#读书笔记 #1 A Random Walk Down Wall Street (Chapter 4)

Chapter 4: The Explosive Bubbles of the Early 2000s

1. The Internet Bubble

Most bubbles have been associated with some new technology (as in the tronics and biotech booms) or with some new business opportunity (as when the opening of profitable new trade opportunities spawned the South Sea Bubble). The Internet was associated with both: it represented a new technology, and it offered new business opportunities that promised to revolutionize the way we obtain information and purchase goods/service.

Bubbles are “positive feedback loops” – Robert Shiller (Irrational Exuberance).

In the first quarter of 2000, 916 venture capital firms invested $15.7 billion in 1,009 startup Internet companies. An astonishing 159 IPOs had been completed in the previous quarter. As happened during the South Sea Bubble, many companies that received financing were absurd. IN earlier times, one needed actual revenues and profits to come to market with an IPO. Some Internet companies had neither. We learned that investors would throw money at businesses that only five years before would not have passed normal due diligence hurdles.

Security Analyst $peak Up

Security analysts always find reasons to be bullish. They seldom utter the “sell” word, because they do not want to endanger current or future investment banking relationship or to offend corporate chief financial officers. Traditionally, ten stocks were rated “buys” for each one rated “sell”. But during the bubble, the ratio was almost 100:1.

New Valuation Metrics

Somehow, in the new Internet world, sale, revenues, and profits were irrelevant. In order to value Internet companies, analyst looked instead at “eyeballs” – the number of people viewing a Web page or “visiting” a Web site. Particularly important were numbers of “engaged shoppers” – those who spent at least 3 minutes on a website. “Mind share” was another popular non-financial metric.

Special metrics were established for telecom companies. Security analysts clambered into tunnels to count the miles of fiber-optic cable in the ground rather than examining the tiny fraction that was actually lit up with traffic.

The Writes of the Media

The bubble was aided and abetted by the media, which turned us into a nation of traders. Like the stock market, journalism is subject to the laws of supply and demand.

The Internet itself became the media. The Internet had democratized the investment process, and it played an important enabling role in perpetuating the bubble. Online brokers were also a critical factor in fueling the Internet boom. Trading was cheap, at least in terms of the small dollar amount of commissions charged.

Cable networks such as CNBC and Bloomberg became cultural phenomena. Across the world, health clubs, airports and bars were permanently tuned into CNBC.

Fraud Slithers In and Strangles the Market

Speculative manias , such as the Internet bubble, bring out the worst aspects of our system. Many businesses were managed not for the creation of long-run vale but for the immediate gratification of speculators – “obliged” high short-term earnings, “creative accounting, etc.

Enron was only one of a number of accounting frauds. Various telecom companies overstated revenues through swaps of fiber-optic capacity at inflated prices.

Should We Have Known the Dangers?

Fraud aside, we should have known better. We should have known that investments in transforming technologies have often proved unrewarding for investors. In the 1850s, the railroad was widely expected to greatly increase the efficiency of communications and commerce. It certainly did so, but it did not justify the prices (collapses in August 1857). History tells us that eventually all excessively exuberant markets succumb to the laws of gravity.

Many villains: fee-obsessed underwriters; research analysts that could be pushed by commission-hungry brokers; corporate executives using “creative accounting” to inflate their profits. It was the infectious greed of individual investors and their susceptibility to get-rich-quick schemes that allowed the bubble to expand.

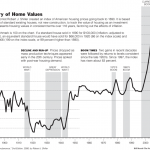

2. The US Housing Bubble and Crash of the Early 2000s

This bubble was undoubtedly the biggest US real estate bubble of all time. Moreover, the boom and later collapse in house prices had far greater significance for the average Americans than any gyrations in the stock market.

In order to understand how this bubble was financed and why it created such far-reaching collateral damage, we need to understand the fundamental changes in the banking and financial systems.

The New System of Banking

Old system is “originate and hold” system. Banks would make mortgage loans and hold those loans as assets until they were repaid. In such an environment, bankers were very careful about the loans they made. This system fundamentally changed in the early 2000s. New system is the “originate and distribute” model of banking – e.g. mortgage-backed securities, CDS (second-order derivatives), etc.

Looser Lending Standards

The financiers created structured investment vehicles, or SIVs, that kept derivative securities off their books, in places where the banking regulators couldn’t see them. In the new system loans were made with no equity down in the hopes that housing prices would rise forever. NINJA loans were common – loans to people with no income, no job , and no asset.

The government itself played an active role in inflating the housing bubble. Under pressure by Congress to make mortgage loans easily available, the FHA was directed to guarantee the mortgages of low-income borrowers. Indeed, almost 2/3 of the bad mortgages on the financial system as of the start of 2010 were bought by government agencies or required by government regulations. No accurate history of the housing bubble can fail to recognize that it was not simply “predatory lenders” but the government itself that caused many mortgage loans to be made to people who cannot afford them.

3. Bubble and Economic Activity

The bursting of bubbles has invariably been followed by severe disruptions in real economic activity. The fallout from asset-price bubbles has not been confined to speculators. Bubble are particularly dangerous when they are associated with a credit boom and widespread increases in leverage both for consumers and for financial institutions. Credit boom bubbles are the ones that pose the greatest danger to real economic activity.

Are the markets inefficient?

“The stock market is not a voting mechanism but a weighing mechanism.” – Benjamin Graham (Security Analysis). Valuation metrics have not changed. Eventually, every stock can only be worth the present value of the cash flow.

Market prices must always be wrong to some extent. But at any particular time, it’s not obvious to anyone whether they are too high or too low. Markets are not always or even usually correct. But no one person or institution consistently knows more than the market. (???)

Continued here:

#读书笔记 #1 A Random Walk Down Wall Street (Chapter 4)

See which stocks are being affected by Social Media