Why India's economy isn't imploding like every other emerging market

On Feb. 17, an article appeared in The New York Times, “As Rivals Falter, India’s Economy is Surging Ahead,” by Keith Bradsher, which, among other things, says, “The stock market and rupee are surging. Multinational companies are looking to expand their Indian operations or start new ones. The growth in India’s economy, long a laggard, just matched China’s in recent months…India is riding high on the early success of Prime Minister Narendra Modi and a raft of new business-friendly policies instituted in his first eight months.”

This poses three questions. First, is it true that India is riding high while its rivals are faltering, or is it just that India is feeling the impact of some international problems with a lag, so that the troubles that its rivals are suffering are still in the future for India? Second, if India is in an advantageous situation, why is it? Third, what should be done to protect the Indian advantage?

Is India riding high?

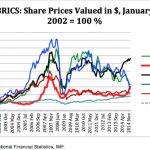

There are bright signs in the Indian economy. Just take a look at the next graph, which shows the stock markets of all the BRICS countries (Brazil, Russia, India, China and South Africa). Brazil and Russia are in a steep dive and South Africa is just stable while India and China are booming. This suggests the existence of an appetite for investing in India and China while investors are taking away their money from Brazil and Russia. In the case of India, such appetite, initially satisfied with stock exchange ventures, could later be turned into brick and mortar investment.

The Indian appeal to investors might be stronger than China’s. Even if the shares are going up in the latter, many enterprises are divesting there and moving to other places, mainly Latin America and Singapore. The main reason for leaving is that Chinese wages have increased beyond what the productivity of the Chinese workers would warrant. Most of these companies are not yet coming to India. They might do it, though. As a token, the chairman of General Motors visited India recently to inspect the company’s preparations to export cars to Chile.

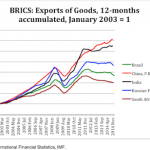

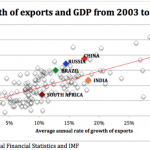

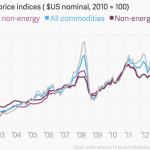

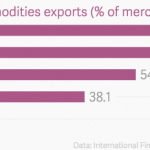

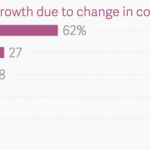

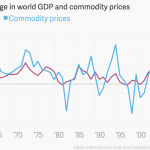

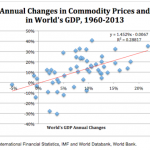

ShareTap image to zoomAnother important sign is contained in the next graph: Out of the five BRICS, just two—China and India—increased their exports in the last year. Those of Russia, Brazil and South Africa have been declining for longer than that.ShareTap image to zoomWe do not have monthly indicators of production for these countries and the data for 2014 is not yet available in comparable form for all of them. However, we have monthly data for exports up to the end of 2014, which is useful because there is a positive correlation between exports and production growth. The next graph shows this correlation in a sample of 135 countries (all the countries in the world for which there was information available). Using this correlation, we can assume that the rates of growth of GDP in Brazil, Russia and South Africa are going down because their exports are falling substantially, while those of India and China are going up because exports are increasing in the two countries.Thus, we can expect China and India to have an advantage over the other BRICS countries not just in terms of exports but also in terms of general economic growth.ShareTap image to zoomBut, why should the exports and production of China and India keep on growing while those of the other three BRICS are going down?Why is India strong?The Indian government is in a good course to increase the country’s investment and growth in a sustainable way. Its plans include, among other things, expanding infrastructure to reduce business costs; creating a true national market by replacing state taxes with a national tax; and reducing the red tape to facilitate doing business. Prime minister Modi is calling universities, institutions and industry to cooperate in the generation of higher value added in the country’s production.These are the right things to do. They, however, are still on the drawing board and, once applied, they will produce full results only in the long term. Of course, just the fact that the government is investing its prestige and its resources on these measures will attract new investments even in the short run. However, apart from this psychological impact, these measures could not possibly be responsible for the current strength of the Indian economy.Rajan magicThe work of Raghuram Rajan, the governor of the Reserve Bank of India, has been more relevant for the construction of such strength. In the crucial months after he took charge of the institution in September 2013, he stabilised the rupee, which had been spinning down, reduced the volatility of the stock markets and reversed the capital outflows that had been ravaging the economy before he was appointed.Additionally, he has strengthened the economy against potential external shocks. In this vein, he has been building up the country’s reserves to prepare for a possible liquidity squeeze in the international markets. Also, he has been pressuring banks to replace the management of financially weak debtor companies, with two objectives in mind: To strengthen the financial situation of the country and to redirect to good uses the resources now being diverted to refinance the loss makers.Through these measures, Rajan has rebuilt the investors’ confidence. His work is evident in the stability of India and the positive outlook investors have for the country.The question is whether this is enough to secure a sustainable flow of investments that would keep exports and GDP growing in the long run while the rest of the emerging markets are going down.To answer this question we must ascertain why Brazil or Russia are going down. It must be something that affects them but not India and China.The fickle commodity pricesLook at the next two graphs. The one on top shows how the prices of commodities have fallen in the last two years and particularly since mid-2014. The second shows the degree of dependence of the exports of BRICS on commodities. Russia, Brazil and South Africa depend on commodities quite heavily while those of China and India do not. The countries that depend more on commodities are the ones that are suffering the most from the current collapse of their prices.ShareTap image to zoomShareTap image to zoomThe next graph shows how the countries with a higher share of commodities in their exports tended to grow faster during the boom of commodities (roughly 2003-2013). Having a relatively low participation of commodities in its exports, India benefited less than many other countries of this boom. Logically, now that the prices are falling, India will suffer less than those other countries.ShareTap image to zoomThe following table shows my estimate of the percent of GDP growth that is due to changes in commodity prices, based on 1960-2013 data (1997-2013 for Russia):ShareTap image to zoomThus, one of the great advantages of India is that falling commodity prices will have a smaller impact than on Russia, Brazil and South Africa. But there is another advantage. The effect of the reduction of commodity prices is not limited to exports. It has an impact on imports and production costs as well.On this other side, the impact of the reduction in the price of one particular commodity, oil, has been extremely positive for India. Before its fall, the annual oil bill represented a $100 billion cost for the economy, about 5% of the country’s GDP. Now this bill has been reduced by half. Rajan told The New York Times (same source cited above) that the fall in oil prices represented a $50 billion gift for the economy.In summary, investors are looking optimistically at India, and for good reasons. Expressed in dollars, stocks in China and India are increasing in value while in most other BRICS are falling fast. China and India’s exports and production have kept on increasing while those of the other BRICS are going down as a result of the catastrophic fall in commodity prices. And, as is well known, China is expected to slow down because its salaries have become too high. India seems to be singled out for its moment of rapid development.An uncertain worldHowever, the fact that the effect of falling commodity prices on its exports and production costs is beneficial relative to the other BRICS does not mean that India can fly high for a long period while these are doing badly. The fall in commodity prices could be a symptom of a larger malady that could affect both commodity-dependent as well as other countries. We can ascertain this by comparing commodity price movements with the growth rates of the entire world’s GDP, including commodity exporters and importers.We do that in the next two graphs. The first compares the annual changes of the world’s total GDP with the changes in commodity prices. They look very close. The second one shows the correlation between the annual changes in those two variables. The degree of correlation is 28%.ShareTap image to zoomShareTap image to zoomThe ups and downs of the commodity prices could not be the explanation for the ups and downs of world production. At the world level, the negative shock that a fall in those prices has on commodity net exporters is compensated by the positive impact it has on the net commodity importers—and the other way around when the prices go up.The causality is likely to run in the other direction: High rates of the world’s GDP are associated with higher industrial production, which in turn results in higher demands for commodities and, therefore, in the prevalence of higher commodity prices. Thus, the changes in the prices of commodities may be a leading indicator of the state of the world’s economy. If this were true, their fall would be announcing an approaching decline in worldwide economic activity.Thus, there is a substantial probability that the world’s economy is approaching a slowdown. India’s current buoyancy may be just a temporary state, not a permanent platform for growth. The fact that it depends less than other BRICS on commodity exports would be just delaying the impact of the worldwide slowdown rather than preventing it.What should be done?As I said before, the government is doing the right things. And it is doing so independently of whether the world economy will grow or slow down in the next several months.If the government is able to convince investors that it will persevere with the policies it has announced India may turn out to be the world’s star performer in the next several decades. If there is a worldwide slowdown, it may avoid its worst consequences in the immediate future, and then become the star performer in the medium term.We welcome your comments at [email protected].This article is a part of Quartz India. For more, follow this link.

See original article here:

Why India's economy isn't imploding like every other emerging market