Spot The Odd One Out

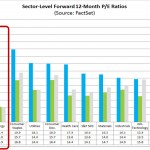

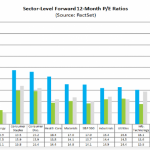

We hate to spoil the surprise, but the answer, as clearly shown by the first blue bar on the chart below, is Energy, and specifically the ridiculous valuation that energy companies are currently trading at. Why? Because as the following Factset chart shows, the forward P/E of the energy sector is currently 27x – an all time high – and which is more than double the historical multiple of this sector.

It also means that even though earlier today we were amused by the ridiculous valuation of the profitless biotech sector, perhaps it is time to mock the various energy names just as vociferously.

So how does one explain this lunacy? Simple: the BTFDers who are by now largely all-in the energy space, are hoping other BTFDers will come and lift oil, despite our repeated warnings that the price of oil is very more likely to plunge in June not only as a result of the US running out of storage capacity but, perhaps far more importantly as we first reported yesterday, North Dakota is likely to see a “big surge” in production this June, potentially besting another supply record even if prices continue to crater, according to Lynn Helms, director of the state’s Department of Mineral Resources, as a result of a tax loophole that will be triggered in June.

Then again, in a market in which central banks are willing and able to buy CL and Brent futures, nothing would surprise us anymore, and it possible that oil will surge right back to $88 and above, the only price at which the current valuation of energy companies makes sense. If it doesn’t, and the closer we get to the end of 2015 the more unrealistic this assumption becomes, energy stocks are looking at an air pocket that will wipe out some 50% of their value in the near future as we explained almost two months ago in “Either Oil Soars Back To $88, Or Energy Stocks Have To Tumble By Over 40%.”

Indicatively, back then the forward energy P/E multiple was “only” 22.4x. Now it is 27x and rising with every passing day!

So for those who missed our analysis back then, here it is again. The only thing that has changed is how much energy equities would have to drop unless oil surges. The answer: more.

* * * * *

From January 29, 2015

Several days ago we showed something remarkable: “current forward 12-month P/E ratio for the Energy sector is now well above the three most recent historical averages: 5-year (12.0), 10-year (11.9), and 15-year (13.6). In fact, this week marked the first time the forward 12-month P/E for the Energy sector has been equal to (or above) 22.4 since April 8, 2002. On that date, the closing price of the Energy sector was 225.15 and the forward 12-month EPS estimate was $10.05.”

Further refining this analysis and using the S&P Energy Sector Index data, the sector’s forward multiple is now an absolutely ridiculous, mindblowing 23x, the highest since 2002, having soared by nearly 100% in just the past few months as a result of collapsing energy sector earnings.

How is this possible?

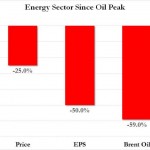

Simple: as the chart below shows, since the oil’s peak in June 2014, Energy company EPS have crashed by 50%, as a result of a 60% plunge in the price of oil. What about Energy Index prices? Well, they have fallen to be sure, but nowhere near far enough to where they should, down “only” 20% from the highs.

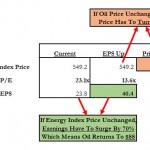

So what does this mean? Simple: either the long-term PE multiple is now null and void, and the “New Normal” forward PE of 20X+ is realistic, which of course is ridiculous, or there are two alternatives:

Energy sector earnings have to surge by 70%, implying a near doubling of oil prices to $88, for the forward P/E multiple to return to normal, or

The Energy sector price has to crash from 549 today to 323, where it would trade down to its historic forward P/E multiple, suggesting a price drop of over 40%!

This is shown visually on the table below:

So which is it? Well, as the following chart showing a relationship we have grown to love over the past few months, the main reason why energy stocks are loathe to catch down to reality is the same BTFD mentality which is keeping the S&P elevated well over 100% above its fair “ex-central banker” value. Indeed, every single time even the smallest buying momentum arrives, energy stocks soar as if stung, only to recrash day after precisely to where credit says they should be trading.

Which means that once the ongoing euphoria of a 5 year Pavlovian BTFD reaction wears off, the pain for those long energy equities (and credit, since the above analysis implies energy credits are also massively mispriced) will be unprecedented, unless of course, by some miracle, oil does indeed double from here and on very short notice.

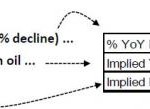

But wait, it gets worse, because while equities are pricing in an unsustainable 23x in foward energy P/E, another market, that of interest rate forwards, is implying oil plunging down to $35! As a reminder, oil is among other things, a function of rate differentials or said simpler, USD strength, strength which appears is not going anywhere. And as the following calculation from Cornerstone implies, should the EURUSD tumble to parity which is what Draghi’s desire seems to be, it would suggest a 22% plunge in oil from here, implying a $35.5 price of oil one year from now.

This in turn would mean that, all else equal, the forward PE multiple would rise to just shy of 30x, and/or that Energy prices as a group would have to tumble over 50% from current levels!

Of course, if and when energy prices are cut in half, this would also have devastating consequences on the rest of the S&P, and all other asset classes, and almost assuredly force the Fed to not only forget all about hiking rates, but promptly engage in QE4.

Which may be just what the market is pricing in.

The only problem is that one can’t have a world in which both QE4 is priced in (as equities are doing), as well as pricing in the 2015 Fed rate hike (as oil is doing), and is one of the main drivers of the USD strength.

One has to give, and it has to give soon.

Average:

5

Your rating: None Average: 5 (3 votes)

See the article here:

See which stocks are being affected by Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}