What Stock Market? These Dividend Contenders Are Not …

Introduction

It has become vividly clear to me that many investors continue to believe that the stock market in general is currently overvalued. Some even go as far to say that it is currently in bubble territory. Although I disagree, (my views about the valuation level of the stock market as measured by the S&P 500 can be found in the introduction to my most recent article found here), it is not this fact alone that disturbs me most.

My main concern deals with how this view of the current state of the market causes many investors to be frozen or afraid to commit their capital to common stocks. Convinced that a market correction is imminent, they are sitting on cash in hopes that better investment opportunities are soon to come. Therefore, cash sits idle earning little to nothing, while time marches on. For most of us, both cash and time are scarce commodities. But to my way of thinking, time is the most precious of all. We might find ways to get more cash, but once the clock ticks, time is gone forever.

Warren Buffett has reminded us about the folly of this behavior on more than one occasion. During the throes of the Great Recession he published an op-ed in the New York Times on October 16, 2008. The following excerpt speaks to my point: “Today people who hold cash equivalents feel comfortable. They shouldn’t. They have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.” Then again, on February 9, 2012, in a piece he published on CNNMoney, he added more color.

I acknowledge that both of the above Warren Buffett writings were made during a time when the market was especially undervalued. Nevertheless, the underlying principles that Warren was writing about in both cases, dealt with how and why time is the friend of the serious investor in productive assets. I call this the advantage of “ownership over loaner-ship.”

The bottom line is that no one, I repeat, no one, is capable of timing the market. We can occasionally make a lucky guess, but it is always only a guess. However, the price for being wrong is permanent because of the waste of the time that we spend waiting. Moreover, even if we guess luckily, we’re overlooking two important facts. First, short-term price volatility will inevitably pass, as quality businesses will return to gains over the longer run. Second, holding cash can result in missing dividends and dividend increases, especially if we wait too long. As I stated in my previous article, I believe it is time in the market, not market timing that serves us best. Of course, this is only if we’re investing when valuations are sound or if we’re lucky enough to find stocks that are undervalued.

Furthermore, in his best-selling book One Up On Wall Street, Peter Lynch devoted his entire chapter 5 to this most important concept. Peter titled the chapter “Is This a Good Market? Please Don’t Ask.” The following excerpts from the chapter also support my views: “I’d love to be able to predict markets and anticipate recessions, but since that’s impossible, I’m satisfied to search out profitable companies as Buffett is. I’ve made money even in lousy markets, and vice versa.” And then later he said “Pick the right stocks and the market will take care of itself.”

This brings me to a few comments about the advantage of investing in quality dividend paying stocks with legacies of raising their dividend each year. To my way of thinking, the practical objective of investing in high quality dividend growth stocks is to be a long-term owner of the business (stock). Dividends are only beneficial if you intend on owning the company for a long enough period of time to collect a series of dividends. When you do, the steadily-rising dividend income stream pays you to wait for volatility anomalies to work themselves out.

This is what so many dividend growth investors are referring to when they state that they do not worry about volatility. Of course, they don’t like to see the price of a stock they own go down, but because they are focused on the dividends, they are given the confidence to stay the course. Moreover, the most astute among them recognize that as long as business remains good (earnings and dividends grow) price will take care of itself, as Peter Lynch stated above.

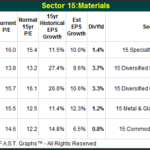

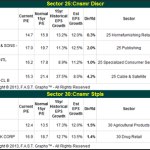

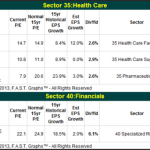

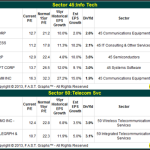

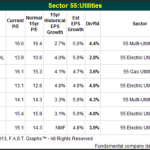

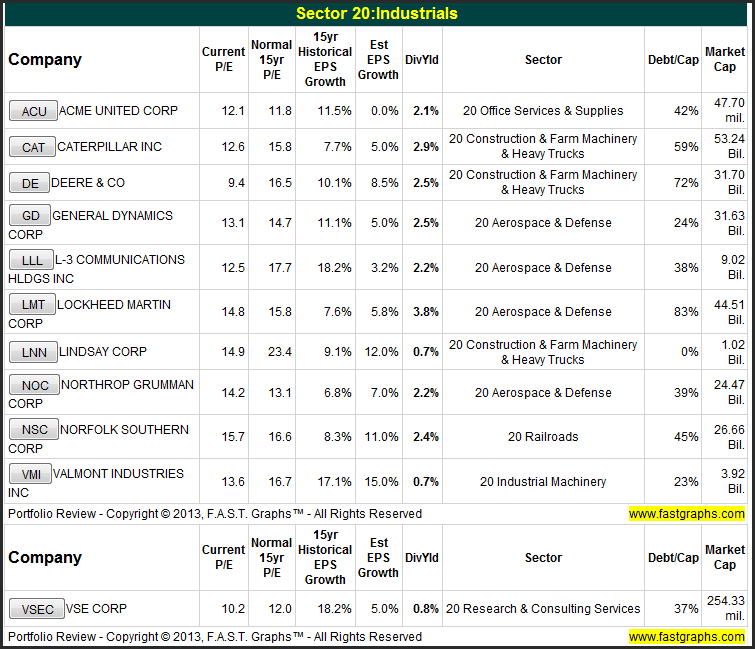

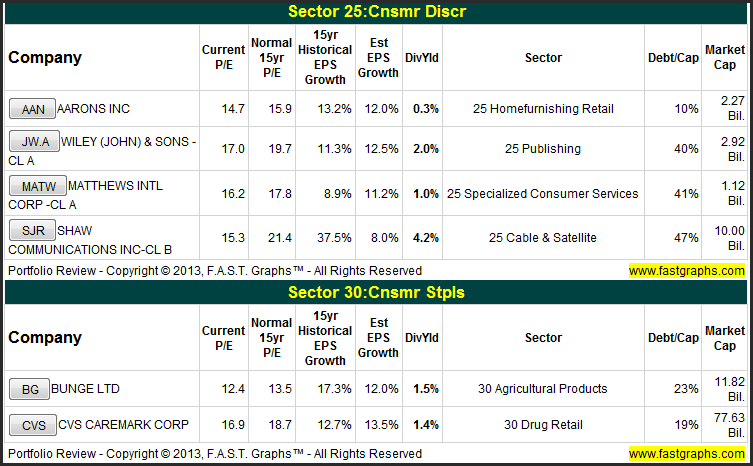

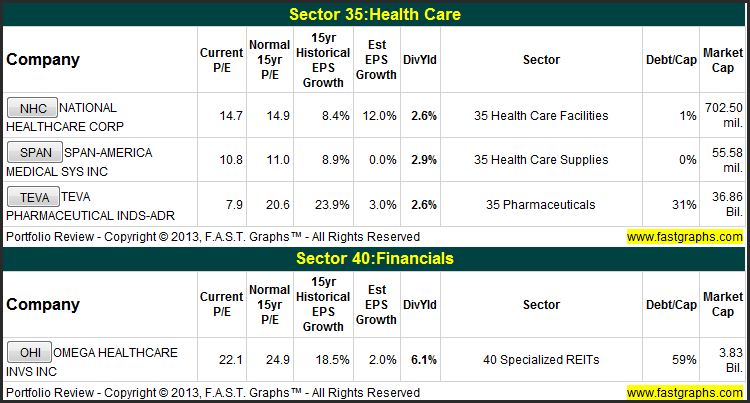

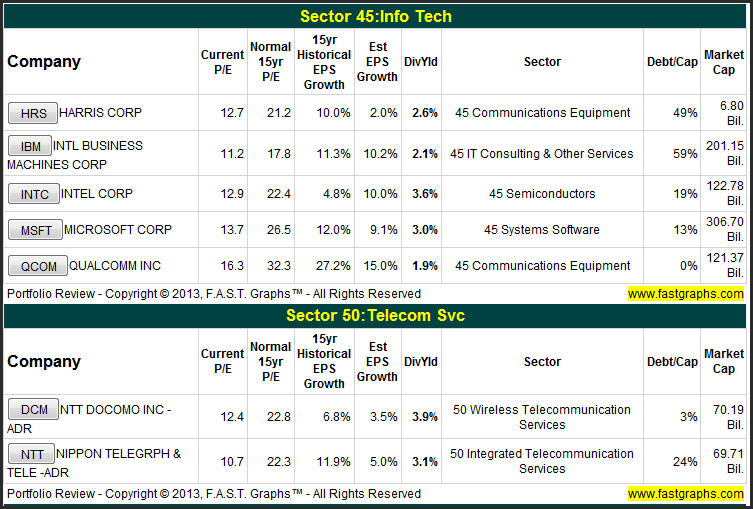

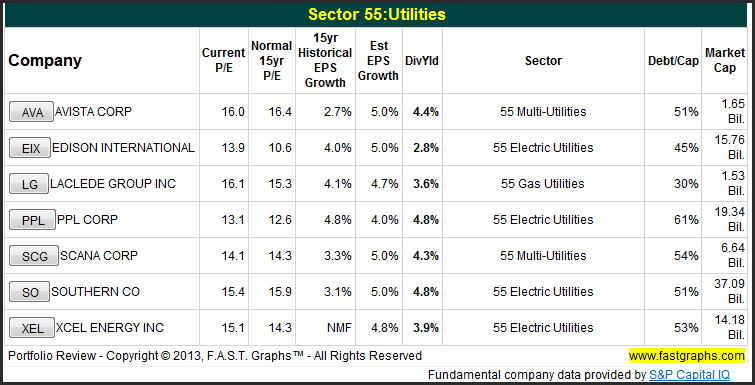

47 Fairly Valued Dividend Contenders Today

For those readers unfamiliar with the term, a Dividend Contender is a dividend paying stock that has increased their dividends every year for 10 to 24 straight years. Therefore, although not members of the more elite Dividend Champions or Aristocrats representing companies that have increased their dividend for 25 or more straight years, Dividend Contenders represent a fertile ground for investors seeking an increasing dividend income stream.

Nevertheless, even though a steadily-increasing dividend income stream is a powerful and valuable metric, it is not the only consideration. As I have stated numerous times, even the best of companies can become overvalued, and when a company becomes overvalued risk increases and return potential is diminished. Therefore, I have screened the entire list of Dividend Contenders provided by fellow Seeking Alpha author David Fish’s CCC lists, one company at a time, looking for fair value or below.

Out of the 209 Dividend Contenders available, I found the following 47 selections that I felt represented companies that were currently at or below fair value. Moreover, I excluded financials from my primary list for reasons I will discuss later. However, I did include one REIT in the list because I consider REITs a unique financial that should be given a separate classification all of their own. Additionally, I think it’s important to point out that even though each of these candidates are on the Dividend Contenders list, that does not to imply that each is an appropriate selection for every unique dividend investor’s needs or goals.

On the other hand, I do believe there are selections on the list that would meet every dividend investor’s specific needs. Therefore, I suggest that the reader ignore those that are not appropriate specifically to them, and focus their attention exclusively on those that are. I present the following list of fairly valued Dividend Contenders by sector. This illustrates that the opportunity for compiling a diversified portfolio of Dividend Contenders is readily and currently available.

Before I move on there is one caveat I would like to point out. Lists such as the Dividend Contenders are dynamic, and therefore, subject to change. Therefore, I suggest checking out the recent article by David Fish covering streaks in jeopardy. The reader would be advised to check the streaks in jeopardy for any Contenders that might fall off the wagon if their dividends are not soon increased.

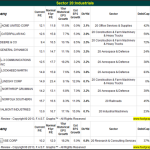

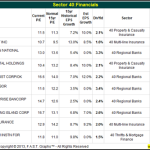

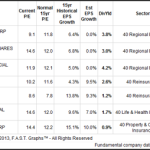

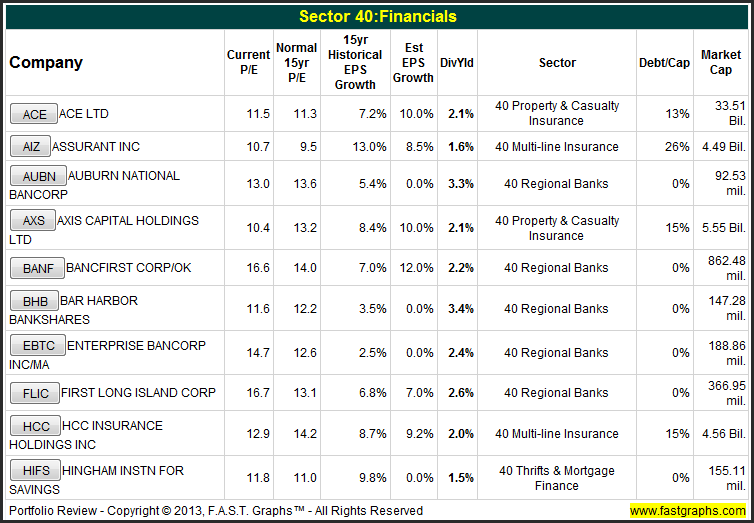

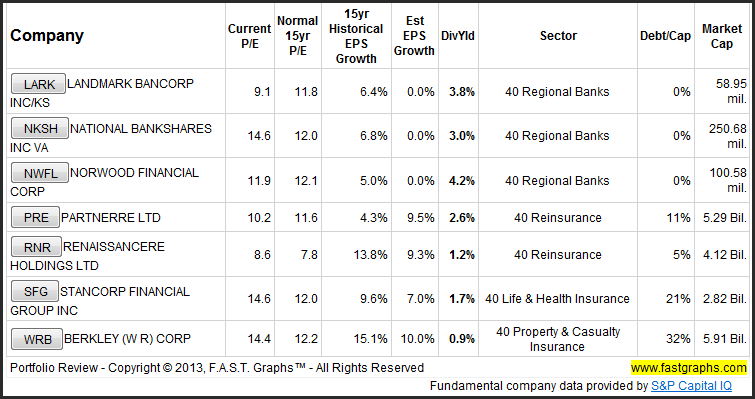

Financials: Special Contender Category

In addition to the 47 candidates listed above I offer a special category exclusively comprised of financials. I found 17 additional Dividend Contender candidates in the financial sector. I presented them separately for several reasons. First of all, this is a sector that has been in broad disfavor by the market since the financial debacle, which led to the Great Recession of 2008. Therefore, I view this as an industry that is out-of-favor, but also perhaps full of opportunity for the more aggressive dividend investor.

In addition to just being out-of-favor, there are many other factors that might indicate greater risk with Dividend Contenders in the financial sector. For many of them, size, or lack of it, is one of those risk factors. A review of the market cap column reveals numerous small to even microcap companies. Size can actually represent a two-edged sword. On the negative side, small companies may not have the resources or financial strength that a prudent dividend investor might want or need. But, on the positive side, small size might provide the opportunity for easier and/or faster future growth of both capital and dividends.

Finally, since valuations are low relative to the average company, this might support taking on the greater risk associated with many of these financials. I will let the reader make those judgments for themselves, and will only add that each company on the list has raised their dividend for at least 10 consecutive years. And of course, as I always wholeheartedly support when evaluating all prospective investments, research, due diligence and continuous monitoring is always necessary and required.

My Personal Favorites For High Current Income, Growth and Income Or Total Return

Although I consider all of the above Dividend Contender candidates to be fairly valued or close to it, I do not consider all of them appropriate for every dividend growth investor. In other words, as I previously stated, not all Dividend Contenders will possess the appropriate characteristics that fit each individual investor’s specific and unique goals, objectives and risk tolerances.

Some dividend growth investors, especially those that are already in retirement, might require high current income and safety over growth. Other dividend growth investors, perhaps with a longer time horizon, may be more interested in total return, and be more willing to take on a little risk to get it. On the other hand, I believe there are solid candidates within the group that can appropriately meet each investor’s unique needs. Therefore, I offer the following more detailed look at specific fairly valued Dividend Contender candidates that possess differing characteristics of growth, yield and quality.

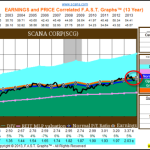

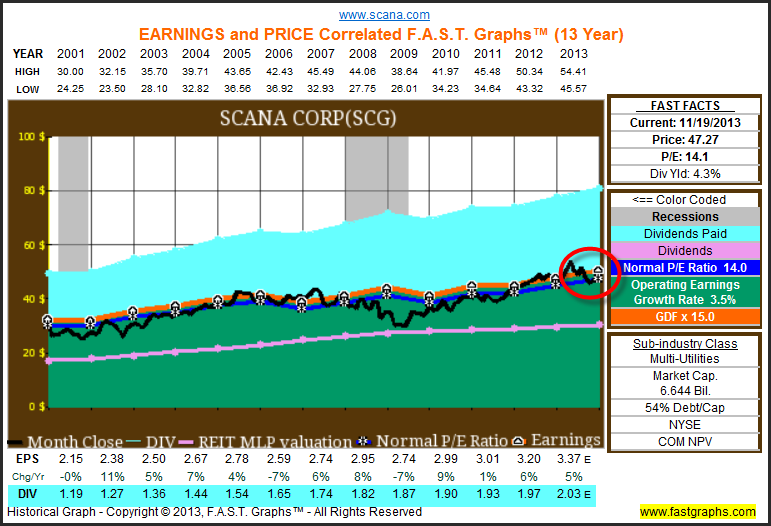

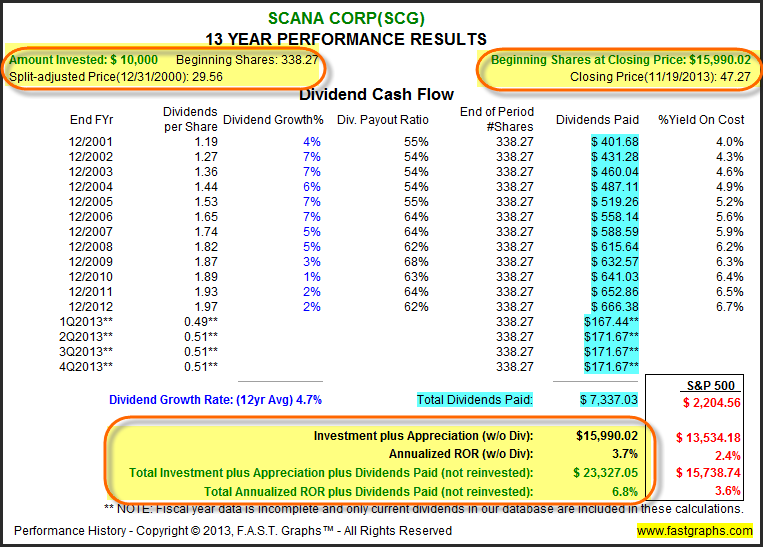

SCANA Corp. (SCG): For High Current Income-13 Consecutive Years

Personally, I have long considered utility stocks as the closest alternative you can get to a bond when investing in equities. Utility stocks are regulated, and as such offer little in the way of growth. However, they do have a legacy of producing above-average current dividend yields and generally low price volatility. Therefore, I strongly suggest only investing in utility stocks when valuations are sound, or better yet low.

Earlier this year, possibly as a flight to quality, utility stocks in general, to include favorites of mine such as SCANA Corp., became overvalued. However, as it will inevitably happen, many have seen their prices return to fair value starting in April of this year. I placed a red circle on the SCANA graph that reveals its recent return to fair value. For a more detailed perspective of my personal views on SCANA, the reader can check out my recent article on the company published in Forbes.

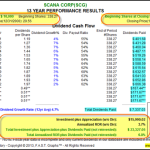

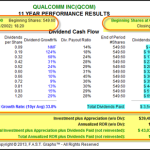

The following performance report covering SCANA’s performance during its recent 13-year streak that qualifies it as a Dividend Contender, illustrates why I like them as an income investment. Note the significantly higher cumulative total dividends paid versus the S&P 500.

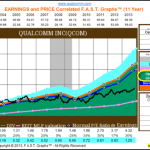

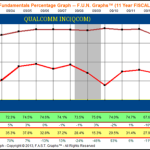

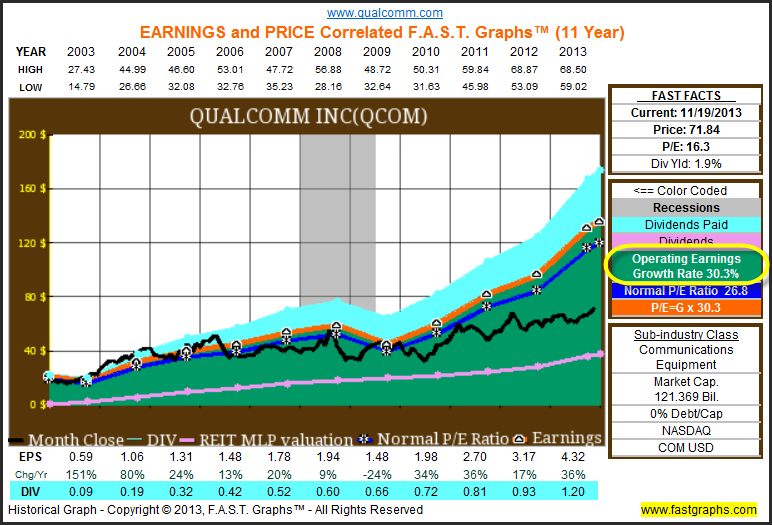

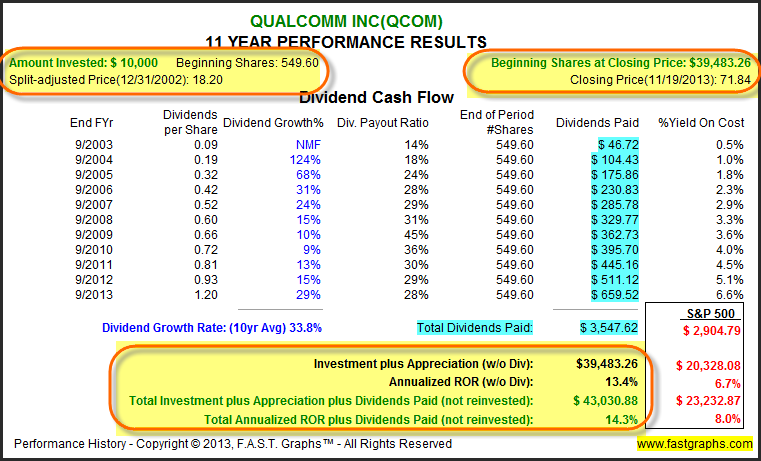

Qualcomm Inc. (QCOM): For Above-Average Growth and Income-11 Consecutive Years

My next favorite Dividend Contender, Qualcomm Inc., is offered for the consideration of those dividend growth investors interested in above-average total return. For a more detailed explanation on Qualcomm here is a link to a recent article published by my Associates at F.A.S.T. Graphs™.

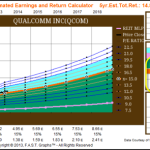

In short, Qualcomm is a global company founded in 1985 that designs, develops, manufactures, and markets digital telecommunications products and services. The company’s passion is “to continue to deliver the world’s most innovative wireless solutions.” As the following Earnings and Price Correlated graph reflecting their streak of 11 consecutive years of dividend increases reveals, operating earnings growth exceeding 30% per annum is clearly above average.

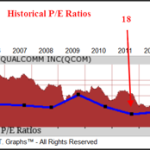

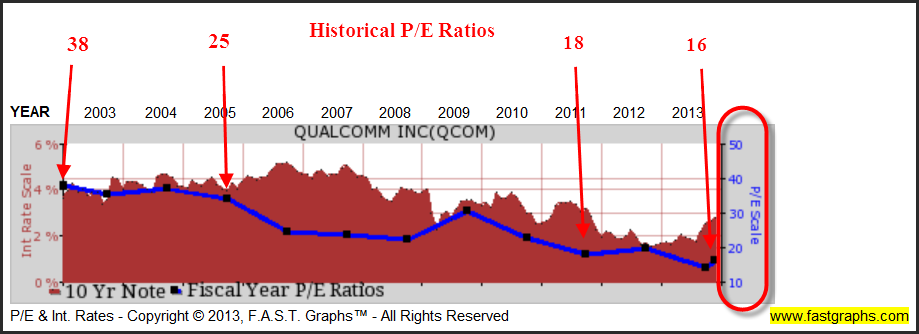

However, before I report the performance associated with the above graph, I thought it would be interesting to look at how Qualcomm’s P/E ratio has essentially been cut in half since the beginning of 2003. If you only had this statistic to rely on, it would be easy to assume that performance might be below average over this time frame.

However, we discover superior long-term performance in spite of the shrinking P/E ratio illustrated above. I believe this speaks loudly to the power of above-average earnings growth. Even though Qualcomm’s P/E ratio has shrunk, and in spite of the fact that the stock is currently at fair value, Qualcomm has soundly outperformed the S&P 500 on both total cumulative dividends and capital appreciation.

Qualcomm is a widely-followed stock and 43 analysts reporting to Standard & Poor’s Capital IQ expect the company to grow earnings at approximately 15% per annum over the next 5 years. On that basis, Qualcomm continues to represent above-average long-term growth opportunity that is currently fairly valued by the market on that basis.

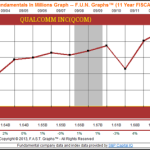

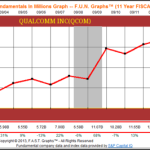

Qualcomm is clearly a powerful growth company that has consistently increased its book value or common equity per share (ceqps) over the years. Moreover, growth of book value has accelerated in the last 2 years (see the highlights at the bottom of the graph).

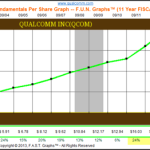

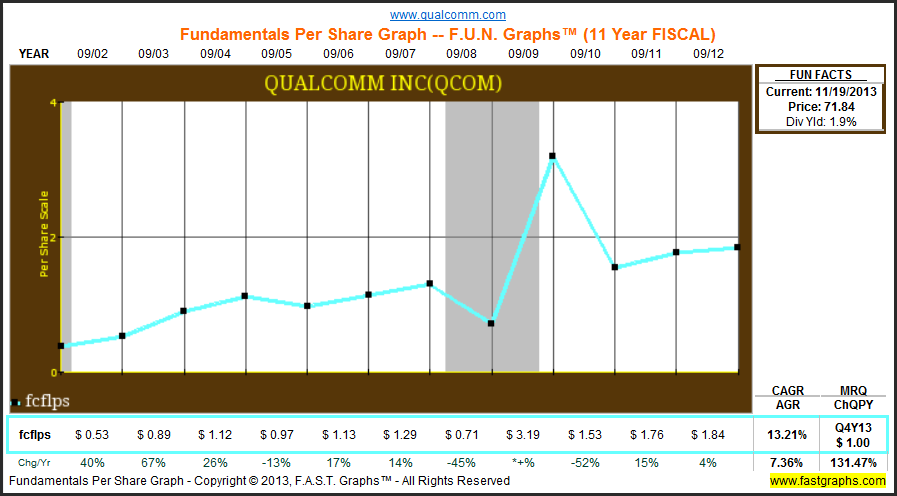

FUN Graphs calculates free cash flow after dividends have been paid. Clearly, Qualcomm has plenty of free cash flow left over.

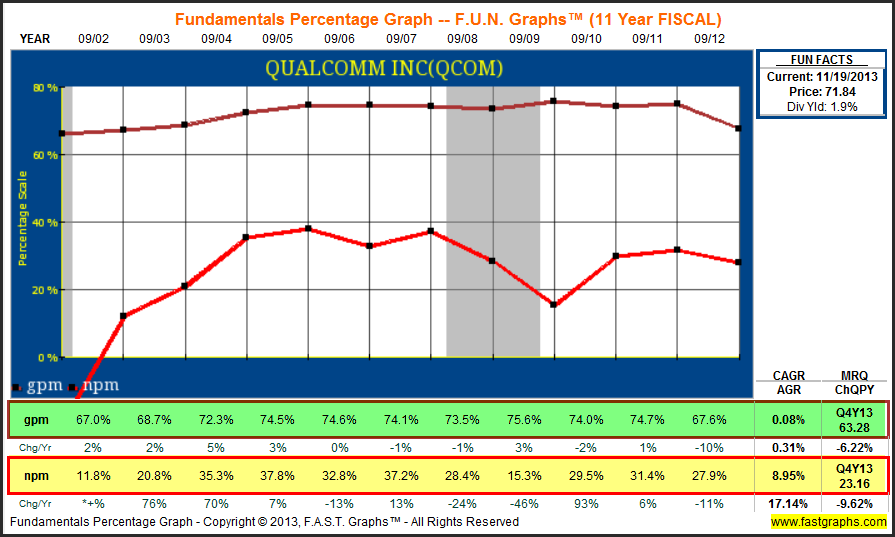

I like to see a company that I’m considering investing in generating high gross profit margins (GPM). Even better, I like to see high net profit margins (NPM) follow. Qualcomm passes both of those tests with an A+ grade, in my opinion.

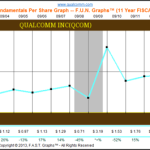

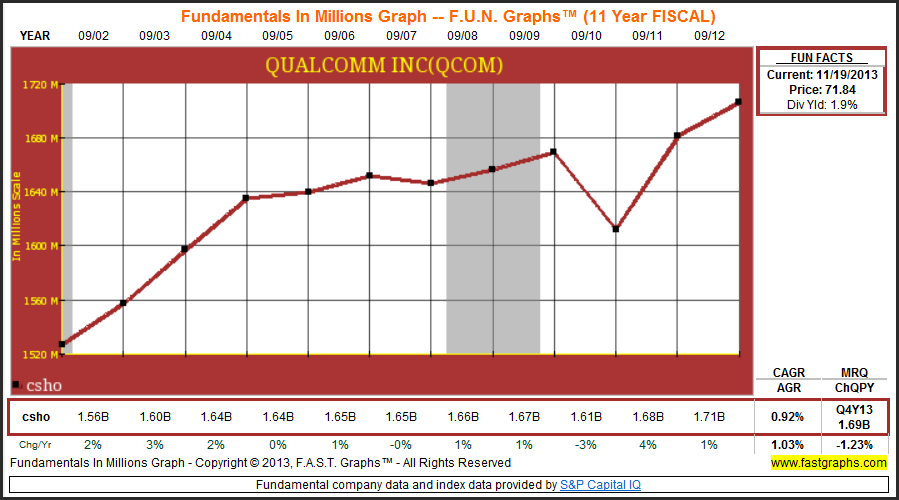

One possible negative regarding Qualcomm is the moderately dilutive aspect of their share count. Common shares outstanding (csho) have been increasing over the past 11 years, albeit at a moderate to low rate of approximately 1% per annum. However, on September 11, 2013, Qualcomm announced a new $5 Billion Stock Repurchase Program.

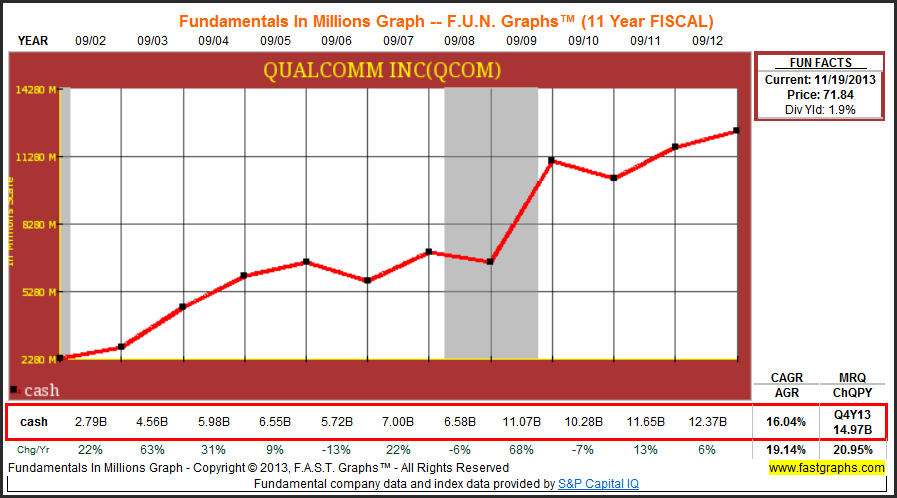

On the other hand, Qualcomm has almost $15 Billion of cash reported during their most recent quarter (MRQ). Consequently, they possess ample resources to support continuous R&D, their newly announced buyback and future acquisition opportunities.

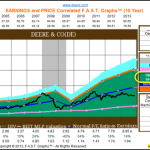

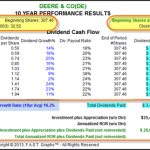

Deere & Co. (DE): Quality and Very Low Valuation For a Leveraged Total Return-10 Consecutive Years

Deere & Co. founded in 1837 is clearly an established company. As the Earnings and Price Correlated graph below indicates, the occasional moderate cyclicality with their earnings is not unusual. Moreover, consensus estimates expect a moderate dip in earnings for fiscal year 2014 ending October 31. Perhaps this explains the recent weakness in their share price.

However, over the longer term analysts expect earnings growth exceeding 8% per annum. I believe this forecast is supported by forecasts for a need for approximately $5 trillion in global infrastructure investment over the next two decades by the World Economic Forum. Deere & Co. is very likely to receive their fair share of business based on long-term future worldwide infrastructure needs.

In spite of its current low valuation, Deere & Co. has generated above-average shareholder returns during the time they have qualified as a Dividend Contender. Both capital appreciation and cumulative dividend income has exceeded the average company as represented by the S&P 500. Additionally, their dividend growth rate has averaged over 16% per annum since 2004.

For additional insight into Deere & Co., I suggest that readers might follow the following link to widely-recognized fellow Seeking Alpha contributor and instablogger Chowder and how his popular Chowder Rule applies to his recent purchase of Deere & Co. on November 14, 2013. The following link takes you to his Project $3 Million blog.

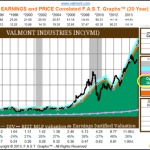

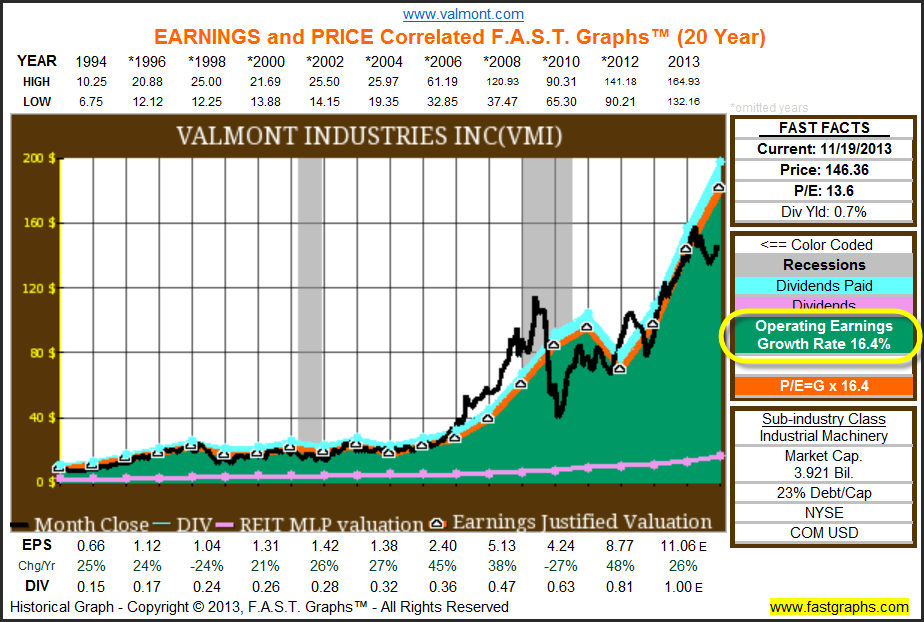

Valmont Industries Inc. (VMI): For High Total Return with a Dividend Kicker

Valmont Industries may not meet the needs of dividend growth investors seeking high yield. However, this Dividend Contender has produced strong total returns for its shareholders. Therefore, I offer it as a candidate for potential high total return with a growing, but small current yield, opportunity for above-average total return. In order to reveal the total opportunity that Valmont Industries possesses, I offer the following review via FAST Graphs™ by running the company over different time periods starting with 20 years (the maximum).

As you can see from the 20-year historical graph below, Valmont Industries’ stock price (the black line) has closely tracked and correlated with earnings (the orange line) which have grown at over 16% per annum since 1994. Also note that the company does pay a dividend, but the dividend payout ratio is quite low (the area below the pink dividend line). This might indicate a high potential for a future increase in their payout ratio.

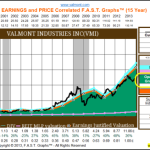

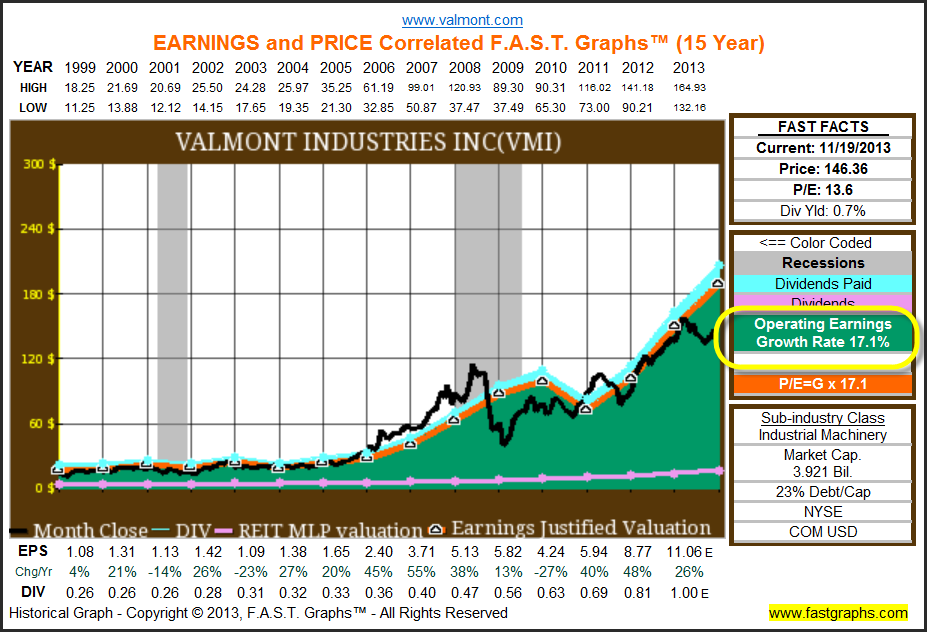

One of the great advantages of the dynamic FAST Graphs™ research tool is the ability to analyze a company over differing historical time frames. I routinely evaluate any company I look at by starting with a long-term 20-year graph followed by successively shorter time periods. This allows me to determine whether earnings growth is accelerating, decelerating or remaining constant.

A review of the 15 calendar year historical graph on Valmont indicates a slight acceleration of growth at over 17% per annum versus 16% growth seen in the 20-year example above. To me this indicates that above-average growth has been reasonably consistent.

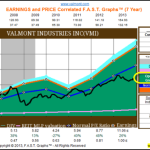

Normally I like to cut my time frames off five years at a time. However, currently I like to examine a company just prior to entering the Great Recession of 2008. I feel it’s important to analyze how a company performed through a recession. As it relates to this article, the most important aspect of Valmont Industries’ record is how they increased their dividend each year since 2007.

It’s also interesting to note that earnings growth was actually quite strong during the recession, although it faltered a bit in 2010. But perhaps most interesting of all is how earnings growth over the past seven calendar years has actually accelerated to over 24% per annum. Valmont Industries is a mid-cap company at $3.9 billion, which indicates that the company is small enough to continue growing at a high rate.

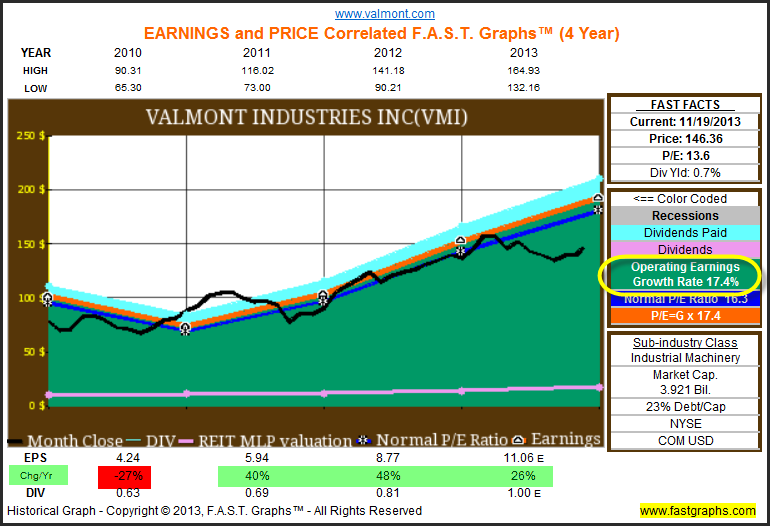

Finally, I offer the last four calendar year time frame that reveals several interesting facts. First of all, notice how stock price has tracked earnings and how the average earnings growth rate has continued to average over 17% per annum. But even more interesting is how earnings growth has accelerated since 2011 (see the highlights at the bottom of the graph). For the past three calendar years Valmont Industries’ earnings growth has averaged over 37% per annum. Consequently, I felt this Dividend Contender represents an intriguing long-term total return candidate.

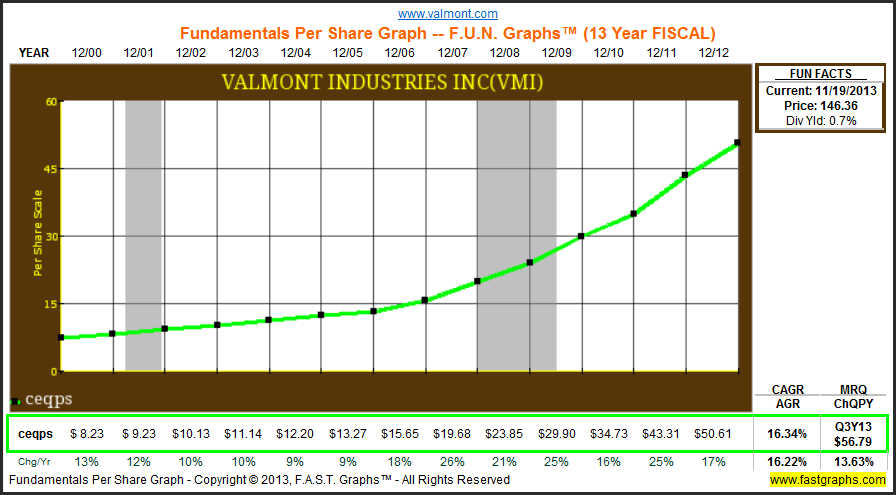

Finally, for those that like to focus on book value, Valmont Industries has increased their book value or common equity per share (ceqps) at a very high rate over the past 11 fiscal years. Although there is not a lot of yield here, growth potential is intriguing. However, further due diligence is suggested.

Summary

The primary motivation behind my writing this article, and my previous article, was to provide the readers with a list of high quality dividend growth stocks that appear fairly valued in today’s market. However, my secondary reason, but of equal importance, was to present logic and evidence supporting the folly of worrying about a potential market drop, therefore, freezing investors into inaction.

First of all, I believe it’s important that investors realize that forecasting the near-term direction of the market is impossible. Short-term market behavior is totally unpredictable, in spite of what many might believe are evidentiary facts indicating an imminent drop. The following quote from a prominent magazine represents a quintessential example of the kind of information investors are basing their unwillingness to invest their capital on.

“The U.S. economy remains almost comatose … the economy is staggering under many structural burdens, as opposed to familiar cyclical problems … The structural faults represent once in a lifetime dislocations that will take years to work out. Among them: job drought, debt hangover, the banking collapse, the real estate depression, the healthcare cost explosion, and the runaway federal deficit.”

Although I believe the above paragraph precisely describes many investors’ current views about our economy (these would include professional and lay investors alike, as well as most journalists and economic prognosticators). However, there is one problem with the above paragraph; it was written in Time Magazine on September 28, 1992, more than 20 years ago. Isn’t it amazing how that message continues to be promulgated after all this time? We continue to be inundated, even pounded, with this same provocative and negative theme in what seems like an endless loop of fear mongering. Notice the banner at the top left-hand corner of the Time Magazine cover page (below) of the edition that included the above paragraph:

Since the above Time magazine article was written, the stock market as measured by the S&P 500 is up over 5-fold. Moreover, high quality Dividend Champions and Contenders have done significantly better. For example, Dividend Contenders Deere & Company would be up over 10-fold, Valmont Industries would be up over 23-fold. Even conservative Dividend Champions such as McDonald’s and Procter & Gamble would be up over 9-fold, and Johnson & Johnson would be up over 13-fold. All of these examples are calculated with dividends reinvested.

Conclusions

I consider it an absolute fact that it is impossible to predict the short-run movement of the stock market, or any individual stock for that matter. On the other hand, I further consider it an absolute fact, that a reasonable calculation and/or estimate of fair value is knowable and doable. Perhaps, not with absolute perfect precision, but certainly within a reasonable enough range of accuracy from which to be confident enough to invest.

Conceivably, the market might drop 10% or even 20% in the near term, again, it is unpredictable. However, when you consider that the Dividend Contenders on the lists provided in this article, and the Dividend Champions in my most previous article all went through the worst recession since the Great Depression without a dividend cut, speaks volumes about their attractiveness as income-producing vehicles.

In my humble opinion, it is wise and prudent to invest in high-quality blue-chip dividend growth stocks with long histories of increasing their dividend whenever you can find them at sound valuations. Because even if a short-term market drop did occur, and the odds are 50-50 that it might, over the longer run it really doesn’t matter. The great majority of every company I have written about in these last two articles have recovered from their recession lows. Moreover, all of them are currently higher than they were when their stocks were trading at fair value just prior to, during and after the Great Recession.

But most importantly, all of the companies on both lists did not miss a dividend increase in any single year during that time frame. I believe the evidence is quite clear, that as long as you invest in a quality blue-chip dividend paying company when you can find it at fair value, your income is likely to grow each year, and your long-term capital appreciation potential will reflect the success of the business behind the stock you invest in.

Not only does it not pay to wait for what might be or might not be a phantom occurrence, the time cost can be egregious. Invest in quality at fair value, and time becomes your friend and ally. As Warren Buffett advised in his Berkshire Hathaway 1994 annual report: “Imagine the cost to us, if we had let a fear of unknowns cause us to defer or alter the deployment of capital. Indeed, we have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist.”

Finally, I feel it’s only fair to point out that not every company on the lists in this article or my prior article will all be excellent long-term investments. On the other hand, I believe the odds are very high that the vast majority of them will, as they have been in the past. Therefore, and as always, I highly recommend conducting further due diligence before investing in any of them, and continuous monitoring of the businesses behind the stocks after you do. In Part 3, I will cover Dividend Challengers.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Disclosure: Long QCOM, SCG, ARLP, COP, OXY, BBL, CAT, DE, LLL, GD, IBM, LMT, INTC, AAN, MSFT, TEVA, OHI at the time of writing. I am long QCOM, SCG, ARLP, COP, OXY, BBL, CAT, DE, LLL, GD, IBM, LMT, INTC, AAN, MSFT, TEVA, OHI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source:

What Stock Market? These Dividend Contenders Are Not Overvalued – Part 2

This article is from:

What Stock Market? These Dividend Contenders Are Not …

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}