The Peril Of Stock Market Tunnel Vision [SPDR S&P 500 ETF Trust …

Tunnel vision is a major risk for stock investors today. As discussed in a recent article, nearly every major asset class beyond the U.S. stock market has struggled in 2013 with many on course to post declines for the year. And the magnitude of stock outperformance this year at over +20% versus all other major investment categories is unprecedented in recent market history. But in our stock obsessed capital markets, investors are completely unfazed by this fact with bearishness at quarter century lows according to Investor Intelligence. One might dismiss this disconnect as simply a clear sign that the global economy is finally on the mend and set to accelerate. But looking across the various components of the global stock market itself reveals ample evidence that this rosy scenario is not likely the case.

A quick glance at global stock markets reinforces the upbeat tone of the U.S. stock market. According to the iShares MSCI All Country World Index (ACWI), global stocks have risen over +19% year to date. While this pales in comparison to the +29% reading for the SPDR S&P 500 (SPY), it marks a strong year nonetheless. But when taking a closer look and dissecting returns across regions, markets and economies, a far more defined picture starts to emerge.

So which markets exactly have been the winners so far in 2013? In short, it has been the developed economies with the largest currencies if not the world’s reserve currency that have been directly benefiting in their own stock markets from the extremely easy monetary policy from their respective central banks. And in the spirit of all boats rising together, the benefits have been quite evenly distributed across these privileged markets.

Let’s begin with Europe. To begin, every major stock market in the Euro Zone is up +10% year-to-date. This includes the largest in the group such as Germany (EWG), France (EWQ) and the Netherlands (EWN), all of which are up over +20%. Even the beleaguered PIIGS have posted exceptional results this year, with Portugal up +14%, Ireland (EIRL) booming +44%, Italy (EWI) gaining +15%, Greece (GREK) elevating +31% and Spain rising +28%. While each of these economies has made progress to varying degrees, in short be noted that they certainly remain far from out of the woods. As for the other major non-Euro Zone markets in Europe, both the United Kingdom (EWU) and Switzerland (EWL) are generating solid double-digit returns for 2013. What do all of these economies have in common? They are all developed markets that have a major global currency with central banks that have been engaged in extraordinarily easy monetary policy.

Now let’s head over to Asia. The Japanese stock market (EWJ) has also gained by +24% year-to-date. And even more than its European counterparts, it has a major global currency along with a central bank that has engaged in arguably the most aggressive monetary easing in modern history for a major developed economy with a program designed to double the yen money supply by the end of next year. The only other market of note is New Zealand, which although small is also a developed economy with its own currency and an independent central bank engaged in aggressive easing. Its stock market is up +14% year to date.

One you look past these major markets, a far gloomier picture suddenly emerges with three key reasons to at minimum question the strength and durability of the stock market rally across the developed world in 2013.

Commodities & Commodity Countries

Another defining characteristic for the markets listed above beyond being a developed economy with a well-established global currency and an independent central bank is that none is dependent on commodity production as a primary driver of growth.

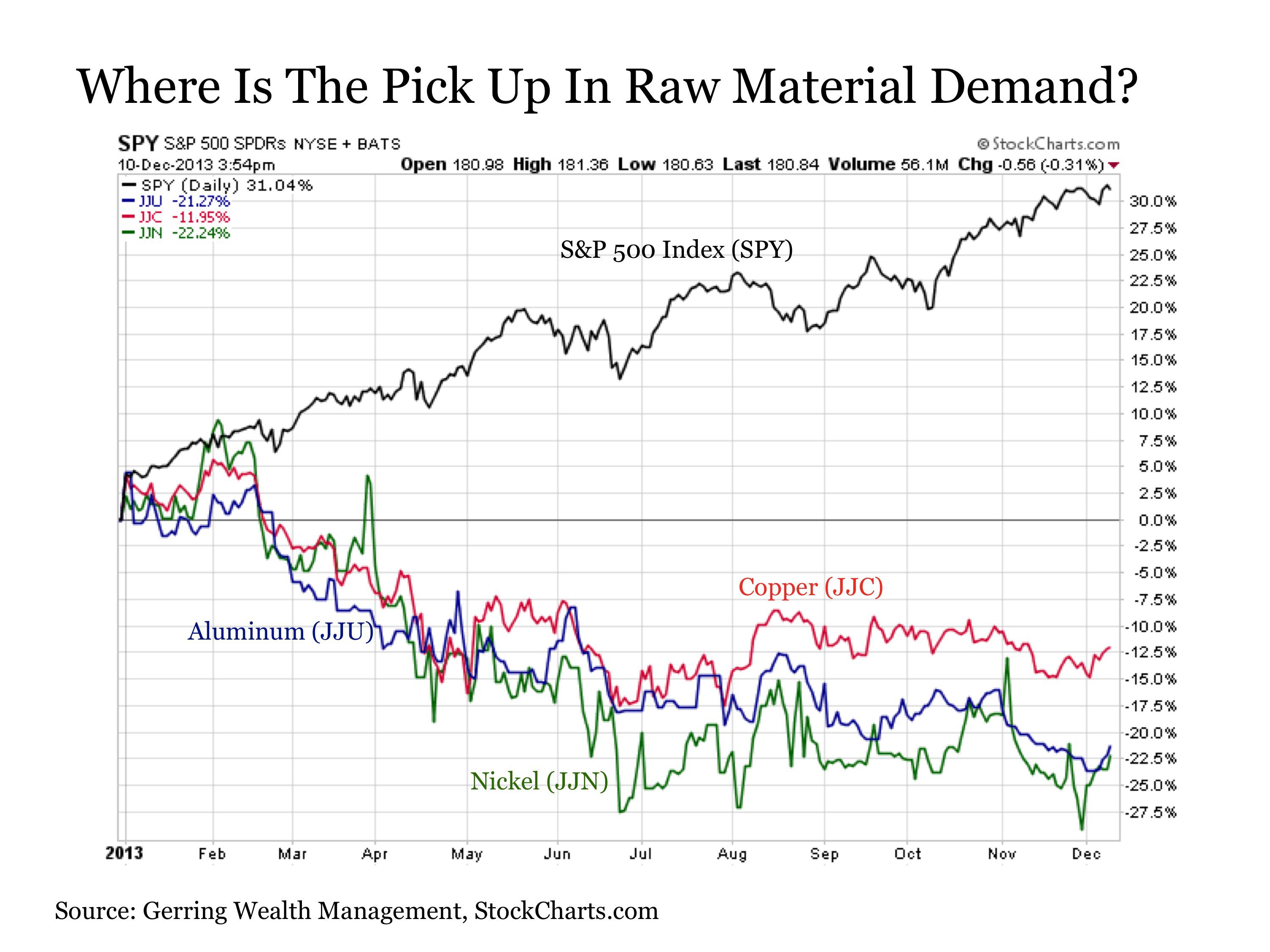

What of the commodities market in 2013 anyway? If we were indeed on the cusp of a major breakout in global economic growth, would we not see industrial commodity prices aggressively bid as companies compete to gather raw materials to ramp up production? Not only have price gains been absent across the metals complex in 2013, they have been hemorrhaging lower all year. For example, copper (JJC) is down -12%, Aluminum (JJU) is lower by -21% and Nickel (JJN) off by -22%. As for oil prices (OIL), they are mixed at best with Brent Crude incrementally down for the year while West Texas Intermediate is now up but was effectively flat year to date as recently as the end of November.

The fact that virtually no evidence exists in the commodities space supporting a global economic recovery is understandably serving as a headwind for those major developed economies that are reliant on commodities production. For example, Australian stocks (EWA) are incrementally lower for the year while Canadian stocks (EWC) are up less than +3% in 2013. And both of these markets have either flattened over the past month in the case of Canada or pulled back sharply in the case of Australia at a time when the U.S. stock market continued to rise. These are hardly signals confirming any quickening of global economic activity.

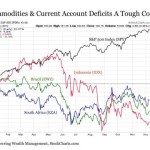

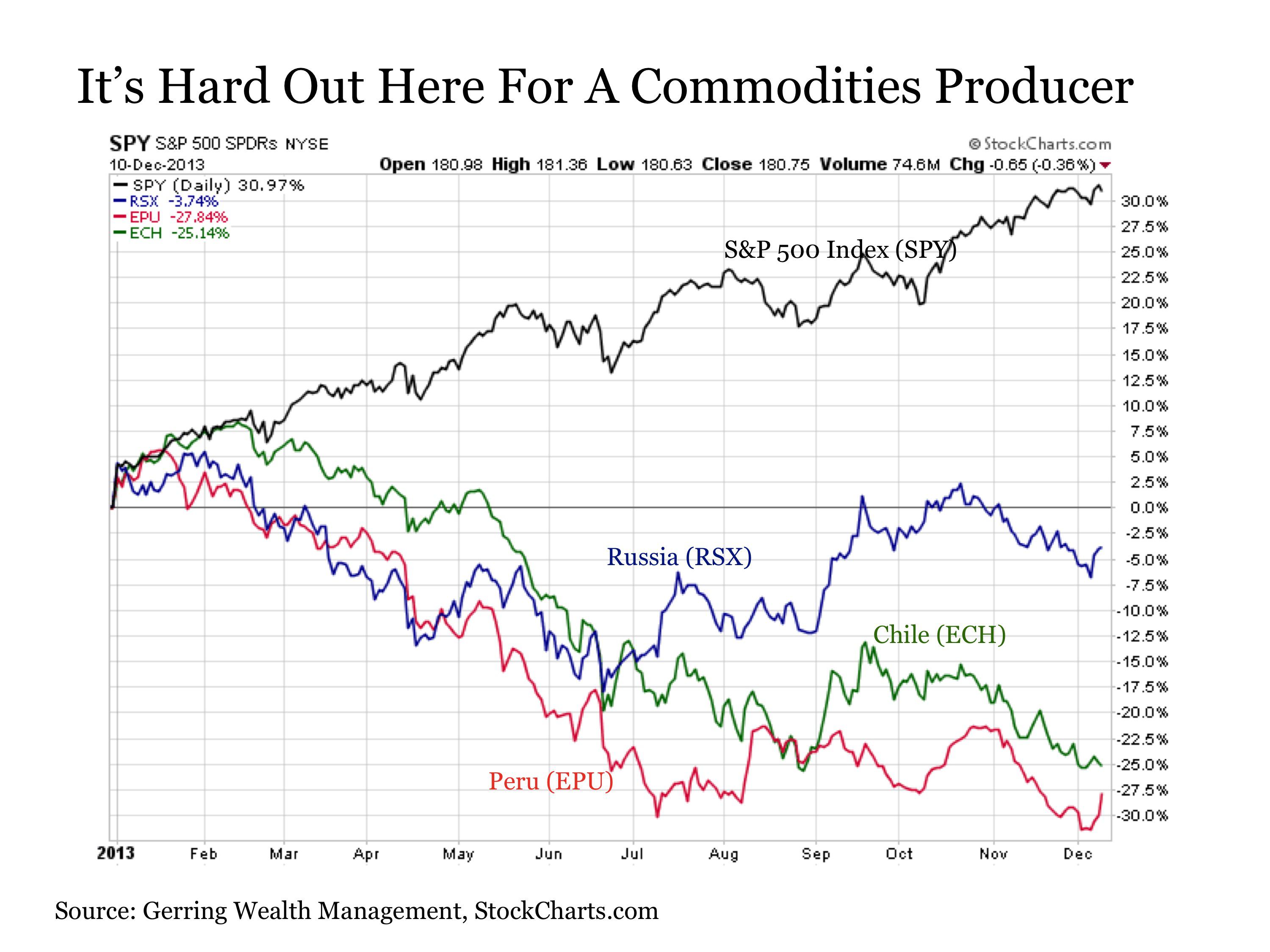

The wrath of declining commodities prices is being felt far more profoundly across emerging market countries that are dependent on commodity production and are already experiencing slowing growth. While the larger countries like Russia (RSX) have been holding up relatively better in recent months, its stock market is still down -4% for the year after being down by as much as -18% in June. And smaller commodity driven economies such as Chile (ECH) and Peru (EPU) are down -25% and -28%, respectively. These are just a few of the many developing economies without a major currency or central bank that are in this bind, with some dealing with compounding issues beyond simply being a commodities producer.

The Current Account Deficit Countries

While the Fed’s aggressively easy monetary stimulus has thus far been a boon for U.S. stocks, the same cannot be said for those economies suffering the spillover effects. This includes those many emerging economies that have been the recipients of massive liquidity flows by investors desperately seeking higher interest rates with yields in the developed world effectively pinned to the ground at zero. While this enabled rampant debt fueled spending activity in these markets at the expense of savings during much of the post crisis period, it appears the bill may be coming due (does this behavior of too much borrowing and not enough savings under artificially and unsustainably favorable circumstances sound at all PIIGSishly familiar?) now that the Federal Reserve appears prepared to finally begin standing down from its relentless stimulus program. This may have a destabilizing effect on the global economy as the money that once flooded in may soon be starting to rush back out at an accelerating rate.

A number of commodity producing economies are feeling the doubly negative effects of running sizeable current account deficits along with higher debt levels in an environment of slowing growth. These include Brazil (EWZ), Indonesia (IDX) and South Africa (EZA) that are lower for the year by -16%, -22% and -9%, respectively.

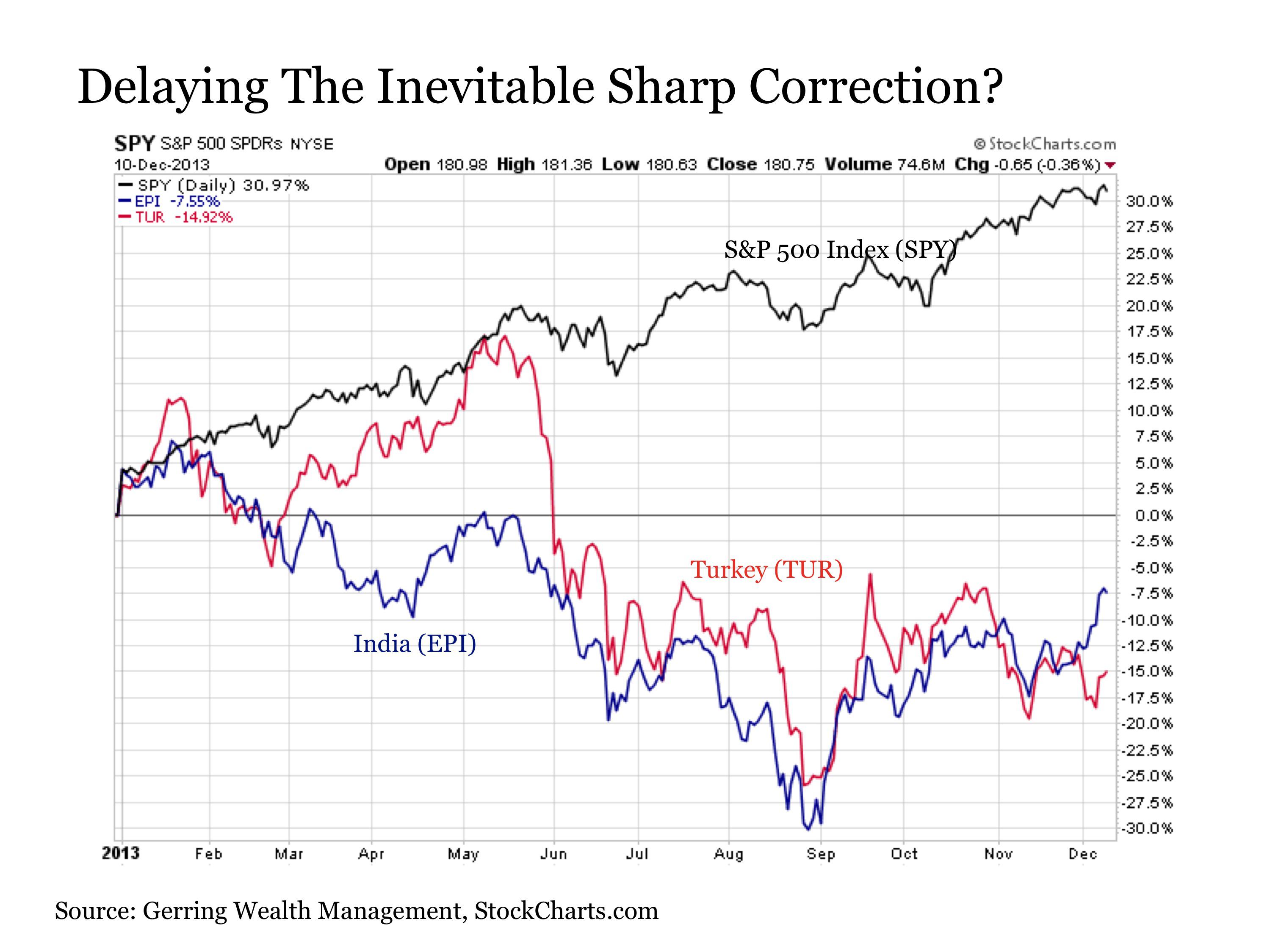

An economy does not need to be a commodities exporter to suffer at the hands of its current account deficit and the problems that have accompanied it in the current cycle. Both India (EPI) and Turkey (TUR) are still down -8% and -15%, respectively, year to date, and this follows sharp rebounds from their early September lows when both markets were off by nearly -30% for 2013. One gets the sense that these markets may be delaying the inevitable sharp correction once the Fed tapering match is finally struck.

But an economy does not even need to be commodity dependent or running a current account deficit with high debt levels to have hit the wall in 2013. And nowhere is this more evident than across Asia.

Asian Countries

While monetary stimulus from the Bank of Japan has the country’s stock market running wild in 2013, the same cannot be said for most other major markets across the region, as the iShares MSCI All Country Asia ex Japan Index (AAXJ) is up a mere +3% year to date.

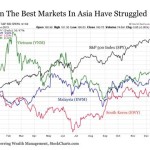

A select group of countries have markets that are performing well, but even these are more of a mixed story upon closer investigation. For example, Vietnam (VNM) is up a solid +13% year to date, but it had been up nearly +40% in early February of this year and has been trending lower ever since. South Korea (EWY) is up +2% for the year, but it had been down as much as -20% in 2013 as recently as late June. And although Malaysia (EWM) is higher by +10% year to date, it peaked in early May and had been lower for the year by as much as -5% only a few months ago in late August. And these are the better performing markets outside of Japan across the region.

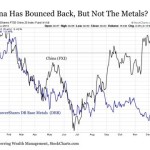

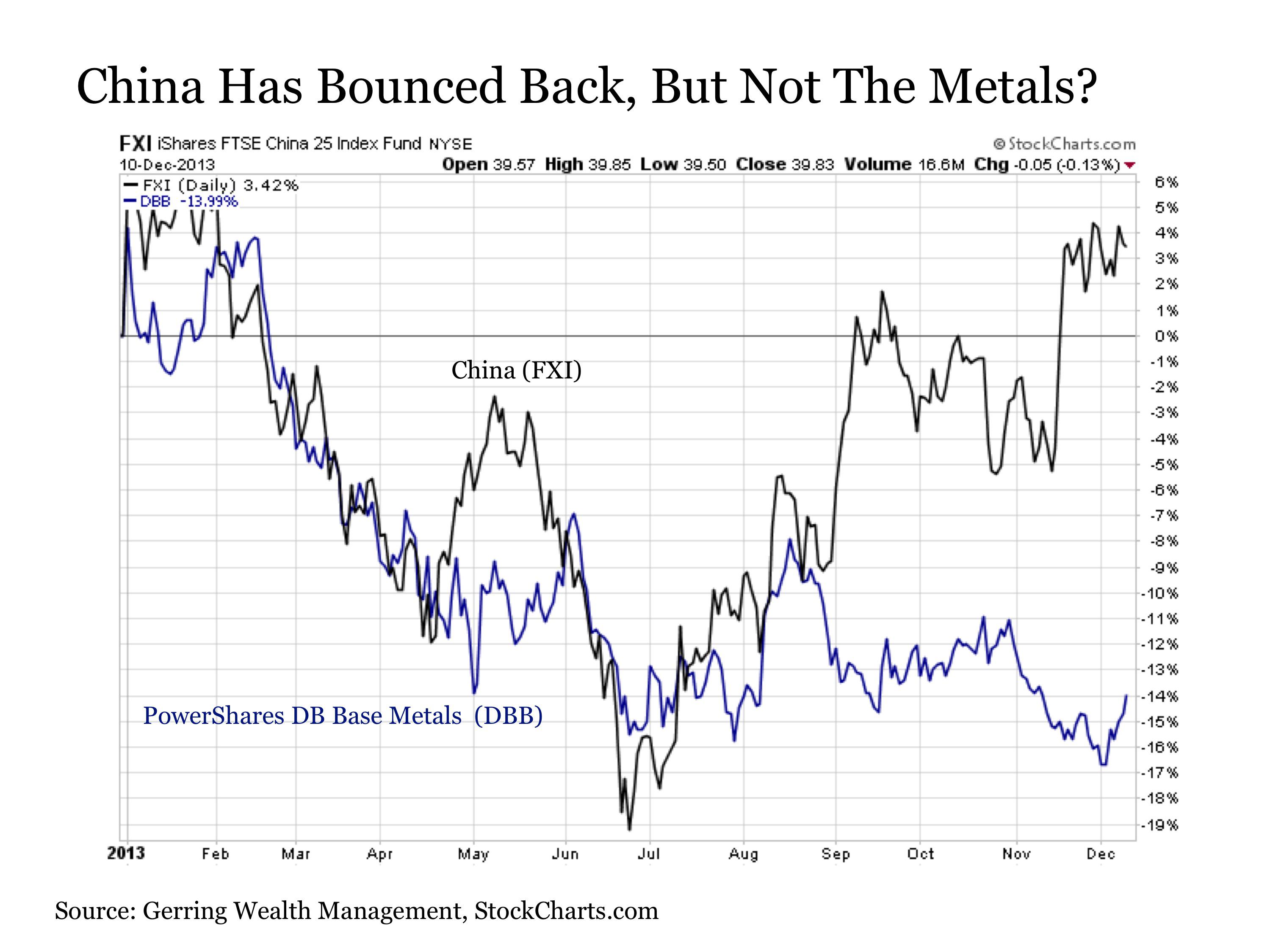

China is another market that has mounted a valiant comeback in 2013, but remains surrounded by major question marks. After being down by nearly -20% in June, China (FXI) is now higher by +3% year to date following a sharp rally over the last month. Closely neighboring and highly correlated markets in Hong Kong (EWH) and Taiwan (EWT) have generally been more consistent performers through the year and are now also up for the year in the high single-digit to low double-digit range after having been in negative territory as recently as late August. But with debt-to-GDP levels already at nosebleed levels in China along with slowing economic growth, persistent signs of speculative froth in market segments such as real estate and efforts at monetary tightening already underway, it stands to wonder how long this recent bounce can sustain itself. Perhaps more importantly, if the recent stock market rally from the largest exporter in the world in China was indicative of a pick up in global economic growth, it stands to wonder why we are not seeing any sort of comparable rebound in industrial metals (DBB) given the traditionally high correlation between the two. It should be noted that any deviations in the recent past have resulted in China catching back up to the downside, which does not bode well given developments since early September.

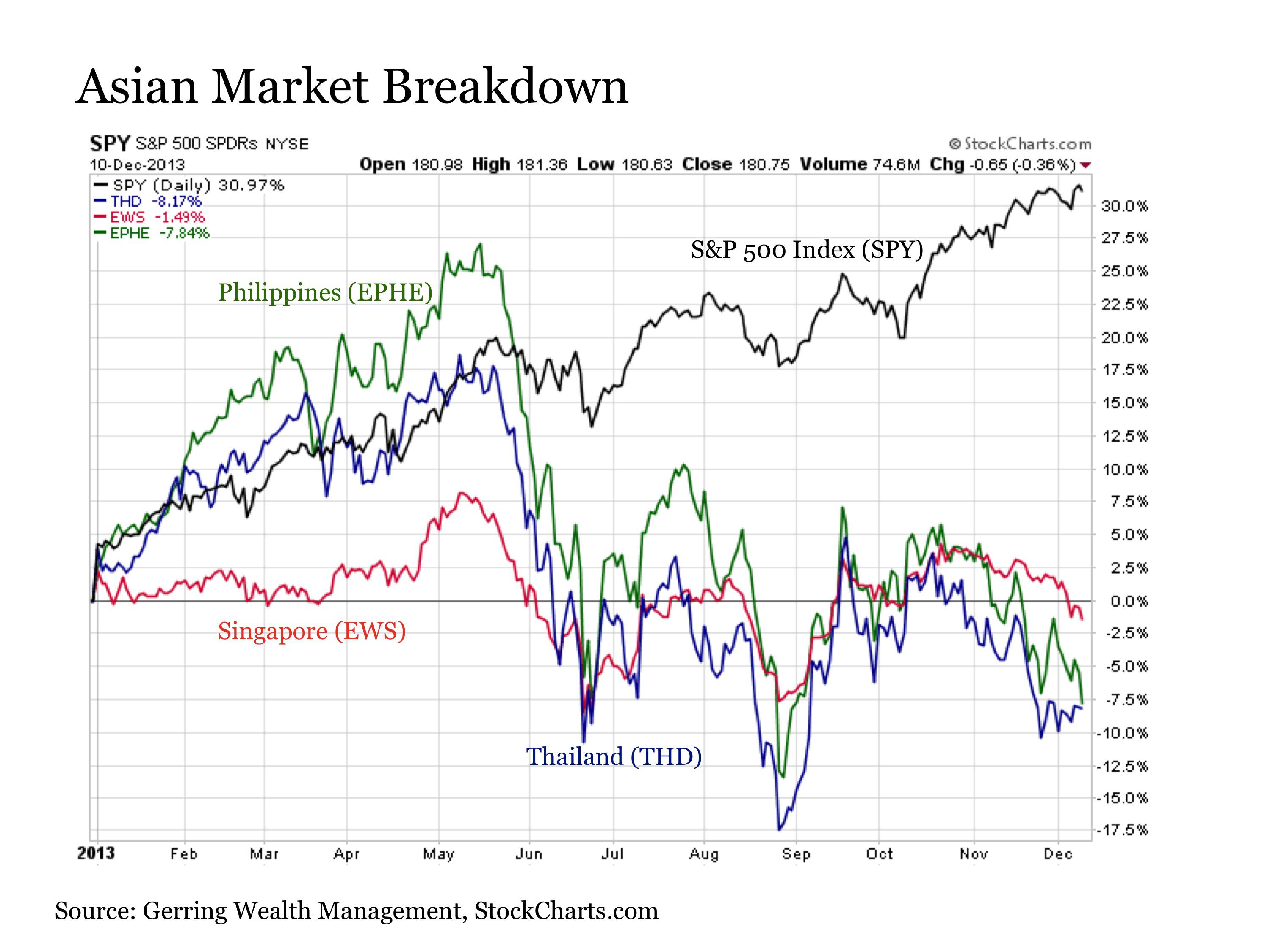

The generally poor performance of a number of other markets across the Asia region raises additional questions. While markets such as Thailand (THD), Singapore (EWS) and the Philippines (EPHE) were all up strongly to varying degrees with the U.S. stock market through mid May, all of these markets have since broken down hard in the months since. While Singapore is still clinging to an incremental gain year to date, both Thailand and the Philippines have both turned negative once again for the year, with all three markets trending lower since mid October.

The Bottom Line

The idea that the U.S. stock market along with its developed world brethren is surging in 2013 behind the momentum of an accelerating economic recovery simply does not add up. The fact that these select developed markets have deviated so far above other major asset classes outside of equities alone raises serious questions. But the fact that so many segments within the global stock market are showing similar deviations is even more notable, particularly when those trailing markets would likely be the ones leading right now if we were indeed on the cusp of the next sustained growth cycle.

Instead, when breaking stock market performance down by region and country, what is currently taking place suddenly becomes very clear. If you are a big economy with a major global currency and an aggressively easy central bank, you still have the ability to juice your stock markets artificially higher. But if you are any other economy around the world, you are increasingly stuck to deal with the unpleasant reality that growth simply is not accelerating the way global central bankers had hoped. And for some, they are even left to deal with the growing spillover consequences of the relentlessly easy policies of major central banks whose policies have yet to achieve sustainable economic growth after all of these years. Thus, the fact that the U.S. Federal Reserve is potentially considering scaling back on its asset purchase program as soon as next week is critical, as we remain far beyond any sense of reality at current prices in the U.S. stock market, not to mention the potential fallout effects abroad.

Surprisingly, the outlook for developed country stocks including the U.S. may be little better even if the Fed stays the course with further aggressive monetary stimulus. A dissection the returns of the S&P 500 Index from January to mid May versus the seven months that have followed to date reveals why. Since mid May, the U.S. stock market is up +9% on the S&P 500, which is certainly a solid performance. But viewing this performance in a different context, it has cost $65 billion in Fed asset purchases since mid May to generate a +1% return in the U.S. stock market. This is greater by more than half over the $41 billion in Fed asset purchases required to generate a +1% gain in U.S. stocks from January to mid May. In short, not only are fewer asset classes responding positively to central bank asset purchases, but the ability to achieve gains among those remaining few categories that are still responding is also becoming increasingly costly with the passage of time. In short, the positive impact on capital markets with each marginal dollar of monetary stimulus is fading.

The tunnel provided by global central bank monetary policy stimulus is becoming increasingly narrow. And those investors that remain tunnel visioned on the U.S. stock market only and choose to ignore the mounting problems already developing in many parts of the world may be doing so at their own peril. For we are already seeing the potential fallout effects begin to surface from persistently aggressive monetary policy after so many years, and the end result may be yet another wave of tumult for global financial markets before its all said and done.

So instead of trying to wring out the last drops of gains from a stock market rally that is extremely long in the tooth after nearly five uninterrupted years, perhaps investors may be better served to begin exploring opportunities in once developed markets like the U.S. finally begin to fall back to the reality that so many in the world have been living for some time.

Disclaimer: This post is for information purposes only. There are risks involved with investing including loss of principal. Gerring Wealth Management (GWM) makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made by GWM. There is no guarantee that the goals of the strategies discussed by GWM will be met.

Source:

The Peril Of Stock Market Tunnel Vision

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More…)

View post:

The Peril Of Stock Market Tunnel Vision [SPDR S&P 500 ETF Trust …

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}