Political Calculations: Is Technical Analysis Completely Worthless?

The general consensus among most people who seriously study markets is that technical analysis is mostly garbage.

After all, how can a investing method that completely disregards a company’s fundamental business prospects in favor of tracking its stock price over time possibly ever get anything right except by chance?

In fact, the most wide-ranging study conducted to date of technical analysis as a trading strategy found that it wasn’t consistently profitable in any of the stock exchanges of 49 countries. Furthermore, of the 5,806 technical analysis trading rules they tested, none provided any “value beyond what may be expected by chance”.

So why would investors waste any time on it at all?

One insight to that question was provided by Morris Armstrong, who used technical analysis while working as a currency trader:

I used technical analysis quite alot when I was a currency trader and I think that it adds a lot of value in the establishment of entry and exit points when contemplating a position. It will also allow you to get a very good idea on when a trend is getting tired or is picking up steam again.

I am not sure if people think that it is a tool for investment strategy but it certainly is a good tool for trading.

Besides, in trading there is the old axiom “I’d rather be lucky than good”

Well, there is always that to stake your livelihood upon, isn’t there?

The reason we’re bringing this up today is because our recent discussion of the actual mechanism that might lead stock prices to “revert to the mean” as stock prices follow a trend provides an ideal opportunity to see if technical analysis might be anything other than worthless.

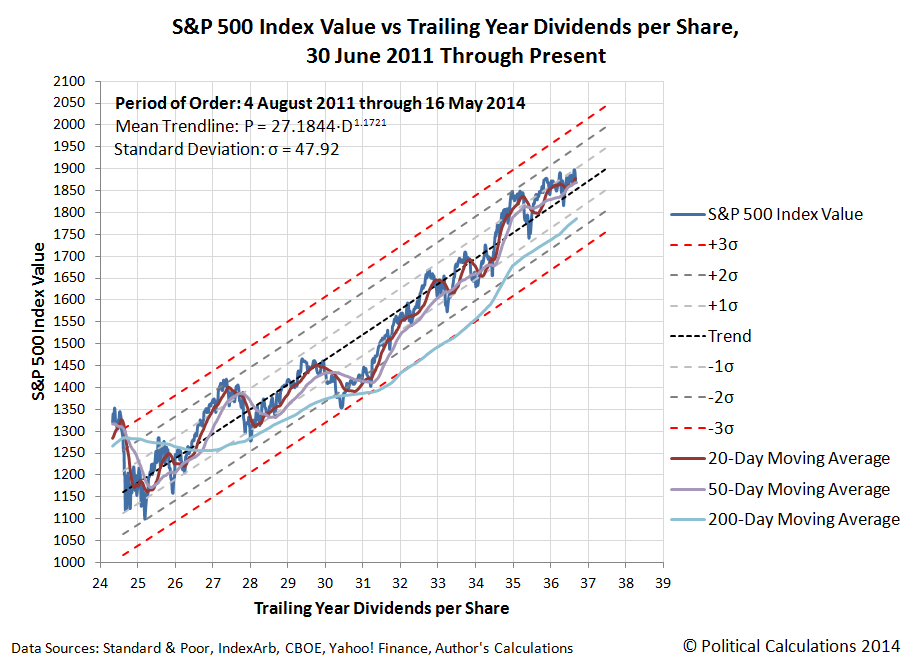

Specifically, the idea of whether the moving averages used by technical traders can give us any legitimate insights. We’ll do that by overlaying the 20-day, 50-day and 200-day moving averages over our power law statistical equilibrium chart to see how well any of these components might coincide with elements of our analysis that have statistical meaning. The chart below shows the results of that exercise:

We selected this period because it coincides with a relative period of order in the U.S. stock market extending through the present day, where the variance of stock prices might be reasonably approximated with a normal distribution. As such, if technical analysis is going to provide any sort of meaningful insight, it should work in this environment.

But before going further however, we should note that stock prices do not closely adhere to a normal distribution – the best that can be said of them is that they do follow a central tendency, but that the variance of their distribution about this central tendency is not normal. This assumption however lets us apply the tools that have been developed for statistical analysis, which provides useful insights in our regular analysis.

Let’s focus on the 200-day moving average to see what its interaction with stock prices and the various statistical indications shown on our chart can tell us about the value of using this technical indicator to choose entry and exit points for investments. Specifically we’ll focus on whether seeing stock prices drop below the 200 day moving average is sending a buy or sell signal, defining where an investor should enter or exit the market.

Here, the most evident thing that stands out to us in the chart above is the relative position of the 200-day moving average with respect to the lower equilibrium limit of our chart when trailing year dividends were between $31 and $34 per share, which occurred between mid-December 2012 and mid-August 2013.

Since the 200-day moving average is often considered to be a “support level” for stock prices, its overlapping of this lower limit of the statistics-based range in which we would expect stocks to fall actually has real meaning. If stock prices drop below this range, that would be an indication that order is breaking down in the stock market, which would be a very clear indication to sell if history is any guide.

Unfortunately, that nine-month period was the only time in the last two and three-quarter years where the insight provided by technical analysis might have been useful. Otherwise, we see that the 200-day moving average has spent much of its time at a level about one and half standard deviations below the mean trend trajectory for stock prices. At this relative position, if stock prices were to drop below this level, it would really be an indication to buy, where an investor would benefit whenever stock prices might revert back to the mean.

These opposing scenarios reveal why technical analysis fails. Unless you know where the 200-day moving average is with respect to the range into which stock prices will most likely fall, whether following an upward or a downward trend, there’s no guarantee that an investor relying upon technical analysis will make the correct investment decision given the same technical signal.

It really is like flipping a coin, since success is random. And really, random at best – most investors who use technical analysis “frequently make poor portfolio decisions“.

In conclusion, we consider technical analysis to be, at best and under very limited circumstances, a very, very weak form of statistical analysis. At worst, more effective and less time consuming ways of making sound investment decisions would involve flipping coins or reading tea leaves.

References

Marshall, Ben R. and Cahan, Rochester H. and Cahan, Jared, Technical Analysis Around the World (August 1, 2010). Available at SSRN or dx.doi.org/10.2139/ssrn.1181367. Ungated version available [PDF Document].

Read more:

Political Calculations: Is Technical Analysis Completely Worthless?

See which stocks are being affected by Social Media

{kind=link}