Will Rising Rates Kill the Stock Market?Pragmatic Capitalism …

By Lance Roberts, CEO, StreetTalk Advisors

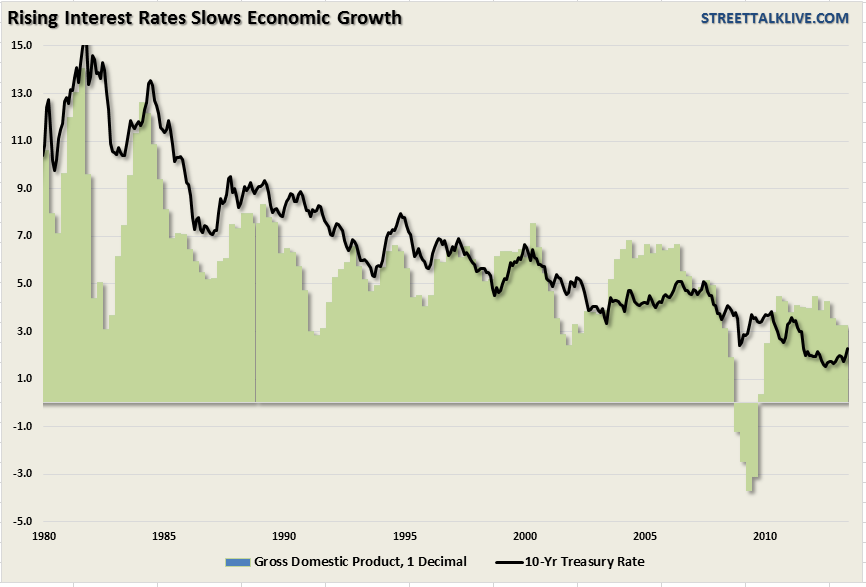

If you have been watching television, or reading headlines much as of late, you are undoubtedly aware that interest rates have risen. The current belief is that rising interest rates are a sign that the economy is improving as activity is pushing borrowing rates higher. In turn, as investors, this bodes well for corporate profitability which supports the current valuations of stocks in the market. While this seems completely logical the question is whether, or not, this is really the case? The chart below shows the 10-year treasury rate versus the economy as represented by GDP.

It is not surprising to find that rising interest rates negatively impact economic growth. As I discussed in “Evaluating 3 Bullish Arguments:”

“Rising interest rates are potentially a huge problem for the markets and the economy. Rising rates increase borrowing costs, carrying costs, and mortgages while reducing profitability, consumption and production. If the prognosticators of a bond market reversion are ‘right,’ like Bill Gross, it will not be good for stock market investors.”

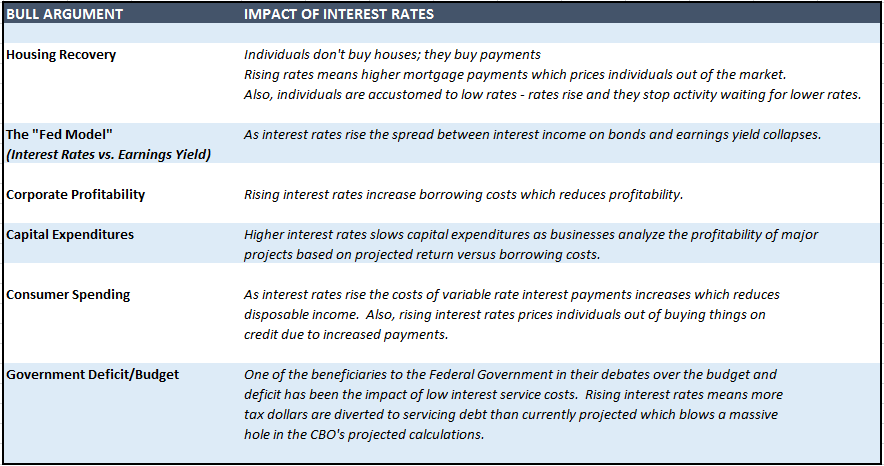

Let me explain that statement a little more thoroughly. The table below lists the various“bullish” arguments for the stock market and the impact caused by rising interest rates:

As you can see higher interest rates are not bullish for the economy or the market overall. However, it is important to remember that there is a significant lag effect between increases in interest rates and the impact on the markets and economy. The problem for investors, in general, is their inherent “immediacy bias.” Investors assume that if “Event A” doesn’t have an immediate impact on “Event B” that the analysis is wrong and that “this time is different.”The reality is that the lag effect is generally discounted by emotional biases which ultimately leads to poor investment decision making.

However, before I discuss the impact of rising rates as it specifically relates to the stock market, it is important to put the recent spike in rates into some context. The chart below shows the long term history of the 10-year interest rate.

As you can see the recent “spike” in rates is really nothing more than a “reversion” in rates from a historically low level back to the top of the long term downtrend. As with all things related to financial markets, and the economy, when things deviate well beyond their long term means (red dashed line) there is historically a “snap-back” that occurs. That “snap-back,” or reversion, could currently take rates back to 3.5%. While such a level is still extremely low by historical standards it is potentially high enough to create sufficient drag on an already weak economic environment.

While the current spike in rates has caught many participants by surprise; it is important to keep it in perspective. At the moment nothing has changed in overall long term down trend of interest rates. It will take increasing rates of economic growth, increases in wage growth and full-time employment, rising monetary velocity and upwardly trending inflation to change the long term trend of interest rates higher. Unfortunately, at the moment, the economic environment that currently exists is not supportive of such factors.

What’s Pushing Rates?

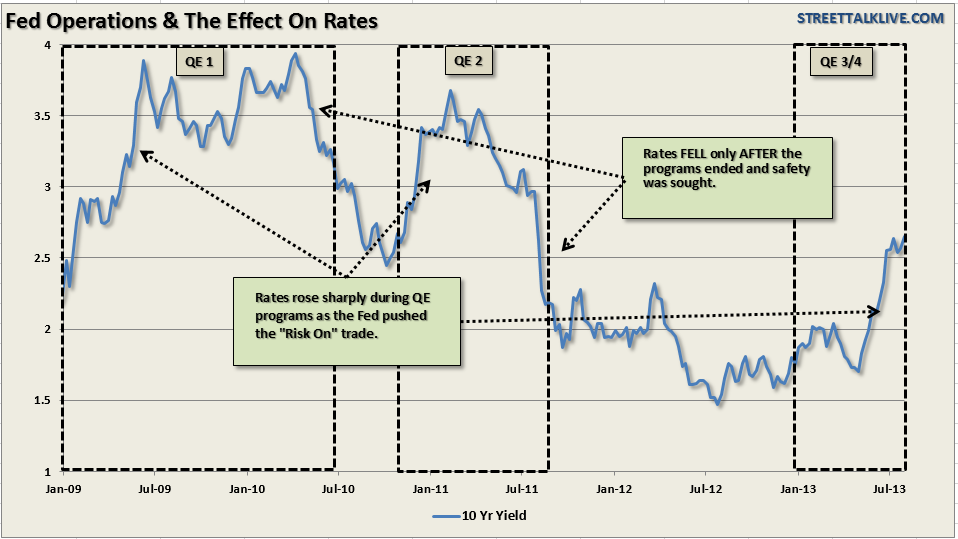

If it really isn’t economic growth driving rates higher then the question becomes “what is?” As I have discussed in “Clues To Watch For The End Of QE Infinity:”

“During QE programs interest rates have risen as the ‘risk’ trade pushed money flows into stocks. However, the opposite occurred at the end of programs as money fled from stocks and into the perceived ‘safety’ of bonds.”

The current move higher in rates actually has much less to do with expectations of economic recovery, despite headlines to the contrary, but rather the impact of the Federal Reserve’s monetary interventions, (QE), on money flows.

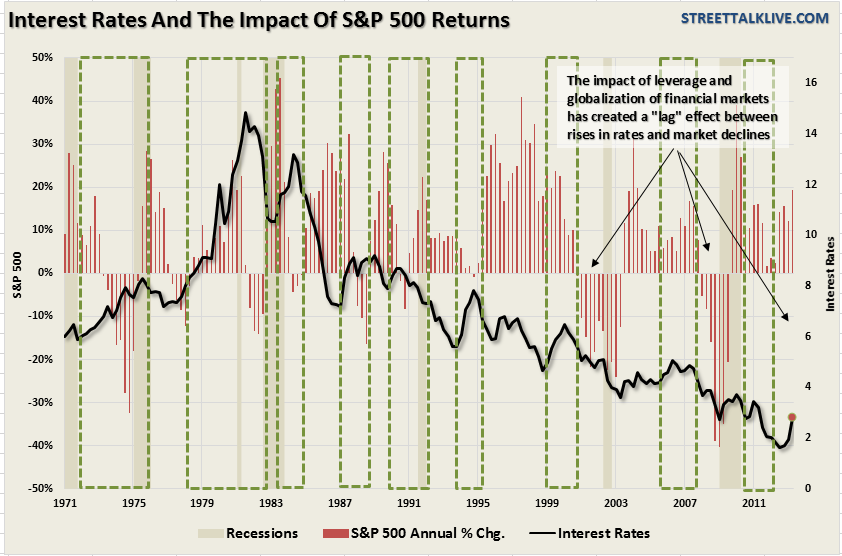

The problem for stock market investors is that the impact of rising rates is a clear negative on the economy and the stock market. As shown in the chart below – historical spikes in interest rates have always led to weaker stock market performance.

As discussed in the table above increases in interest rates slow economic activity, with a lag effect, which negatively impacts earnings, margins and forward guidance. Ultimately, and it may take several quarters to manifest itself fully, the fundamental deterioration leads to a reversion in stock market prices. As noted in the graph that “lag effect” has become much more pronounced since the turn of the century due to the impact of liquidity (from both the equity extraction during the housing bubble and QE programs currently), leverage via margin debt, and globalization of the markets through program trading. Regardless, the impact of higher interest rates will eventually negatively impact market returns which will then lead to the next decline in rates.

There are two important considerations. First, just because rates theoretically should not go lower – it also does not mean that they will start trending higher any time soon. Just take a look at Japan for what happens when a country becomes trapped in a liquidity cycle. Secondly, with economic growth already very weak it will not take much of an increase in rates to slow the economy further.

While the Federal Reserve may only slow their rate of bond purchases in the near future – less accommodative action is the same as “tightening” monetary policy. That decrease of policy accommodation will be amplified by the rise in interest rates which could conceivable create a bigger problem that the Fed and market participants are anticipating. While the current increase in interest rates hasn’t created any issues just yet – it certainly doesn’t mean that the pot won’t boil over the minute we quit paying attention to it.

View original –

Will Rising Rates Kill the Stock Market?Pragmatic Capitalism …

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}