Where's the Plane? | Active Investment Advisor

In another example of life duplicating the media, it seems like most people here and abroad have been consumed by watching a real life episode of Lost for the last week. The question of what happened to Malaysia Airlines Flight 370 has quickly soared to the opening spot on all of the network news shows, much as Lost and its Oceanic Airlines Flight 815 climbed quickly to the top of the ratings. At CNN it appears that the network of late can report on nothing else!

Of course, there are other stories. Like last year when we were all consumed by Cyprus and Italy, Spain and Portugal before that, this year we have the Ukraine, Russia and the Crimea mess to divert us, and a Chinese economic slowdown as Premier Li Keqiang seeks to have interest rates, demand and currency values become slightly more market driven. But last year and the year before we were up 10%-plus year to date at this point, while this year the market indexes hover around breakeven for the year and last week saw a better than 2% fall in the Dow.

All of us feel for the crew and passengers of Flight 370. I don’t know how their friends and family can cope with the “not knowing.” And it is that “not knowing” that provides the allure of the current story of Flight 370. It is a mystery. Like in Lost, no one really knows what happened. Heck, TV viewers and the show’s producers are still arguing over whether everyone was dead or not.

However, just as what follows a big up or down day on Wall Street, this present day story has plenty of experts telling us what really happened. Kind of like the blogs and TV critics did with Lost. Yet as we discussed last week, these experts do not have a good record of predicting anything where uncertainty is present.

Our approach is different, both in this column and in our management. When talking about the market or making Buy and Sell decisions, we like to focus on the things we know to tell us what is likely to happen in the immediate future. We look to the past for similar instances and extrapolate into the future. These are all quantifiable events – economic happenings whose effects are measurable allowing us to assign probabilities for future occurrences.

Right now we know that interest rates are at a record low level. In this country, with its economy and its stock market, this is an incredibly dominant theme of which many refuse to recognize the significance. Even when interest rates start moving up from these levels, we will be at relatively low interest rates – still among the lowest in our lifetimes. This may continue to be a positive underlying support for the market for a long time, but with rates still down from last year at this time it remains a positive in the short term, as well.

Secondly, we just completed an earnings reporting season. The reports were for the most part great. Not only did the earnings rate hit a record high, but the percentage of reports beating expectations was the highest in years. Stock prices generally reflect earnings. It’s no coincidence that both are at record highs.

Of course, the markets have to value those earnings and how they value – at what multiple – can also send stocks higher or lower. This multiple, called the price earnings ratio – the price of a stock divided by its earnings per share – has been the source of a great deal of discussion over the last few years.

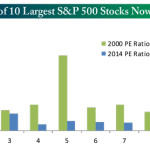

I have to admit that I was concerned when the P/E ratio refused to drop to single digits at the market low, as it had in most other declines. And now that the P/E of the S&P 500 is up to 19.7 on a trailing earnings basis, many experts are saying that we are getting overvalued and in “bubble” territory.

Yet a look at the P/Es of the top ten companies of the S&P today versus their level at the top of the last “bubble” suggests that we have a long way to go before we hit true “bubble” territory. In other words, as our friends at Bespoke Investment Group put it:

The chart below shows the current valuations of the ten largest S&P 500 companies and compares them to the valuations of the ten largest S&P 500 companies in 2000. Using this scale, the valuations of the ten most highly valued companies stand well in the shadows of where the ten largest companies in S&P 500 were valued back in 2000. Yes, there may be certain areas of the market that are showing bubble characteristics. The key difference between now and 2000, though, is that the stocks that are in bubbles right now are not large enough to drag down the entire market along with them. A large decline in fuel-cell, marijuana, or even social media stocks is unlikely to be a major market moving event.

Source: Bespoke Investment Group

In addition, the general economy is improving, with eight of twelve economic reports coming in better than expected last week. And with weather likely to be less of a plot device in the months ahead, we should see continued improvement.

Finally, both seasonality and market sentiment support higher prices. The next two weeks are generally positive in the market. The “Saint Patrick’s Day effect” I call it, as the market leprechauns generally send shares higher over that period each year. In fact, the next two weeks have been positive seven straight years and eight of the last ten. Also, this week is an option expiration week and that is normally bullish.

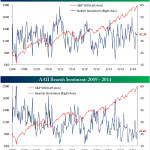

Sentiment-wise stock market investors, as evidenced by the bullish sentiment measured by the American Association of Individual Investors AAII Sentiment Index, are not living in “bubble” territory either. The bullish sentiment index is kind of stuck in the middle of the road and even the bear market sentiment, which has been very low and concerning, has ticked upward. Not the kind of environment where market tops are likely to have been formed.

Source: Bespoke Investment Group

Although all of these indicators seem positive, we’re talking about the financial markets here. And anything is possible short term. Focus could shift back to China or the Crimea on any day. Or some other black cloud, like the smoke monster in Lost, could suddenly appear. That’s why we argue for dynamically risk-managed strategies combined in strategically diversified portfolios. It allows us to employ systems to spot and adjust to the unexpected.

Speaking of the unexpected, and being an optimist, I can only hope, just as the late Hervé Villechaize, playing Tattoo, used to say on Fantasy Island , that the next thing we will hear on Flight 370 is someone spotting and shouting “Da Plane! Da Plane!” After all, life often does seem to duplicate the media.

All the best,

Jerry

Excerpt from:

Where's the Plane? | Active Investment Advisor