The Stock Market In 2014 [SPDR S&P 500 ETF Trust, ProShares …

I’ve been working on gathering my thoughts for the market in 2014. This is a very useful exercise, in that it forces us to really think about what goes into stock prices, what those assumptions should be, and how they interact.

There are three key variables here: the growth rate of the economy as a whole and the level and change in profit margins (which together will determine corporate earnings growth), and the level of price multiples (or how much investors will pay for a given level of earnings). The fourth variable, what happens in Washington, DC, factors in as well, of course, but that’s a subject for another day.

Economic Growth Rate

The growth rate for the third quarter was just revised upward to 3.6 percent, largely due to increased inventory investment by businesses, which probably won’t be repeated. Nonetheless, we do see growth accelerating, and we also see the components of growth in almost all of the major areas – consumer, business, net exports and government – improving as well.

This discussion deserves a post of its own (probably more than one), but I will say that I expect U.S. growth to be in the 3.5 percent-4 percent range for 2014. Most of this will come from consumer spending growth, but government is also poised to stop subtracting from growth – and maybe even contribute – and business is showing signs of stepping up.

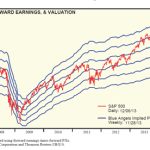

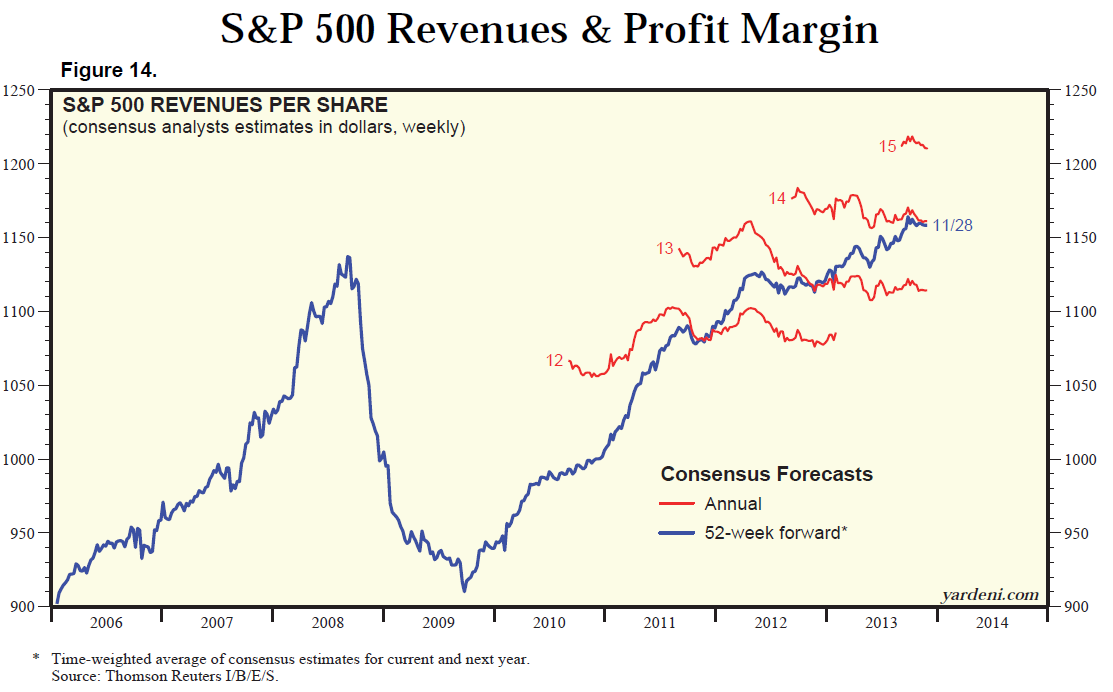

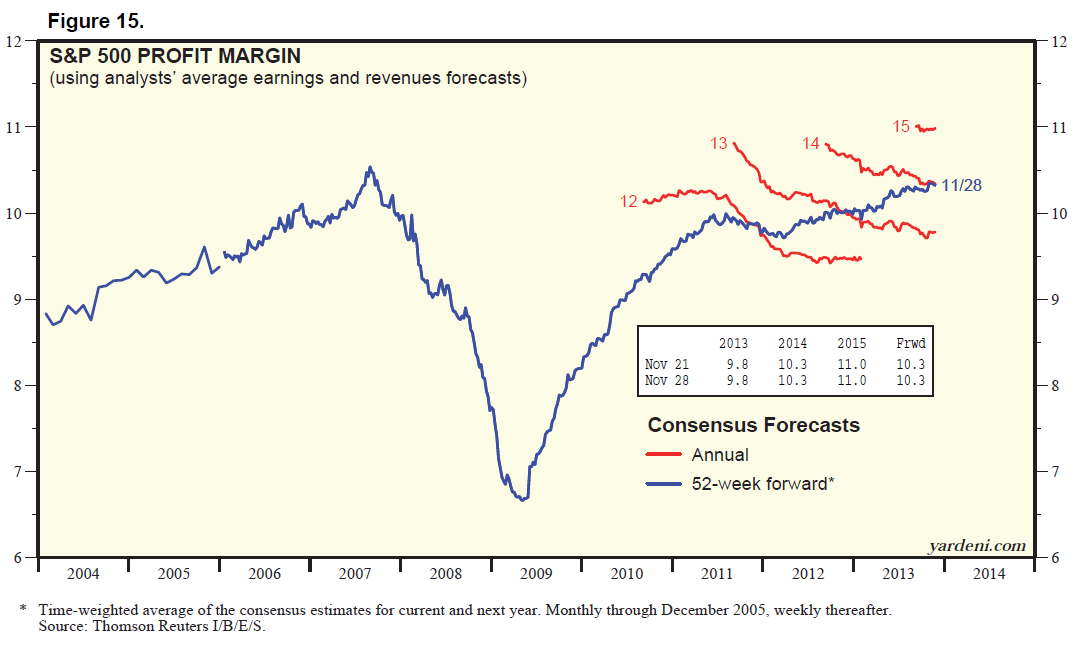

Aggregate corporate revenue, the top line, grows over time at the rate of GDP growth, so we can reasonably estimate revenue growth at, say, 4 percent. This may actually be generous. Looking at a report by Ed Yardeni, available here, we can see that current revenues are right around the level analysts project for 2014. Using 4 percent seems reasonably fair but isn’t a slam dunk.

Profit Margins

If nothing else changes, with revenue growth of 4 percent, we would also see corporate earnings grow at 4 percent, depending on how well the businesses are run – that is, on the profit margins. Profit margins are currently very close to all-time highs, which may limit any future improvements. Just as with revenues, we’re also currently at the estimated profit margin for 2014, per Yardeni.

There are reasons to believe that margins might come down, with rising wages being the most prominent, but increasing operating leverage as the economy improves may well compensate for that. Overall, margins can reasonably be expected to stay around current levels for 2014, so overall corporate earnings should grow by about the 4 percent of the economy as a whole. The remaining question is, how much will investors be willing to pay for those earnings?

Price Multiples

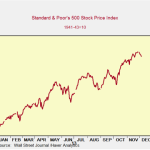

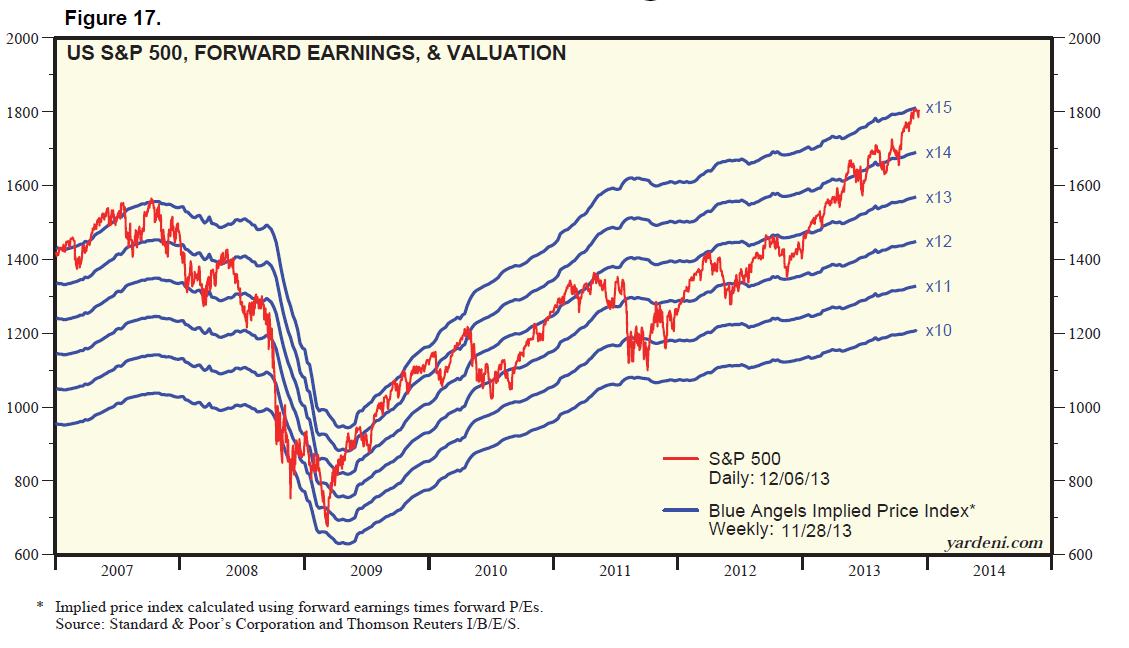

Looking at the past five years, multiples have bounced between 10 and 15 times forward earnings for the S&P 500. Back at the peak in 2007, they even briefly exceeded 15x. With current prices for the S&P 500 now brushing 15x again, it seems unlikely that multiples will expand even further in 2014. In fact, it seems quite possible that valuations could tick down again.

Conclusions

Right now, if the economy continues its accelerating recovery and businesses continue to operate at their current very high profitability levels, the stock market can be expected to appreciate around 4 percent in 2014 – implying a year-end target of 1,880 for the S&P 500.

This is close to a best-case scenario, and is based on earnings growing as expected and profit margins staying high. The reason it may not be a best-case scenario, though, is that with investors shifting from a fundamental to a psychological basis, as I have noted before, we may see multiples pushed higher than 2007 levels. We’re already seeing several other metrics – margin debt, for example – pushing above 2007 levels, so there is no reason multiples couldn’t do the same. There are upside risks here.

The downside risks, though, are more serious in my opinion. The projection above is reasonably likely based on my conclusion that the economy is in a sustainable recovery. It also seems likely that margins should remain around current levels.

The valuation, again, is the key variable. Valuations are typically based on the expected level of future growth, with investors willing to pay more for faster growth. As you can see from the above charts, expected future earnings growth (for 2015) looks quite high and, even with strong economic growth, could be tough to meet. If investors moderate their growth expectations, multiples could get hit.

Looking at the chart above, you can see that around 14x forward earnings is a typical multiple for most of the past five years. Based on an earnings growth rate of around 4 percent, and using a concluded typical 14x multiple, the indicated year-end target for the S&P 500 would be around 1,750.

Overall, I suspect the risks to the overall economic growth rate – and, therefore, for aggregate corporate earnings – are on the upside, while margins and valuations are likely to decline slightly. The indicated target, then, is between the two indicators above, 1,750 and 1,880.

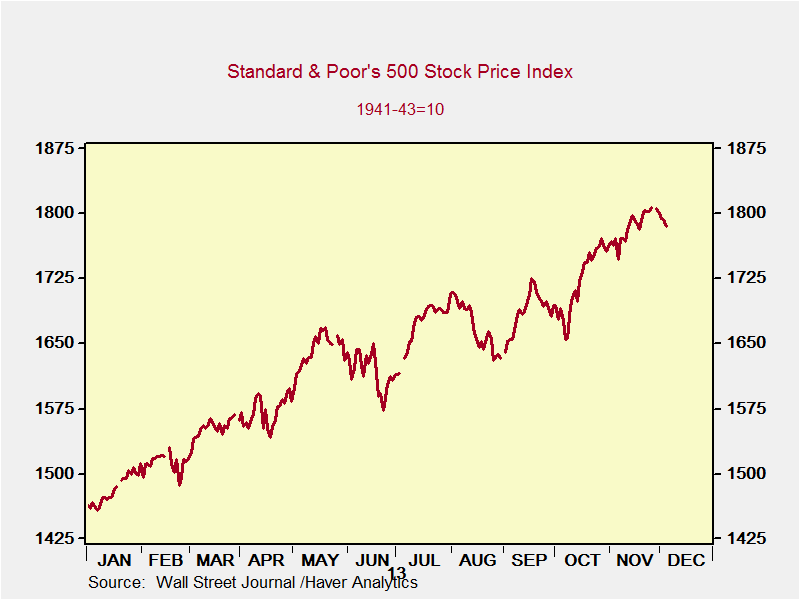

Looking at the market so far this year, we ran quickly up to 1,800 and have since taken a break. Although we’ve edged above that level in the past several days, the momentum seems to have slowed.

With the Fed poised to taper its stimulus in the next couple of months, with rates rising slowly, and with most metrics already about as favorable as they get, I find the notion of continued double-digit appreciation hard to support. In fact, as mentioned above, I believe the market will normalize in 2014. I am therefore projecting a year-end 2014 target of 1,800 for the S&P 500.

This is not a prediction of a flat, boring market. I believe a sell-off in the first quarter is very possible, as investors reexamine their holdings after the end of the year, and as they process the first step of the Fed’s taper process. I also expect investors to reassess the attractiveness of stocks as interest rates rise, which they should during 2014. Finally, I also expect wage growth to accelerate, which should have a negative effect on profit margins, even as it boosts the economy as a whole.

Current expectations for the market appear entirely too rosy. Too many metrics are too high – in many cases, at or above 2007 levels. This certainly doesn’t signal problems in the short term, but it probably does mean future appreciation opportunities are limited.

As always, the value of this exercise is in the process, not the conclusions. I think the key factors I mentioned have to define the possible outcome, but their interactions depend more than anything else on the psychology of investors – which, in many ways, depends on the actions of the Federal Reserve.

For 2014, as for the past several years, the financial center to watch will be Washington, DC, not New York. With that in mind, any forecasts will have to be revised significantly when they change the rules of the game again.

Source:

See original:

The Stock Market In 2014 [SPDR S&P 500 ETF Trust, ProShares …

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}