Why Stock Market Bulls Should Hope Interest Rates Don't Rise …

Yesterday, I participated in a panel discussion on CNBC about the markets and the economy. It was during the course of that discussion that one of the participants uttered the most important phrase:

“Everbody knows interest rates are going to rise.”

First, let me explain my reasoning for why it is possible that “everybody” is wrong. As I addressed last week in “Interest Rate Predictions Meet Rule #9” when everyone is expecting something to happen, it is often the opposite that occurs.

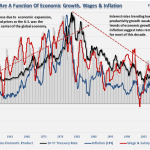

“As you can see there is a very high correlation, not surprisingly, between these three components (inflation, economic and wage growth) and the level of interest rates. Interest rates are not just a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically the demand for capital rises as businesses expand production to meet rising demand. Increased production leads to higher wages which in turn fosters more aggregate demand. As consumption increases, so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs.

However, in the current economic environment this is not the case. The need for capital remains low, outside of what is needed to absorb incremental demand increases caused by population growth, as demand remains weak. While employment has increased since the recessionary lows much of that increase has been the absorption of increased population levels. Many of those jobs remain centered in lower wage paying and temporary jobs which does not foster higher levels of consumption.”

Whether you agree with this premise, or not, is largely irrelevant to this discussion. The current “bullish” mantra is the “great bond bull market is dead, long live the stock market bull.” However, is that really the case?

When the bond bubble ends this means that bonds will begin to decline, potentially rapidly, in price driving interest rates higher. This is the worst thing that could possible happen.

1) The Federal Reserve has been buying bonds for the last 4 years in an attempt to push interest lowers to support the economy. The recovery in economic growth is still dependent on massive levels of domestic and global interventions. Sharply rising rates will immediately curtail that growth as rising borrowing costs slows consumption.

2) The Federal Reserve currently runs the world’s largest hedge fund with over $4 Trillion in assets. Long Term Capital Mgmt. which managed only $100 billion at the time, nearly brought the economy to its knees when rising interest rates caused it to collapse. The Fed is 40x the size and growing.

3) Rising interest rates will immediately kill the housing market taking that small contribution to the economy away. People buy payments, not houses, and rising rates mean higher payments. (Read “Economists Stunned By Housing Fade” for more discussion)

4) An increase in interest rates means higher borrowing costs which leads to lower profit margins for corporations. This will negatively impact corporate earnings and the financial markets.

5) One of the main arguments of stock bulls over the last 5 years has been the stocks are cheap based on low interest rates. When rates rise the market becomes overvalued very quickly.

6) The massive derivatives market will be negatively impacted leading to another potential credit crisis as interest rate spread derivatives go bust.

7) As rates increase so does the variable rate interest payments on credit cards. With the consumer being impacted by stagnant wages and increased taxes, higher credit payments will lead to a rapid contraction in income and rising defaults.

8) Rising defaults on debt service will negatively impact banks which are still not adequately capitalized and still burdened by large levels of bad debts.

9) Many corporate share buyback plans and dividend issuances have been done through the use of cheap debt, which has led to increases corporate balance sheet leverage. This will end.

10) Corporate capital expenditures are dependent on borrowing costs. Higher borrowing costs leads to lower capex.

11) Commodities, which are very sensitive to the direction and strength of the global economy, will plunge in price as recession sets in.

12) The deficit/GDP ratio will begin to soar as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

I could go on, but you get the idea.

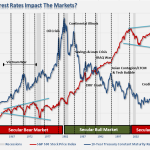

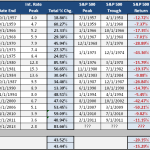

However, for those of you who still doubt that rising rates are bad for stock market returns, let me put into graphical form for you.

The chart and table below show what happens to the financial markets, and the economy, when interest rates increase.

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds. However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices has very little to do with the average American and their participation in the domestic economy. Interest rates, however, are an entirely different matter.

What would be required to diminish the impact of bursting bond market bubble is a slow, and controlled, unwinding of the bond market over an extremely long period of time. The Fed would have to step up interventions on a massive scale to offset the selling of the bond market to curtail the rise in rates. Even with that, I would expect a rather sharp economic deceleration as the housing market grinds to halt and overall consumption declines. The actual achievement of such a counter balance to a market as large as the bond market is difficult to fathom.

However, while bond prices are near historic highs, with interest rates near lows, it would certainly seem as if bonds are in a bubble. However, if interest rates are a reflection of economic growth, inflation and wages, as the first chart above suggests, then rates are likely “fairly valued.”

As I discussed yesterday, there is an ongoing belief that the current financial market trends will continue to head only higher. This is a dangerous concept that is only seen near the peak of cyclical bull market cycles.

“We saw much of the same analysis as Brad’s at the peak of the markets in 1999 and 2007. New valuation metrics, IPO’s of negligible companies, valuation dismissals as “this time was different,” and a building exuberance were all common themes. Unfortunately, the outcomes were always the same. It is likely that this time is “not different” and while it may seem for a while that Brad analysis is correct, it is ‘only like this, until it is like that.'”

The point here is that while the current trends can last longer than reasonably believed, which is why we currently remain invested in the markets, it is inevitable that things will change. The problem for most is that by they time they recognize that the underlying dynamics have changed it will be too late to be proactive, only reactive. This is where the real damage occurs as emotional behaviors dominate logical processes.

Original article:

Why Stock Market Bulls Should Hope Interest Rates Don't Rise …

See which stocks are being affected by Social Media