Burgeoning Global Capital Flows Mean Traditional Stock Market …

Summary

Global capital flows are growing.

So much so that the net of these flows are often greater than a country’s international trade balance.

The implications of these growing capital flows for investors are discussed in the article.

©Elliott R. Morss, Ph.D. All Rights Reserved

Introduction

The law of supply and demand ultimately determines the prices of goods/services. And this holds for stock markets “prices” and currencies. Foreign demand for both US equities and dollars continues to grow. This growing demand has implications for commonly used stock market pricing norms and dollar values.

a. Stock Market Prices

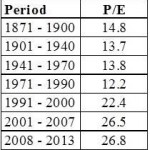

The long-term norm for stock market prices has been the price-to-earnings ratio (P/E). Table 1 indicates what has happened to the Standard and Poor’s 500 P/E over time. For most of its history, the P/E has been in the 12-15 range. That all changed in the 1990s. Why have P/E ratios increased and remained high? As will be shown below, a good part of the explanation has to do with increased foreign demand for US equities.

Table 1. – Standard and Poor’s 500 P/E

Source: http://www.multpl.com/table

b. Value of the US Dollar

Traditionally, a country’s trade balance (the difference between goods and services exports and imports) has been a pretty good indicator of whether its currency is increasing or decreasing in value. One would think that with the huge trade deficits the US has run since the ’70s, the dollar would have lost a lot of value, and it has. Since 1998, when the euro was established, the dollar has lost 12% against the euro and 21% against the yen. But more recently, the dollar has held most of its value against these two currencies, even though the US continues to run large deficits. How could this happen? As will be shown below, a good part of the answer has to do with other dollar demands.

Importance of Global Capital Flows

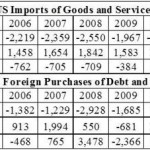

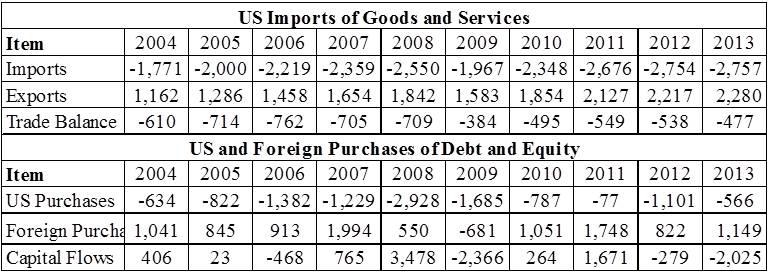

Capital flows consist primarily of equity and debt purchases by Americans and foreigners. Foreigners’ purchases can be likened to US exports of goods and services in that they require dollars and hence increase dollar demand. US purchases of foreign securities are just the opposite. And US imports of goods and services, they require foreign currencies and thereby reduce dollar demands. Table 2 indicates just how important capital flows have become relative to US international goods and services trade. Note that in 2008, 2009, 2011, and 2013, net capital flows were much greater than the trade balances for the same year. The growing importance of capital flows relative to trade mean dollar values will increasingly depend on capital “imports” and “exports”.

Table 2. – “US Trade” Versus Capital Flows (bil. US$)

Sources: Trade – US Bureau of Economic Analysis, Capital Flows – US Treasury.

International Equity and Debt Flows: Analysis

Foreign holdings of US equities and debt have become important. The Federation of World Exchanges estimates the capitalization of the NYSE and Nasdaq to be $18 and $6 trillion, respectively. The US Treasury estimates foreign equity holdings at $5 trillion, or 21% of the total. A recent Congressional Research study found that foreigners own 47.1% of US Federal publicly held debt.

When do foreigners buy US securities? And when do Americans buy foreign equities and debt?

a. Equities

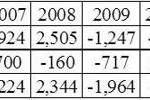

Table 3 includes data on US and foreign purchases and sales of equities. Figures are negative when transactions result in dollars leaving the US, e.g., US purchases of foreign equities or foreign sales of US equities.

From Table 3, it is apparent that in most years, Americans have been buying foreign equities and foreigners are buying US equities. For the total period, the transactions totals have been amazingly close, with US net purchases only $2 billion higher than foreign purchases of US equities.

Table 3. – US and Foreign International Equity Transactions, 2004-2013 (US$ bil.)

Source: US Treasury

It is also interesting to look at buying and selling patterns over the entire period. Americans have been steadily accumulating foreign equities over the period, with the exception of 2008 (US banking collapse) and 2011 (eurozone problem). Foreigners bought US equities throughout the period, except for 2008 and 2009. Heavy foreign equity purchases in 2011 could have been a swap of euro equities for US equities.

b. Debt

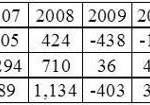

Table 4 includes data on US and foreign purchases and sales of debt. Figures are negative when transactions result in dollars leaving the US, e.g., US purchases of foreign debt or foreign sales of US debt. As can be seen, foreigners have purchased a net $5.9 trillion of US debt (mostly US Treasuries) over the last decade. With the exception of the panic year (2008), Americans have steadily accumulated foreign debt.

Table 4. – US and Foreign International Debt Transactions, 2004-2013 (US$ bil.)

Source: US Treasury

Implications for Investors

In the above, we have documented the growing importance of capital flows and their impact on equity, debt and currency markets. In what follows, we speculate on how capital will flow in coming years and the significance of these movements for investors.

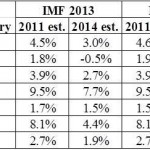

Consider first what global equity investors are thinking. Table 5 provides 2014 GDP growth estimates for regions and countries made by the IMF both in 2011 and today. It is notable that in this group of regions and countries, only the US has exceeded the 2011 growth estimate. The significance of this for global investors? Invest in the US.

Table 5. – 2014 GDP Growth Estimates Made in 2011 and 2014

Source: IMF

Consider next debt investments. With the Federal Reserve keeping interest rates effectively at 0%, many fixed income investors went overseas in search of debt yield. With the Fed’s Treasury purchases winding down, US interest rates will start to rise, and that will bring a lot of fixed income investors back to the US.

The growing demand for US fixed income investors will strengthen the dollar. The dollar will also be strengthened as the US trade deficit falls due to continuing reductions in “energy product” imports (with growing oil and natural gas production in the US, energy imports have already fallen by $79 billion between 2011 and 2013).

In short, US P/Es are not too high. Right now, US equities are the best option for global investors. And fixed income investors will return to the US once US interest rates rise.

Of course, this will not last. Emerging market growth rates have moderated a bit, but the demand for goods and services from their growing middle classes of Latin America and Asia continues to be a significant stimulus for global growth. And once the “weak sister” countries in the eurozone return to their own currencies, growth will resume there as well.

ETFs are a great way to take advantage of changing global conditions. For example, for the countries and regions discussed above, the following list of ETFs is worth tracking:

Vanguard Total World Stock Index ETF (NYSEARCA:VT)

iShares S&P India Nifty Fifty Index (NASDAQ:INDY)

Guggenheim China All-Cap ETF (NYSEARCA:YAO)

iShares S&P Latin America 40 Index Fund (NYSEARCA:ILF)

SPDR EURO STOXX 50 ETF (NYSEARCA:FEZ), and

ProShares Ultra MSCI Japan ETF (NYSEARCA:EZJ).

Source:

Burgeoning Global Capital Flows Mean Traditional Stock Market And Currency Norms No Longer Apply

Disclosure: The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it. The author has no business relationship with any company whose stock is mentioned in this article. (More…)

Original source:

Burgeoning Global Capital Flows Mean Traditional Stock Market …

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}