% of sales)

Source:

Huttig Building Products: A Housing Stock Trading At 4 Times Peak Earnings

Disclosure: I am long HBP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More…)

Link:

Huttig Building Products: A Housing Stock Trading … – Seeking Alpha

{kind=link}