Bank of America Corp (BAC) news: Stock Market Myopia: Why …

Summary

Bank of America is still struggling with legacy issues, but most of its operations have been stabilized.

Many investors are mostly focused on the legacy issues, but they are neglecting the bank’s asset base.

Without the litigation provisions, the results would have, most likely, come higher.

The bank’s asset base, under normal conditions, should yield an ROA around 1%.

Introduction

Bank of America (BAC) went through some rough times in the past few years. During that time, Brian Moynihan was selected to be the new CEO and Warren Buffett invested in the company.

In 2013, the company was able to achieve around $10 billion in profits. However, when investors thought that the company was about to enjoy some calm quarters, suddenly, a $6 billion provision pushed the company back to quarterly losses.

Almost instantly, many stock analysts started screaming that BAC is clearly overvalued. Some argued that the litigation issues are here to stay. Others pointed out signs of underachieving performance in mortgage origination. Honestly, all this seems to be like if a basketball fan is watching a game using a magnifier, following only one player, thus ignoring all the other dynamics developing on the field.

I understand that the momentum is for bearish stances, however, I believe that the situation asks for a wider look.

The Blow – How big is it?

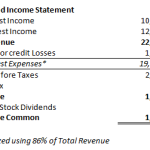

First of all, I think it is necessary to put the provision costs into perspective – after all, these are non-recurrent costs. If we exclude the $6 billion provision and use a normalized figure, we achieve the following results:

Table 1 – Normalized Income Statement (in USD millions) (Source: Bank of America, except for normalized figures)

Basically, I estimated non-interest expenses at 86% of total revenue, which is higher than the same ratio for previous quarters. Even using these conservative figures, the estimated result would have constituted an improvement around 12% in relation to 13Q1. Looking at the situation from this point of view, things do not seem so alarming.

What does really matter?

The point I’m trying to make is, when it comes to evaluating Bank of America, some investors seem to be suffering from myopia. They seem to believe that litigation will keep going on forever and mortgage operations will never recover. Well, they are right in one aspect: the company’s stock price must suffer. Or better, it must have suffered when news came out about litigation, bad mortgage operations and regulators trying to make an example out of BAC.

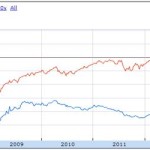

Graph 1 – Bank of America versus the S&P 500 (Source: Google Finance)

Actually, Bank of America not only heavily underperformed the S&P during the banking crisis, it keeps underperforming the S&P in the present (Graph 1). However, at the some point in the near future, it will most likely stop underperforming the S&P. The reason is simple: what really matters is the bank’s franchise:

- 5,100 banking centers

- $2.1 trillion in assets

- 57 million customers

- Merrill Lynch asset management operation

The main doubt was to know what would be the impact of the crisis in the bank’s asset base. Since the bank was able to hold together during the worst part of the crisis, I do not believe that the present is the time for pessimism. On the other hand, if investors just stand waiting for good indicators, when the good numbers arrive, it will be too late. Usually, the stock market does not forgive procrastination.

On the other hand, how can we be sure that the good numbers will arrive in the future? The answer is exactly in the four points previously stated. Basically, 57 million clients, $2.1 trillion in assets, a widespread agency network covering the US and the Merrill Lynch asset management unit are the asset base that will bring the bank back to good profitability. It is a question of adopting the right strategy to take the most out of the bank’s great asset base.

The bank’s strategy

The management team intends to pursuit a conservative set of business policies. The goal is to adopt a lean approach to the bank’s asset base, returning to core operations. The sale of non-strategic assets should help build a fortress balance sheet.

Therefore, the way to go for Bank of America is to focus on consumer and business banking, rehabilitate the consumer real estate services and leverage the Merrill Lynch unit. In the future, the bank’s results should be influenced by the conservative approach. Most probably, the bank will not have the swings in profitability that it had in the past.

Table 2 – Return on assets for BAC

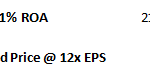

In Table 2, we can see that the bank has had some very good years, but it has performed very poorly in other years. In the future, it is expected that the bank will not have years as good as in 2006, but it will be able to avoid a streak of bad years like the 2008 to 2012 period. Therefore, I think that in the medium term (2-3 years), the bank should target a return on assets (ROA) around 1%. If the bank is able to achieve this figure, then the following valuation becomes reasonable:

Table 3 – Valuation for BAC @ 1% ROA

Conclusion

In my opinion, Bank of America owns one of the best asset bases in the US banking industry. On the same note, Brian Moynihan is adopting the right strategy by adopting a lean attitude toward the banks operations and by preferring a conservative banking management approach. A good sign is the fact that Warren Buffett seems to believe in the project. Putting it all together, I think that in the following years, the bank will be able to achieve profits around 1% of assets. If this materializes, I think that a valuation around $22.50 is easily achievable, representing a potential upside of more than 40% in relation to the present price of $16.13.

The main threat that I see in the near future is the possibility of some White House Administration deciding to cut the bank in pieces in order to end the too-big-to-fail bank species.

Source:

Stock Market Myopia: Why Investors Don’t Understand Bank Of America

Disclosure: I am long BAC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More…)

Continue reading here:

Bank of America Corp (BAC) news: Stock Market Myopia: Why …

{kind=link}

{kind=link}