The Dollar Carry Trade's Impact On Global Equities Is Increasing …

I would say there is no pleasing some people, but that statement is incomplete; a better assessment is that there is no pleasing people in general and people eager to shift responsibility in particular. Take the nonstop complaining by receivers of the dollar carry trade after the launch of QE in March 2009. Political leaders — a class well-versed in sloughing off responsibility for the bad while taking credit for the good — in places ranging from Brazil to India felt their domestic economies and price levels were being distorted by the flow of low-yielding dollars into higher-yielding reais and rupees.

Now the worm turns, as the worm often does. As an aside, have you ever wondered why you see earthworms stranded helplessly on the sidewalk after a heavy rainstorm? The annelid worms have about 518 million years of evolutionary history but still have not been able to come up with a plan for what to do when it rains. That they have survived this long puts that whole “be prepared” thing into question.

Equity Market Exposure

Carry trades, the borrowing of a low-yielding currency such as the dollar to lend into higher-yielding currencies, can be broken into two components: the net interest rate return and the spot currency return. As only 10 of the 28 currencies examined have had positive total carry returns since taper talk began in May 2013, and as only six currencies have had lower average daily interest rate returns than the dollar over that period, it stands to reason that the greenback has gained on a spot rate basis against the remaining eighteen currencies.

We have seen the effects of these negative carry returns on short-term interest rate instruments such as the iShares Emerging Markets Local Currency Bond ETF (NYSEARCA:LEMB) or the Templeton Emerging Markets Income Fund (NYSE:TEI); they have lost 8.29% and 13.33%, respectively, since May 22, 2013. Their positive interest rate spreads were unable to offset the negative spot rate changes; any level of interest rates high enough to offset one-day currency drops such as last Thursday’s 12.39% drop in the official rate for the Argentine peso or the Ukrainian hryvnia’s 2.37% year-to-date decline would devastate the local economy. Oh, and if you are not happy that our currency is more pronounceable than Ukraine’s, I am.

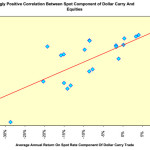

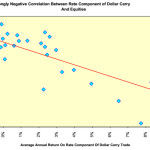

Now let’s map the annualized returns in USD terms for a set of national equity markets as a function of their annual interest rate return against the USD since last May. The function is very strongly negative with a beta of -6.20. The higher a country’s interest rate spread to the US over this period, the lower its equity market return to the USD-domiciled investor.

Now we can repeat the exercise for the annualized spot rate change. Here the beta is a strongly positive 1.86; the stronger a country’s currency is relative to the dollar, the higher its USD-denominated returns are.

What is so striking about these relationships’ increasing strength and clarity since May 2013 is how little the US has had to do to induce dollar strength. Taper talk in May was followed by a month of “we didn’t mean it” speeches by Federal Reserve officials, a postponed taper in September, and a small taper in December.

If all of this has unfolded in mere anticipation of QE’s eventual end in the US – we have yet to talk about higher short-term interest rates – then actual action could make international investing for the American investor an exciting proposition for the next few years.

Continued –

The Dollar Carry Trade's Impact On Global Equities Is Increasing …

See which stocks are being affected by Social Media