Serial Correlation: What it is and How it Applies to Stock Trading

Serial correlation, sometimes also called autocorrelation, defines how any value or variable relates to itself over a time interval. It is a technical term used by statisticians, mathematicians and engineers. Don’t worry if it doesn’t click right away; by the time we’re through with this tutorial, you’ll not only understand what serial correlation is, but also how it is used by stock brokers to predict future prices of a stock.

You can learn more about serial correlation and other quant based stock trading theories in this course on mastering charting reading and technical analysis.

Serial Correlation for Laymen

First, let’s try to arrive at a definition of serial correlation in plainspeak: serial correlation is the relationship of a quantity with itself over time.

For example, we know that stock prices are time dependent, i.e. they vary with time. Now suppose we were tasked with estimating the dividend from a stock within a specific time frame, say, a quarter. If we were to somehow overestimate the dividend from the stock (called ‘error term’ in econometrics) in one quarter, serial correlation would dictate that the overestimation would carry over to subsequent quarters.

In the simplest possible terms, serial correlation defines how past values affect present values.

Serial correlation was originally a concept used in signal processing and systems engineering to determine how a signal varies with itself over time. It was later adopted by fields like econometrics to make sense data that varies with time. In the 1980s, as economists and mathematicians invaded Wall Street, they brought over the idea of serial correlation to predict stock prices.

Today, serial correlation is extensively used by trading analysts to see how past prices of a stock vary over a time interval. Since trading analysts (often called ‘quants’ in the business) essentially predict future prices based on data, not company fundamentals, serial correlation gives them an indicator of future price movements based on past prices. Therefore, understanding this correlation is important for anyone who wants to trade on the ‘quant’ model.

New to trading? Understand how option spreads and credit spreads work in this course!

Understanding the Theory Behind Serial Correlation

Now that we know what serial correlation is, let’s try to arrive at a more theoretically sound definition for it.

Let us suppose that we have two error terms, εi and εj , where εi is the magnitude of error at some time interval i and εj is the magnitude of the error at some time interval j, such that i ≠ j. When εi does not have a relation with εj, i.e. the magnitude of one error does not influence the magnitude of another error, the two error terms are said to be independent or unrelated.

However, more often than not, there is some distinct relationship between two error terms separated by a time interval. The most common of these relationships is serial correlation where one error term, εi has a positive/negative correlation with another error term, εj. When this happens, the assumptions in the original model are violated and thus, we have to account for the relationship between error terms. Practically, if there is something causing an error term in one time period, i, it only follows that it would cause an error in another time period, j.

Mathematically speaking, a serial correlation in a linear regression model can be denoted as:

corr(εj – εi) ≠ 0

That is, the correlation between the two terms is not equal to zero.

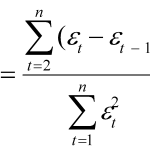

A popular test for verifying serial correlation is the Durbin-Watson test which can be calculated as:

Going deeper into regression models and the Durbin-Watson tests is beyond the scope of this tutorial. What we will look at, however, is the different types of serial correlation and how it applies to stock trading.

Types of Serial Correlation

Serial correlation can be either positive or negative. A brief definition of both is given below:

1. Positive Serial Correlation: Sometimes also called positive first-order serial correlation, this is the most common type of correlation where an error term has a positive bias on subsequent error terms. The correlation is mostly serial, that is, an error term in one time period has a positive bias on error terms in a subsequent time periods (say, like two successive quarters). It can also be non-linear – for example, an error term in the third quarter manifesting a positive bias in the third quarter of the subsequent year.

Mathematically, this can be represented as:

corr(εj – εi) > 0

2. Negative Serial Correlation: Also called negative first-order serial correlation, here, a positive error is followed by a negative error, or a negative error followed by a positive one. That is, the error term has a negative influence on subsequent error terms. This type of serial correlation is far less common. Mathematically, it can be represented as:

corr(εj – εi) < 0

Trading options? This course on essential strategies for mastering the stock market will help you make the most of your investment.

Serial Correlation and Stock Trading

Serial correlation defines how a specific quantity relates to itself over time. As mentioned before, it is a statistical term with applications in multiple fields, including mathematics, signal processing, trading analysis, and of course, statistics. The most useful application of serial correlation, thus, is in determining not just how a quantity relates to itself, but also to predict future correlations.

For example, in stock trading there is a widely held belief that today’s price changes in a stock relates valuable information about tomorrow’s price changes (εj affects εi). As per this assumption, an increase in prices today may cause prices tomorrow to:

Go up, as momentum from the positive change carries onwards.

Go down, as investors cash out their profits.

Remain the same, i.e. there is no correlation between prices on subsequent days and each day begins anew.

Scenario #1 is clearly a case of positive correlation. If the correlation is statistically significant, a trader can predict the positive future movement of the stock price.

Scenario #2 is an example of negative correlation. Again, if correlation is apparent statistically, a trader may move money out of the stock in anticipation for the predicted drop.

Scenario #3 assumes that there is either no correlation between day-to-day prices, or that the correlation is not statistically significant enough to be considered valuable.

Keep in mind that correlation is highly dependent on time periods. While one may observe a correlation in day to day or even hour to hour prices, the correlation may be absent or statistically insignificant if the time period is larger, i.e. year to year or even quarter to quarter.

As a trader, you can use serial correlation to make decisions about buying or selling a stocks, provided the data is statistically significant enough. You can learn more about trading in this course technical analysis of stock charts.

What are your favorite stock trading tips and tricks? Share them with us in the comments below!

More –

Serial Correlation: What it is and How it Applies to Stock Trading