Endowment payouts cut despite stock market soaring – The Guardian

Standard Life has cut payouts on endowment policies by 2%. Photograph: David Sillitoe for the Guardian

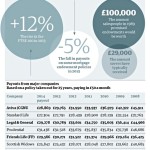

The millions of people who have clung on to mortgage endowment policies received more miserable news this week, with many insurers cutting payouts despite the rising stock market. The biggest endowment provider, Standard Life, said it was slicing 2% off payouts despite the 12% rise in the FTSE 100 index in 2013.

A typical 25-year policy maturing this year, where the saver has diligently paid in £50 a month, will pay out £27,304, compared to a projected £27,791 last year.

Others cut even deeper, with Legal & General knocking 5% off maturity payouts this year.

This is a far cry from the promises made to savers when the policies were taken out. Commission-hungry salespeople, who usually pocketed £1,000 or more from selling an endowment policy, enticed buyers with projected returns of around £100,000 when, in reality, they have been just a fraction of that.

The policies were mostly taken out to cover the repayment of a mortgage, but as shortfalls emerged, the companies were forced to compensate savers to the tune of more than £2bn for mis-selling.

Endowments maturing today have, in many cases, barely matched inflation over the past 25 years, and fallen well short of the money savers would have made if the cash was put, instead, into a low-cost “tracker” matching the gains on the FTSE.

Nutmeg.com, a low-cost investing website, prepared some figures for Guardian Money which assumed that instead of putting £50 a month into an endowment policy, the saver put it into a FTSE All-Share tracker fund.

It calculates that over 25 years the payout (taking into account charges) would have been £46,077 – or nearly 70% higher than the amount Standard Life is offering to its policyholders. “High fees often take away most of the gain”, says Nutmeg chief executive, Shaun Port.

But why are returns on endowments still falling despite a bumper year on the stock market? Insurers say it’s in part because endowments are not fully invested in shares – they are in a mix of bonds, property and cash, so they don’t fully reflect what’s happening to the FTSE. But, even so, Standard Life says its with-profits endowment fund earned 9.8% overall – leaving policyholders understandably puzzled as to why the cuts keep coming.

Patrick Connolly of financial advisers Chase de Vere says: “It’s disappointing because I really did think we would see increased payouts on endowments this year. What’s happening is that the providers are still playing catch-up on the losses they incurred before.

“Between 2000 and 2003, many with-profits endowments paid out more than they were generating from the stock market [which was falling heavily at the time] and people got more than they should have.”

But there is better news for savers into private pension schemes. Payouts at some companies are up between 4% and 7% this year, with a typical £200 a month policy held for the last 20 years giving a return of around £80,000.

Connolly says: “The payouts from Prudential compare favourably against other stronger with-profits providers such as Aviva and Legal & General, and are hugely superior to the weaker providers such as Scottish Widows.”

What should you do with your policy?

• Keep it If only one or two years away from maturity, keep paying in. Most “with-profits” policies have a valuable terminal bonus which you won’t receive unless you stay with it.

• Make it paid up Stop paying the monthly premiums but don’t take the proceeds until the maturity date. The advantage is you still qualify for the terminal bonus, although it won’t be as much as if you had continued.

• Cash it in Write to the provider and ask for a “surrender value” and whether there are any penalties for cashing in early. Also ask if there are any guarantees attached, which may make it more valuable. Then decide whether it’s still worth throwing money into it.

• Sell it This used to be a popular option, but the market has shrunk massively in recent years. It is, though, still possible to obtain a better price by selling it to a market maker who takes it on, carries on making the payments and takes the terminal bonus. Surrenda-link (surrendalink.co.uk/0800 919 021) is the best known in the traded endowment market. It generally buys with-profits policies that are at least five years old (though you only really get much of an uplift if the policy is 10-15 years old) and has a surrender value of at least £3,000.

• Get compensation More than £2bn has been paid out, but you have almost certainly missed the boat by now. You can make a compensation claim for mis-selling if you took the policy out within the last six years, which is unlikely as most were sold in the late 1980s and early 1990s. But you can also make a claim within three years of realising it may have been mis-sold. Contact the Financial Ombudsman Service at financial-ombudsman.org.

How your endowment payouts have fallen

Continue reading:

Endowment payouts cut despite stock market soaring – The Guardian

See which stocks are being affected by Social Media