Stock Market And Housing Stock Implications Of Trends In Lumber …

Summary

Lumber prices have been declining, as have those for panels.

Since the Great Recession ended, similar declines have preceded stock market sell-offs accompany the end of QE.

Thus the question arises as to whether the end of QE, due this fall, will mark a market top.

Background: Every week I look at the weekly trends in lumber and panel prices, and correlate them with the trends in the futures market for lumber as reported by FINVIZ. While no correlation should be expected to be valid going forward, I like to make decisions based on prior facts, and for whatever reason or perhaps by chance, these trends have “worked” since the Great Recession. I therefore report on them in this article.

Introduction: Housing has traditionally led the U.S. out of recessions, but with an aging population and a difficult job market for 20-somethings, the times, they are a-changing. Whether the authorities have been to some significant degree pushing on a string with all their efforts to support housing prices is unclear. What is clear is that housing has not “recovered.” Furthermore, an important component of building houses, lumber, has followed the reflationary efforts of the authorities up in price and now has faltered. At this point, five years after the recession officially ended, a decline in lumber prices may signal a beginning of a down cycle for housing. This article begins by presenting data that demonstrates the scope of the new bear market in lumber.

Lumber prices – moving on down: FINVIZ allows looks at one type of lumber that trades often enough to create a readable chart. On a one-year basis, it looks like this:

(click to enlarge)

On a multi-year basis, it looks like this:

(click to enlarge) The green line below the charts tracks commercial hedgers. The red and blue lines track the positioning of large and small speculators, respectively.

Looking at these two charts together, we can note that a new downtrend is in force. A classic rollover topping pattern is now present that I always respect, though of course no certainty exists of future movements from any particular chart pattern. This is in contrast to the classic bull market action seen until now, with concave upward moves from setbacks. We also note the presence of a lower high price on this current rollover compared with the prior high of summer 2013. No lower low has been made, though. Year on year, prices are down.

Another observation we can make is that prices of lumber are up from their lows a lot more than wages.

A different observation relates to the correlation of lumber’s price action and that of the stock market. We note that lumber bottomed in summer 2009, well before the homebuilding stocks (see below). Lumber then took a big tumble in March-April 2010, a few months before the stock market took its post-QE1 swoon. Lumber recovered, and again peaked well before the overall market in 2011, also in advance of the end of QE, this being QE2. Lumber again bottomed, making a higher low, before beginning the same unrelenting march upward in price as the stock market. Once again, it peaked in early 2013 before the “taper tantrum” that affected stocks (though it affected bonds more).

Now we have a fourth setback for lumber prices since summer 2009. Will this once again presage a playable downturn in the stock market? After all, once again QE is ending. Even though banks are lending again, whether they are lending wisely and well may determine how well the economy functions without the monetary and psychological crutch of quantitative easing.

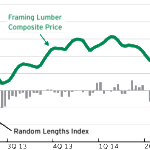

We can also look at lumber prices in a more detailed way by looking at the trade publication Random Lengths. This weekly comes out after the market closes on Fridays and shows both lumber and engineered product prices. The latest data are as follows:

This Week

Jun 6 Last Week

May 30 Year Ago

2013 Random Lengths Framing Lumber Composite Price* $375 $381 $340 KD Western S-P-F #2&Btr 2×4 R/L Mill Price 314 328 307 KD Eastern S-P-F #1&2 2×4 R/L, delivered Great Lakes 421 431 407 Green Douglas Fir Std&Btr 2×4 R/L (Portland) 300 315 295 Southern Pine (Westside) #2 2×4 R/L 412 406 345 KD Coast Hem-Fir #2&Btr 2×4 R/L 388 400 330 Ponderosa Pine (Inland) #2&Btr 1×12 R/L 750 750 600 * Weighted average of 15 key items

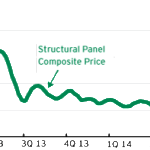

And for panels, it shows this:

(f.o.b. mill prices) This Week

Jun 6 Last Week

May 30 Year Ago

2013 Random Lengths Structural Panel Composite Price* $371 $382 $414 Southern (west-east) 15/32-inch 3-ply rated sheathing plywood 405-425 412-440 390-425 Southern (west-east) 15/32-inch 4-ply rated sheathing plywood 405-433 412-445 390-430 Western 1/2-inch 4-ply rated sheathing plywood 409 423 375 North Central 7/16-inch Oriented Strand Board 215 230 312 *Weighted average of 11 key items

The downturn in panel pricing has been severe. There is commentary about both of those, which you can read via the link. Since lumber and panels are largely used in the domestic home building and home improvement industries, price sends a signal about demand. This fits with various reports of a housing slowdown nationwide.

Housing stocks: Two of the major ETFs related to the housing market are iShares US Home Construction (ITB) and SPDR S&P Homebuilders ETF (XHB). Directionally, each tends to track the overall stock market, as seen by a comparison of ITB with the SPDR S&P 500 (SPY):

Of course, the housing debacle accounts for the overall underperformance, given that ITB was created shortly after the housing bubble had popped but the stocks had not yet “caught down” to the decelerating fundamentals. Over the past two and five years, though, ITB has outperformed SPY, but over the past year, SPY has outperformed ITB.

If declining lumber prices again lead declining stock prices as a whole, I’d expect ITB and XHB to follow the market down.

On their own merits, there is little special about ITB or XHB. Relative to the overall market and their own trading histories, I’d give each of them a “meh” rating.

Summary: I look at lumber prices often because I am guessing that relatively few other stock market investors do so, and because of their post-financial crisis correlation with stock prices, especially their habit to date of leading bear moves in stocks. The current and ongoing decline in lumber and panel prices is something I am paying attention to in my asset allocation. Given the age of the economic expansion, I’m interested in being proactive, and have been concentrating both in recession-resistant, lower-beta stocks or those secular growth stocks with GARP characteristics such as Alibaba (ABABA), with Yahoo! (YHOO) as its proxy, that have attractive valuations according to GARP principles. In contrast, I do not see homebuilders or other classic early cycle stocks as attractive right now.

With QE scheduled to end this fall (“the taper”), other past episodes of its ending, which have been associated with drops in lumber prices as have been occurring recently, may perhaps point the way toward unwanted market and economic trends by year-end.

Source:

Stock Market And Housing Stock Implications Of Trends In Lumber Prices

Disclosure: I am long YHOO. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Not investment advice. I am not an investment adviser. (More…)

View original post here:

Stock Market And Housing Stock Implications Of Trends In Lumber …

See which stocks are being affected by Social Media

{kind=link}